|

시장보고서

상품코드

1811815

잠수함 시장(2025-2035년)Global Submarine Market 2025 - 2035 |

||||||

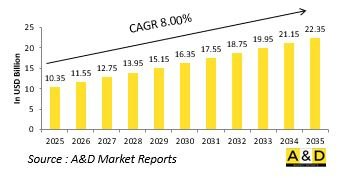

세계의 잠수함 시장 규모는 2025년 103억 5,000만 달러로 추정되며, 2035년까지 223억 5,000만 달러로 성장할 것으로 예측되고 있으며, 2025-2035년 연평균 복합 성장률(CAGR)은 8.00%가 될 것으로 보입니다.

잠수함 시장의 소개

잠수함은 스텔스성, 억지력, 전력투사에 있어 비교할 수 없는 능력을 국가에 제공하기 때문에 방위잠수함 시장은 해군방위 중 가장 전략적인 분야 중 하나입니다. 수상함대와 달리 잠수함은 은밀하게 행동하기 때문에 감지되지 않은 채 정찰, 정보수집, 정밀공격의 임무를 수행할 수 있습니다. 현대 해전에서 잠수함의 역할은 전통적인 전투에 그치지 않습니다. 해로의 보호, 해상 국경의 확보, 특수 작전의 플랫폼으로서의 역할도 매우 중요합니다. 잠수함 시장은 지역 및 세계적인 무대에서 해저 지배의 중시가 높아짐에 따라 형성되고 있습니다. 잠수함은 특히 첨단 무기 시스템과 장기 내구 설계를 갖춘 경우 중요한 억제 수단으로 작용합니다. 잠수함은 장기간에 걸쳐 모습을 숨길 수 있기 때문에 분쟁시에도 평시 순찰시에도 해군부대에게 큰 어드밴티지를 줍니다. 많은 해양 지역의 파워 밸런스는 잠수함의 능력에 의해 점점 좌우되고 있으며, 각국은 선진적인 추진 시스템, 음향 정숙화 기술, 강화된 생존 기능을 갖춘 함대의 현대화를 촉진하고 있습니다. 이는 국가 안보를 보호하고 분쟁 해역에 영향을 미치는 해저 플랫폼의 지속적인 중요성을 반영합니다.

잠수함 시장의 기술 영향

이 기술은 국방 활동에서 잠수함의 설계, 성능, 전략적 중요성을 근본적으로 재정의했습니다. 추진 시스템의 혁신, 특히 공기 독립적 추진과 원자력 기술의 발전은 잠수함의 내구성과 운영 범위를 크게 확대했습니다. 이러한 개발로 잠수함은 장시간 잠수할 수 있어 스텔스성이 강화되고 감지되기 어려워지고 있습니다. 음향 정숙화 기술은 또 다른 중요한 진보 분야입니다. 잠수함은 음향 시그니처를 최소화하는 선체 코팅, 소음 감소 추진기 및 방진 시스템으로 설계되었습니다. 이로 인해 적이 잠수함을 추적하는 것이 더 어려워지고 해전에서 잡기 어려운 잠수함의 역할이 강화됩니다. 스텔스성과 함께 고급 소나 어레이와 센서 스위트의 통합은 상황 인식을 극적으로 향상시켜 잠수함 자신이 숨은 채로 보다 원거리 위협을 감지할 수 있게 합니다. 디지털화와 네트워크화된 능력도 잠수함의 작전을 일변시켰습니다. 최신 플랫폼은 수상 함선, 항공기, 사령부와 실시간 정보 교환이 가능하며, 연결된 해저 네트워크를 구축하고 있습니다. 또한 장거리 순항 미사일과 어뢰와 같은 무기 시스템의 발전으로 잠수함의 공격력이 확대되고 있습니다. 보완적인 자산으로서 무인 수중 차량이 채용된 것으로, 잠수함의 작전 범위는 더욱 재조합되어, 기술이 어떻게 잠수함을 해군력의 결정적인 수단으로서 계속해서 높이고 있는지를 실증하고 있습니다.

잠수함 시장의 주요 촉진요인

방위 분야에서의 잠수함 수요는 전략적 요청, 안보상의 과제, 기술적 기회의 조합에 의해 추진되고 있습니다. 각국은 잠수함을 해상 우위를 확보하고 해로와 해양자원에 연관된 경제적 이익을 지키기 위해 필수적인 자산으로 간주하고 있습니다. 잠수함의 은밀한 행동 능력은 분쟁이 격화하는 해양 환경에서의 억지력, 전력 투사, 정보 수집에 필수적입니다. 중요한 수로를 둘러싼 지정학적 대립과 영토문제는 더욱 수요를 가속시킵니다. 잠수함은 해군이 적의 활동을 감시하고, 해양 권익을 행사하고, 수상 함대처럼 시인하지 않고 전력을 투사할 수 있게 함으로써 전략적 우위를 제공합니다. 해로가 경쟁하는 지역에서 긴장이 증가함에 따라 잠수함 능력에 대한 투자는 방어 계획의 중심이 됩니다. 기존 함대의 근대화도 중요한 추진력입니다. 많은 해군 강대국은 구식 플랫폼을 단계적으로 폐지하고 선진적인 추진력, 스텔스, 무기 기술을 도입한 잠수함으로 대체하고 있습니다. 게다가 잠수함이 정상형과 핵억제 역할을 모두 수행할 수 있기 때문에 국가안전보장 전략에서 잠수함의 가치가 높아지고 있습니다. 잠수함은 분쟁 시나리오 이외에도 감시, 조사, 해저 인프라 보호 등 비전투 임무에도 공헌하고 있으며, 여러 작전 영역에 걸쳐 지속적인 관련성을 확보하고 있습니다.

잠수함 시장의 지역 동향

방위용 잠수함 시장의 지역 역학은 지역, 안보 환경, 전략적 우선순위에 의해 형성됩니다. 광대한 해안선과 중요한 해로에 접근하는 해양 국가는 영해의 안전을 확보하고 해안에서 멀리 떨어진 곳으로의 전력 투사를 위해 잠수함 함대를 선호합니다. 해안 방어, 반 접근 전략, 지역의 적대자에 대한 억지력의 모두가, 이 지역에서의 잠수함 조달의 원동력이 되고 있습니다. 해군 선진국은 원자력 잠수함을 중시하고 장기적인 전개와 세계 전개가 가능한 플랫폼에 투자하고 있습니다. 이 함선은 전략적 억지의 요점으로 보통 작전과 2차 공격 핵전력을 모두 지원합니다. 이와는 대조적으로, 예산이 한정된 지역에서는 최신의 추진력과 센서 기술을 탑재한 디젤 전기 잠수함이 선호되는 경우가 많아 비용과 작전 효과의 밸런스가 취해지고 있습니다. 분쟁해협과 분쟁해역 등의 지정학적 핫스팟은 지역 수요를 더욱 증폭시킵니다. 잠수함은 항상 바다에 존재감을 유지하고 적의 움직임을 모니터링하고 중요한 수로의 지배를 보장하기 위해 배치됩니다. 산업 능력도 동향에 영향을 미칩니다. 자립성을 높이기 위해 자국에서의 잠수함 건조를 우선하는 나라도 있고, 선진적인 플랫폼을 획득하기 위해 파트너십이나 합작 사업을 추구하는 나라도 있습니다. 이러한 지역의 다양성은 잠수함에 대한 세계적인 관심을 넓히는 반면, 각 시장 부문은 지역, 자원 및 안보 과제와 연관된 지역별 우선순위를 반영합니다.

주요 잠수함 프로그램

Mazagon Dock Shipbuilders는 독일 ThyssenKrupp Marine Systems(TKMS)와 주요 잠수함 구상에 대한 공식 계약 협의를 시작했습니다. TKMS는 인도의 조달 당국과 공식적으로 협상을 시작하여 해군 분야에서 인독의 파트너십이 탄생하고 있음을 보여줍니다. TKMS의 주문 잔액은 6월 30일 현재 185억 유로에 달하고 있으며, 그 중 일부는 현재 진행 중인 협상 때문입니다. 프로젝트에 대한 자세한 내용은 아직 비밀이지만, Mazagon Dock의 적극적인 참여는 인도의 해양 방위 산업에서 전략적 중요성을 보여줍니다. 이번 합의는 Mazagon Dock의 주문 파이프라인을 대폭 강화하고 인도의 해군 능력 근대화에 기여를 강화하는 것입니다.

목차

잠수함 시장 보고서 정의

잠수함 시장 세분화

유형별

용도별

지역별

향후 10년간 잠수함 시장 분석

이 장에서는 10년간의 잠수함 시장 분석을 통해 잠수함 시장의 성장, 변화하는 동향, 기술 채용의 개요 및 시장의 매력에 대한 자세한 개요를 제공합니다.

잠수함 시장 시장 기술

이 부문에서는 이 시장에 영향을 미칠 것으로 예상되는 상위 10개 기술과 이러한 기술이 시장 전체에 미칠 수 있는 영향에 대해 설명합니다.

세계 잠수함 시장 예측

이 시장의 10년간 예측은 위의 부문에 걸쳐 상세하게 설명되어 있습니다.

지역별 잠수함 시장 동향과 예측

이 부문은 지역별 잠수함 시장 동향, 촉진요인, 억제요인, 과제, 그리고 정치, 경제, 사회, 기술 등의 측면을 망라하고 있습니다. 또한 지역별 시장 예측과 시나리오 분석도 자세히 다루고 있습니다. 지역 분석의 마지막 단계에서는 주요 기업프로파일 링, 공급업체의 상황, 기업 벤치 마크 등에 대해 분석합니다. 현재 시장 규모는 일반적인 시나리오를 기반으로 추정됩니다.

북미

촉진요인, 억제요인, 과제

PEST

시장 예측 및 시나리오 분석

주요 기업

공급자 계층의 상황

기업 벤치마킹

유럽

중동

아시아태평양

남미

잠수함 시장 국가별 분석

이 장에서는 이 시장에서 주요 방어 프로그램을 다루며 이 시장에서 신청된 최신 뉴스와 특허에 대해서도 설명합니다. 또한 국가 수준의 10년간 시장 예측과 시나리오 분석에 대해서도 설명합니다.

미국

방위 프로그램

최신 뉴스

특허

이 시장의 현재 기술 성숙도

시장 예측 및 시나리오 분석

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

잠수함 시장 기회 행렬

기회 행렬은 독자가 이 시장에서 기회의 높은 부문을 이해하는 데 도움이 됩니다.

잠수함 시장 보고서에 관한 전문가의 의견

이 시장의 잠재적 분석에 대한 우리의 전문가의 의견을 제공합니다.

결론

리서치사에 대하여

JHS 25.09.22The Global Submarine market is estimated at USD 10.35 billion in 2025, projected to grow to USD 22.35 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 8.00% over the forecast period 2025-2035.

Introduction to Submarine Market:

The defense submarine market represents one of the most strategic areas within naval defense, as submarines provide nations with unmatched capabilities in stealth, deterrence, and force projection. Unlike surface fleets, submarines operate covertly, enabling them to conduct surveillance, intelligence gathering, and precision strike missions while remaining undetected. Their role in modern naval warfare extends beyond traditional combat; they are also crucial for protecting sea lanes, securing maritime borders, and serving as platforms for special operations. The market is shaped by the growing emphasis on undersea dominance in both regional and global theaters. Submarines serve as critical tools of deterrence, especially when equipped with advanced weapon systems and long-endurance designs. Their ability to remain hidden for extended periods gives naval forces a significant advantage, both in times of conflict and during peacetime patrols. The balance of power in many maritime regions is increasingly influenced by submarine capabilities, prompting nations to modernize fleets with advanced propulsion systems, acoustic quieting technologies, and enhanced survivability features. This makes the submarine market a central focus of naval procurement programs, reflecting the enduring importance of undersea platforms in safeguarding national security and projecting influence across contested waters.

Technology Impact in Submarine Market:

Technology has fundamentally redefined the design, performance, and strategic importance of submarines in defense operations. Innovations in propulsion systems, particularly air-independent propulsion and advancements in nuclear technology, have significantly extended the endurance and operational range of submarines. These developments allow vessels to remain submerged for longer durations, thereby enhancing stealth and reducing vulnerability to detection. Acoustic quieting technologies are another critical area of progress. Submarines are increasingly designed with hull coatings, noise-reducing propulsors, and vibration isolation systems that minimize their acoustic signature. This makes them more difficult for adversaries to track, bolstering their role as elusive assets in naval warfare. Alongside stealth, the integration of sophisticated sonar arrays and sensor suites has dramatically improved situational awareness, enabling submarines to detect threats at greater distances while remaining hidden themselves. Digitalization and network-enabled capabilities have also transformed submarine operations. Modern platforms can exchange real-time intelligence with surface ships, aircraft, and command centers, creating a connected undersea network. Additionally, advances in weapon systems, including long-range cruise missiles and torpedoes, have expanded the offensive potential of submarines. The adoption of unmanned underwater vehicles as complementary assets is further reshaping their operational scope, demonstrating how technology continues to elevate submarines as decisive instruments of naval power.

Key Drivers in Submarine Market:

The demand for submarines in the defense sector is propelled by a combination of strategic imperatives, security challenges, and technological opportunities. Nations view submarines as vital assets for ensuring maritime dominance and protecting economic interests tied to sea routes and offshore resources. Their ability to operate covertly makes them essential for deterrence, power projection, and intelligence gathering in an increasingly contested maritime environment. Geopolitical rivalries and territorial disputes over key waterways further accelerate demand. Submarines provide a strategic edge by allowing navies to monitor adversary activities, enforce maritime claims, and project force without the visibility of surface fleets. As tensions escalate in regions with contested sea lanes, investments in submarine capabilities become central to defense planning. The modernization of existing fleets is another significant driver. Many naval powers are phasing out older platforms and replacing them with submarines that incorporate advanced propulsion, stealth, and weapons technology. Additionally, the dual capability of submarines to conduct both conventional and nuclear deterrence roles enhances their value in national security strategies. Beyond conflict scenarios, submarines also contribute to non-combat missions such as surveillance, research, and undersea infrastructure protection, ensuring their continued relevance across multiple operational domains.

Regional Trends in Submarine Market:

Regional dynamics in the defense submarine market are shaped by geography, security environments, and strategic priorities. Maritime nations with expansive coastlines and access to vital sea lanes prioritize submarine fleets to secure territorial waters and project power far from their shores. Coastal defense, anti-access strategies, and deterrence against regional adversaries all drive submarine procurement in these areas. Advanced naval powers emphasize nuclear-powered submarines, investing in platforms capable of extended deployments and global reach. These vessels serve as cornerstones of strategic deterrence, supporting both conventional operations and second-strike nuclear capabilities. In contrast, regions with limited budgets often favor diesel-electric submarines equipped with modern propulsion and sensor technologies, balancing cost with operational effectiveness. Geopolitical hotspots such as contested straits and disputed maritime zones further amplify regional demand. Submarines are deployed to maintain a constant undersea presence, monitor adversary movements, and ensure control over vital waterways. Industrial capabilities also influence trends: some nations prioritize indigenous submarine construction to enhance self-reliance, while others pursue partnerships and joint ventures to acquire advanced platforms. This regional diversity ensures that while global interest in submarines is widespread, each market segment reflects localized priorities tied to geography, resources, and security challenges.

Key Submarine Program:

Mazagon Dock Shipbuilders has entered official contract discussions with Germany's ThyssenKrupp Marine Systems (TKMS) for a major submarine initiative. TKMS has formally opened negotiations with Indian procurement authorities, indicating an emerging Indo-German partnership in the naval sector. The company's order backlog reached EUR 18.50 billion as of June 30, with part of this attributed to the ongoing negotiations. Although detailed project specifics remain confidential, Mazagon Dock's active participation showcases its strategic importance within India's maritime defense industry. The agreement's outcome could substantially boost Mazagon Dock's order pipeline and enhance its contribution to the modernization of India's naval capabilities.

Table of Contents

Submarine Market Report Definition

Submarine Market Segmentation

By Type

By Application

By Region

Submarine Market Analysis for next 10 Years

The 10-year submarine market analysis would give a detailed overview of submarine market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Submarine Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Submarine Market Forecast

The 10-year submarine market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Submarine Market Trends & Forecast

The regional submarine market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Submarine Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Submarine Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Submarine Market Report

Hear from our experts their opinion of the possible analysis for this market.