|

시장보고서

상품코드

1951129

방위용 화기 관제 레이더/일루미네이터 시장(2026-2036년)Global Defense Fire Control Radars / Illuminators Market 2026-2036 |

||||||

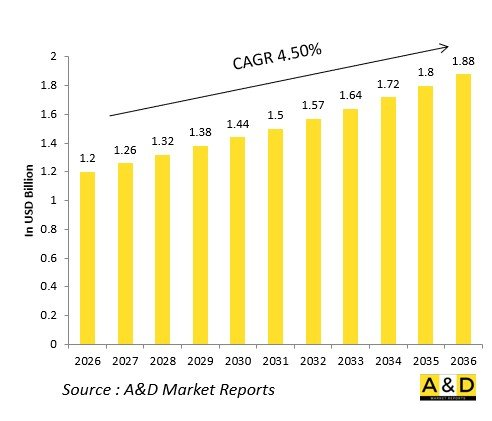

세계의 방위용 화기 관제 레이더/일루미네이터 시장 규모는 2026년 12억 달러에서 2026-2036년의 예측 기간 중 CAGR 4.50%로 성장하며, 2036년에는 18억 8,000만 달러에 달할 것으로 예측됩니다.

소개:

세계 방산 화기관제 레이더/조명기 시장은 현대화, 통합, 디지털화를 특징으로 하는 변혁의 10년을 맞이하고 있습니다. 표적 포착과 공격 정확도의 기반이 되는 이러한 시스템은 멀티 도메인 전략에서 점점 더 중요한 역할을 하고 있습니다. 전 세계 각국의 국방 기관들은 복잡하고 통제된 환경에서도 첨단 감지, 추적, 정밀 유도 능력을 발휘하는 레이더 솔루션에 대한 투자를 진행하고 있습니다. 전자 주사식 위상배열, 디지털 빔포밍, 네트워크화된 표적 포착 시스템의 채택으로 화기관제 레이더는 지능화된 전투 지원 시스템으로 재정의되고 있습니다. 지정학적 경쟁의 격화와 실시간 상황 인식에 대한 수요가 증가함에 따라 각 제조업체들은 긴 수명과 적응성을 보장하기 위해 모듈식 및 소프트웨어 업그레이드가 가능한 아키텍처에 초점을 맞추었습니다. 군용 플랫폼이 더 높은 살상 능력과 상호 운용성을 위해 진화하는 가운데, 화기관제 레이더 및 조명기 시스템은 통합 방공 및 미사일 방어 아키텍처의 핵심 자산으로 자리매김하고 있으며, 세계 방산 시장 전반에 걸쳐 상당한 장기적 성장 기회를 창출하고 있습니다.

방어용 화기 관제 레이더/조명기의 기술적 영향

기술 혁신은 국방용 화기관제 레이더/조명기의 설계, 성능, 운용의 다양성에 혁명을 일으키고 있습니다. 능동형 전자식 스캐닝 어레이(AESA)와 디지털 신호 처리로 전환하여 보다 빠른 목표물 감지, 향상된 추적 정확도, 전자파 방해에 대한 내성을 실현했습니다. AI와 머신러닝의 통합이 진행되어 위협 분류와 목표 우선순위 자동화를 통해 전자 환경이 밀집된 상황에서 신속한 의사결정을 돕고 있습니다. 네트워크 중심 전술 개념은 상호 운용성을 더욱 강화하여 레이더 시스템이 육상, 항공, 해상 자산 간에 표적 데이터를 원활하게 공유할 수 있도록 합니다. 또한 개방형 아키텍처 설계로의 전환은 확장성과 손쉬운 업그레이드를 보장하며, 국방 현대화 계획에 부합합니다. 신흥 소재, 경량화 부품, 에너지 절약형 송수신 모듈도 설계 이념에 영향을 미쳐 신뢰성 향상과 유지보수 비용 절감을 실현하고 있습니다. 이러한 혁신 기술이 결합되어 기존의 화기관제 레이더는 차세대 방어 시나리오에서 효과적으로 운용할 수 있는 지능적이고 적응력이 뛰어난 시스템으로 변모하고 있습니다.

국방용 화기관제레이더/조명기의 주요 추진요인

여러 가지 전략적 및 기술적 요인이 세계 방산용 화기 관제 레이더/조명기 시장 수요를 주도하고 있습니다. 지정학적 긴장 고조와 영토 분쟁은 각국의 방공 능력과 상황 인식 능력을 강화하도록 촉구하고 있습니다. 정밀한 표적 포착에 대한 집중과 다영역 작전 준비 태세 확립이 결합되어 첨단 레이더 유도 시스템의 국방 조달을 가속화하고 있습니다. 탱크, 해군 함정, 전투기 등 구식 플랫폼의 현대화는 여전히 주요 성장 요인입니다. 또한 스텔스 기술의 보급과 극초음속 위협 증가로 감지 및 추적 범위가 강화된 고주파 화기관제 레이더에 대한 관심이 높아지고 있습니다. 국방 예산은 살상력, 생존성 및 임무 수행 보장을 향상시키기 위해 레이더 기반 화기 통제 솔루션을 우선적으로 채택하는 경향이 증가하고 있습니다. 국방부대가 디지털화 및 네트워크 지원 전투 시스템으로 전환하는 가운데, 레이더 기반 조명 및 화기 관제 기술에 대한 투자는 계속 확대될 것이며, 국가 안보 요구와 전략적 억지력을 모두 지원할 것으로 전망됩니다.

방산용 화기관제 레이더/조명기의 지역별 동향

방위 화기 관제 레이더/조명기 시장의 지역적 동향은 다양한 안보 우선순위, 산업 역량, 현대화 계획에 의해 형성되고 있습니다. 북미는 기술 혁신의 선두주자로서 육상, 항공 및 해군 플랫폼에서 AESA 레이더 통합의 진전을 주도하고 있습니다. 유럽은 공동 안보의 틀 안에서 상호 운용성과 센서 융합을 강조하는 공동 방위 계획에 집중하고 있습니다. 아시아태평양에서는 견고한 국방 확대와 지속적인 영토 분쟁이 레이더 유도 무기 시스템의 빠른 조달을 촉진하고 있습니다. 중동 및 아프리카 일부 지역의 신흥 시장에서는 항공기 및 미사일 위협에 대응하기 위해 레이더 현대화에 대한 투자가 진행되고 있으며, 대부분 세계 제조업체와의 파트너십 및 오프셋 계약을 통해 이루어지고 있습니다. 한편, 여러 지역에서 방위산업 자립화를 위한 노력이 강화되고 있으며, 국산 레이더 생산이 촉진되고 있습니다. 지역적 군사 동맹과 기술 공유 협정은 계속해서 조달 결정에 영향을 미치고 있으며, 화기 통제 및 조명 시스템 시장에서 경쟁이 치열하고 다양한 시장 상황을 보장하고 있습니다.

세계의 방산용 화기관제 레이더/조명기 시장을 조사했으며, 주요 동향, 시장 영향요인, 주요 기술 및 그 영향력, 주요 지역 및 국가별 동향, 시장 기회 분석 등의 정보를 정리하여 전해드립니다.

목차

방위용 화기 관제 레이더/일루미네이터 시장 : 목차

방위용 화기 관제 레이더/일루미네이터 시장 : 리포트 정의

방위용 화기 관제 레이더/일루미네이터 시장 : 세분화

향후 10년간 방위용 화기 관제 레이더/일루미네이터 시장 분석

세계의 방위용 화기 관제 레이더/일루미네이터 시장 : 예측

방위용 화기 관제 레이더/일루미네이터 시장의 동향·예측 : 지역별

시장 예측·시나리오 분석

방위용 화기 관제 레이더/일루미네이터 시장 : 국가별 분석

시장 예측·시나리오 분석

방위용 화기 관제 레이더/일루미네이터 시장 : 기회 매트릭스

결론

KSA 26.03.19The Global defense fire control radars and illuminators market is estimated at USD 1.2 billion in 2026, projected to grow to USD 1.88 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.50% over the forecast period 2026-2036.

Introduction:

The global market for defense fire control radars and illuminators is entering a transformative decade marked by modernization, integration, and digitization. These systems, which form the backbone of target acquisition and engagement accuracy, are increasingly pivotal to multi-domain operations. Defense forces worldwide are investing in radar solutions capable of performing under complex, contested environments with enhanced detection, tracking, and precision guidance capabilities. The adoption of electronically scanned arrays, digital beamforming, and networked targeting systems is redefining fire control radars as intelligent combat enablers. Amid heightened geopolitical competition and the demand for real-time situational awareness, manufacturers are focusing on modular, software-upgradable architectures to ensure longevity and adaptability. As military platforms evolve toward higher lethality and interoperability, fire control radar and illuminator systems stand as critical assets within integrated air and missile defense architectures, driving substantial long-term growth opportunities across global defense markets.

Technology Impact in Defense Fire Control Radars / Illuminators

Technological advancements are revolutionizing the design, performance, and operational versatility of defense fire control radars and illuminators. The shift toward active electronically scanned arrays (AESA) and digital signal processing enables faster target detection, improved tracking accuracy, and resilient performance against electronic countermeasures. Artificial intelligence and machine learning are increasingly integrated to automate threat classification and target prioritization, supporting rapid decision-making in dense electronic environments. Network-centric warfare concepts further enhance interoperability, allowing radar systems to share targeting data seamlessly across land, air, and naval assets. Moreover, the transition to open-architecture designs ensures scalability and easier upgrades, aligning with defense modernization programs. Emerging materials, lighter components, and energy-efficient transmit/receive modules are also influencing design philosophies, improving reliability and reducing maintenance costs. Collectively, these innovations are transforming traditional fire control radars into intelligent, adaptive systems capable of operating effectively across next-generation defense scenarios.

Key Drivers in Defense Fire Control Radars / Illuminators

Multiple strategic and technological factors are propelling demand in the global defense fire control radar and illuminator market. Rising geopolitical tensions and territorial disputes are encouraging nations to upgrade their air defense and situational awareness capabilities. The focus on precision targeting, coupled with multi-domain operational readiness, has intensified defense procurement of advanced radar-guidance systems. Modernization of legacy platforms-such as tanks, naval vessels, and fighter aircraft-remains a key growth enabler. Additionally, the proliferation of stealth technologies and hypersonic threats is stimulating interest in high-frequency fire control radars with enhanced detection and tracking ranges. Defense budgets increasingly prioritize radar-based fire control solutions to improve lethality, survivability, and mission assurance. As defense forces shift toward digitized and network-enabled combat systems, investments in radar-based illumination and fire control technology will continue to expand, supporting both national security imperatives and strategic deterrence objectives.

Regional Trends in Defense Fire Control Radars / Illuminators

Regional dynamics in the defense fire control radar and illuminator market are shaped by divergent security priorities, industrial capabilities, and modernization programs. North America remains a leader in technological innovation, driving advancements in AESA radar integration across land, air, and naval platforms. Europe focuses on collaborative defense programs emphasizing interoperability and sensor fusion under joint security frameworks. In the Asia-Pacific region, robust defense expansion and ongoing territorial disputes are fueling rapid procurement of radar-guided weapon systems. Emerging markets in the Middle East and parts of Africa are investing in radar modernization to counter aerial and missile threats, often through partnership or offset agreements with global manufacturers. Meanwhile, increasing defense industrial self-reliance initiatives in several regions are encouraging indigenous radar production. Regional military alliances and technology-sharing agreements continue to influence procurement decisions, ensuring a competitive and diversified market landscape for fire control and illumination systems.

Key Defense Fire Control Radars / Illuminators Programs

Global defense programs involving fire control radars and illuminators demonstrate significant diversity in scale, scope, and technological ambition. Advanced radar initiatives on modern fighter aircraft, naval combatants, and air defense units highlight the strategic value of precision-targeting systems. Several leading defense manufacturers are developing multi-mode radars capable of integrating target tracking, illumination, and guidance within networked architectures. Collaborative programs emphasize modular designs that can be adapted for both domestic and export markets, aligning with evolving mission profiles. In addition, upgrades to existing radar installations are focused on improving electronic counter-countermeasure performance, wider frequency coverage, and data-link integration. Many nations are incorporating these systems into layered air defense structures that also support missile interception missions. The continued evolution of such programs underscores the critical role of adaptable, high-performance radar systems in ensuring operational edge and force protection across modern defense ecosystems.

Table of Contents

Defense Fire Control Radars / Illuminators Market - Table of Contents

Defense Fire Control Radars / Illuminators Market Report Definition

Defense Fire Control Radars / Illuminators Market Segmentation

By Region

By Platform

By Application

By Frequency

Defense Fire Control Radars / Illuminators Market Analysis for next 10 Years

The 10-year Defense Fire Control Radars / Illuminators Market analysis would give a detailed overview of Defense Fire Control Radars / Illuminators Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Fire Control Radars / Illuminators Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Fire Control Radars / Illuminators Market Forecast

The 10-year Defense Fire Control Radars / Illuminators Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Fire Control Radars / Illuminators Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Fire Control Radars / Illuminators Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Fire Control Radars / Illuminators Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Fire Control Radars / Illuminators Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports