|

시장보고서

상품코드

1913305

나프탈렌 시장 예측 : 기회, 성장 요인, 업계 동향 분석(2026-2035년)Naphthalene Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

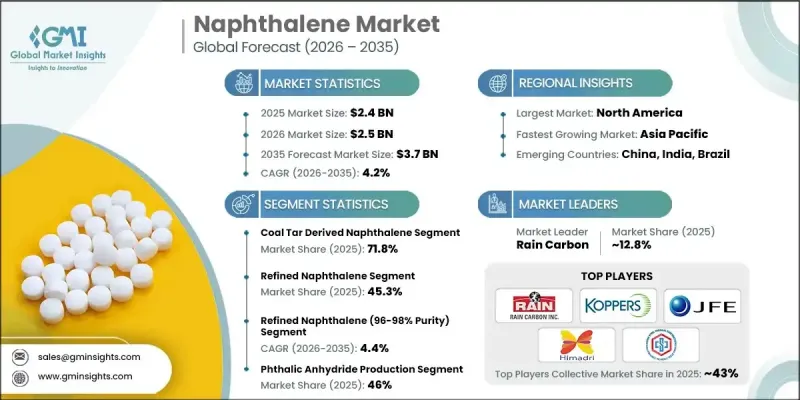

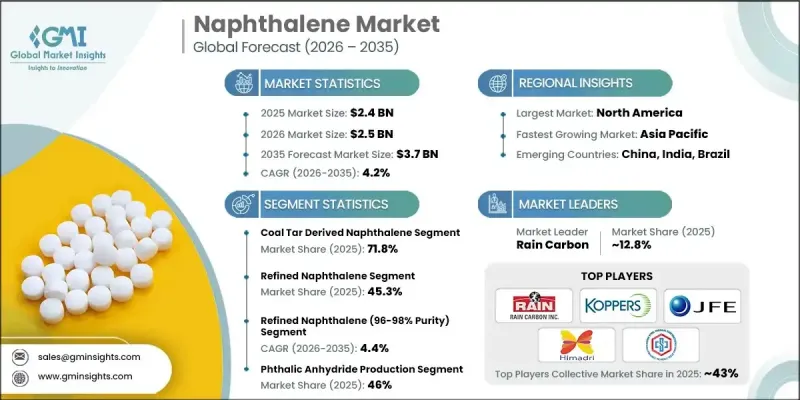

세계 나프탈렌 시장은 2025년에 24억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 4.2%로 성장하여 37억 달러에 이를 것으로 예측됩니다.

나프탈렌(화학식: C10H8)은 주로 콜타르 처리 및 석유 정제를 통해 생산되는 다환 방향족 탄화수소입니다. 본 물질은 정제 나프탈렌, 알킬나프탈렌, 고체 변종 등 여러 상업 형태로 공급되며, 순도는 90-95%의 조품 등급에서 99% 이상의 고순도 등급까지 다양합니다. 화학 제조 체인에서 핵심 원료, 건설 관련 배합제, 확립된 산업용도로 널리 이용되고 있습니다. 무수 프탈산 수요 증가, 건설용 화학제품의 사용 확대, 특수 화학제품 용도의 개발이 함께 세계 시장 확대를 견인하고 있습니다. 생산자는 진화하는 고객 사양을 수용하기 위해 깨끗한 제조 공정, 정밀 정제 시스템 및 차별화된 제품 등급에 주력하고 있습니다. 가공 효율과 일관성 향상은 여러 최종 이용 산업 및 지역에서 안정적인 수요를 지원합니다. 수요의 성장, 기술의 진보, 다양한 용도의 조합이 결합해, 나프탈렌 시장의 장기적인 발전을 지속적으로 지지하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 24억 달러 |

| 예측 금액 | 37억 달러 |

| CAGR | 4.2% |

정제 및 등급 관리의 기술 발전으로 고순도 나프탈렌의 제조가 재구성되었습니다. 석탄 타르 및 석유 유래의 양 원료에 있어서, 99% 이상의 고순도 레벨의 고성능 용도에의 대응, 결정화 관리의 엄밀화, 배치간의 일관성 향상이 가능하게 되었습니다. 이러한 진보는 고부가가치 화학 합성 및 중간체 생산에 필요한 엄격한 품질 기준을 충족시키기 위한 것입니다. 증류기술의 고도화, 결정화 공정의 개량, 수소화 기반의 공정에 의해 불순물 함량이 저감되는 동시에 기능적인 신뢰성이 향상되어, 제조업체는 보다 예측 가능한 성능과 폭넓은 산업에서의 수용성을 갖춘 나프탈렌 제품을 제공할 수 있게 되었습니다.

콜타르 유래 나프탈렌 부문은 2025년에 71.8%의 점유율을 차지했고 2026년부터 2035년에 걸쳐 CAGR 4%로 확대될 것으로 예측되고 있습니다. 그 우위성은 철강 및 코크스 처리 공정과 연계한 성숙한 생산 시스템, 유리한 수율 경제성, 안정된 제품 품질에 기인하고 있습니다. 이 원료 공급원은 대규모 생산을 지원하면서 비용 효율성과 안정적인 공급을 유지하는 광범위한 세계 콜타르 인프라의 혜택을 누리고 있습니다. 주요 소비지역의 견고한 기반과 산업 밸류체인에 대한 수년간의 통합이 결합되어 세계 나프탈렌 시장의 주도적 지위를 지속적으로 강화하고 있습니다.

정제된 나프탈렌 부문은 2025년에 45.3%의 점유율을 차지했고 2035년까지 연평균 복합 성장률(CAGR)3.6%로 성장할 것으로 예측되고 있습니다. 이 형태는 안정적인 순도와 우수한 취급 특성으로 인해 대량 화학 처리의 우선 옵션입니다. 통합 화학 제조 시설 내에서 광범위한 사용은 효율적인 다운스트림 공정과 신뢰할 수 있는 운영 성능을 지원합니다. 확립된 생산 네트워크와 입증된 경제적 이점은 세계의 화학 생산 기지에서 지속적인 이점에 기여하고 있습니다.

미국 나프탈렌 시장은 2025년에 9억 2,990만 달러의 규모를 기록해 산업 및 건설 관련 분야에 있어서의 안정된 소비에 지지된 견고한 지역 수요를 반영하고 있습니다. 확립된 생산 시설, 통합된 가공 인프라, 지속적인 최종 용도 수요의 존재는 국내 시장의 안정성을 지원합니다. 가공 효율과 공급망 신뢰성에 대한 지속적인 투자는 북미 전역에서 수요 성장의 기반이 되고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 수익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규기술

- 가격 동향

- 지역별

- 제품 등급별

- 장래 시장 동향

- 특허 상황

- 무역 통계(HS코드)(참고: 무역 통계는 주요 국가에 대해서만 제공됨.)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 이니셔티브

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 형태별, 2022-2035

- 정제 나프탈렌

- 알킬 나프탈렌

- 고형 나프탈렌

- 기타

제6장 시장 추정 및 예측 : 원료별, 2022-2035

- 석탄 타르 유래 나프탈렌

- 석유 유래 나프탈렌

- 재생 원료 및 2차 원료

제7장 시장 추정 및 예측 : 제품 등급별, 2022-2035

- 원료 나프탈렌(순도 90-95%)

- 정제 나프탈렌(순도 96-98%)

- 고순도 나프탈렌(99% 이상의 순도)

- 특수 등급 및 맞춤형 제품

제8장 시장 추정 및 예측 : 용도별, 2022-2035

- 프탈산 무수물(Phthalic anhydride) 생산

- 계면활성제 및 분산제

- 감수제(건설용 화학제품)

- 염료 및 안료(화학 중간체)

- 기존 용도(방충제, 가죽 처리제)

- 신흥 및 기타 용도

제9장 시장 추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Atom Scientific

- CDH Fine Chemical

- China Steel Chemical

- Deza

- Dong-Suh Chemical Ind. Co., Ltd.

- ExxonMobil Chemical

- Himadri Specialty Chemical Ltd.

- JFE Chemical Corporation

- King Industries

- Koppers

- PCC Group

- Rain Carbon

- Tulstar Products

The Global Naphthalene Market was valued at USD 2.4 billion in 2025 and is estimated to grow at a CAGR of 4.2% to reach USD 3.7 billion by 2035.

Naphthalene, chemically identified as C10H8, is a polycyclic aromatic hydrocarbon produced mainly through coal tar processing and petroleum refining. The material is supplied in multiple commercial forms such as refined naphthalene, alkyl naphthalene, and solid variants, with purity levels spanning from crude grades of 90-95% to high-purity grades exceeding 99%. It is widely used as a core feedstock in chemical manufacturing chains, construction-related formulations, and established industrial applications. Rising demand for phthalic anhydride, increasing use of construction chemicals, and the development of specialty chemical applications are collectively shaping market expansion worldwide. Producers are focusing on cleaner production routes, precision purification systems, and differentiated product grades to meet evolving customer specifications. Improvements in processing efficiency and consistency are supporting stable demand across multiple end-use industries and regions. This combination of demand growth, technology advancement, and diversified applications continues to support long-term development of the naphthalene market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.4 billion |

| Forecast Value | $3.7 billion |

| CAGR | 4.2% |

Technological progress in purification and grade control is reshaping naphthalene manufacturing by enabling purity levels above 99% for high-performance uses, tighter crystallization management, and improved batch consistency from both coal tar and petroleum-based sources. These advancements are designed to meet strict quality benchmarks required for high-value chemical synthesis and intermediate production. Enhanced distillation, crystallization refinement, and hydrogenation-based processes are lowering impurity content while improving functional reliability, allowing manufacturers to deliver naphthalene products with more predictable performance and broader industrial acceptance.

The coal tar-based naphthalene segment held 71.8% share in 2025 and is forecast to grow at a CAGR of 4% from 2026 to 2035. Its dominance is attributed to mature production systems aligned with steel and coke processing operations, favorable yield economics, and stable output quality. This source benefits from extensive global coal tar infrastructure that supports large-scale production while maintaining cost efficiency and dependable supply. Its strong foothold across major consuming regions, combined with long-standing integration into industrial value chains, continues to reinforce its leadership in the global naphthalene landscape.

The refined naphthalene segment accounted for 45.3% share in 2025 and is anticipated to register a CAGR of 3.6% through 2035. This form remains the preferred choice for large-volume chemical processing due to its consistent purity and favorable handling characteristics. Its widespread use within integrated chemical manufacturing facilities supports efficient downstream processing and reliable operational performance. Established production networks and proven economic advantages contribute to its continued dominance across global chemical production hubs.

US Naphthalene Market generated USD 929.9 million in 2025, reflecting strong regional demand driven by steady consumption across industrial and construction-related sectors. The presence of established production facilities, integrated processing infrastructure, and sustained end-use requirements supports market stability within the country. Ongoing investment in processing efficiency and supply chain reliability continues to underpin demand growth across North America.

Key companies active in the Naphthalene Market include Rain Carbon, Himadri Specialty Chemical Ltd., ExxonMobil Chemical, Koppers, PCC Group, China Steel Chemical, JFE Chemical Corporation, and Dong-Suh Chemical Ind. Co., Ltd., Deza, King Industries, Atom Scientific, CDH Fine Chemical, and Tulstar Products. Companies operating in the Naphthalene Market are strengthening their market position through capacity optimization, investment in advanced purification technologies, and expansion of high-purity product portfolios. Many players are focusing on operational integration with upstream raw material sources to improve cost control and supply security. Strategic partnerships and long-term supply agreements are being used to stabilize demand and enhance regional presence. Firms are also prioritizing process efficiency, emission reduction, and sustainable production practices to align with evolving regulatory expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Source

- 2.2.2 Form

- 2.2.3 Product Grade

- 2.2.4 Application

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product grade

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Form, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Refined naphthalene

- 5.3 Alkyl naphthalene

- 5.4 Naphthalene solid

- 5.5 Other

Chapter 6 Market Estimates and Forecast, By Source, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Coal tar derived naphthalene

- 6.3 Petroleum derived naphthalene

- 6.4 Recycled and secondary sources

Chapter 7 Market Estimates and Forecast, By Product Grade, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Crude naphthalene (90-95% purity)

- 7.3 Refined naphthalene (96-98% purity)

- 7.4 Pure naphthalene (99%+ purity)

- 7.5 Specialty grades and custom products

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Phthalic anhydride production

- 8.3 Surfactants & dispersants

- 8.4 Water reducing agents (construction chemicals)

- 8.5 Dyes & pigments (chemical intermediates)

- 8.6 Traditional applications (mothballs, tanning agents)

- 8.7 Emerging and other applications

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Atom Scientific

- 10.2 CDH Fine Chemical

- 10.3 China Steel Chemical

- 10.4 Deza

- 10.5 Dong-Suh Chemical Ind. Co., Ltd.

- 10.6 ExxonMobil Chemical

- 10.7 Himadri Specialty Chemical Ltd.

- 10.8 JFE Chemical Corporation

- 10.9 King Industries

- 10.10 Koppers

- 10.11 PCC Group

- 10.12 Rain Carbon

- 10.13 Tulstar Products