|

시장보고서

상품코드

1913308

라미네이트 튜브 시장 예측 : 기회, 성장 요인, 업계 동향 분석(2026-2035년)Laminated Tubes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

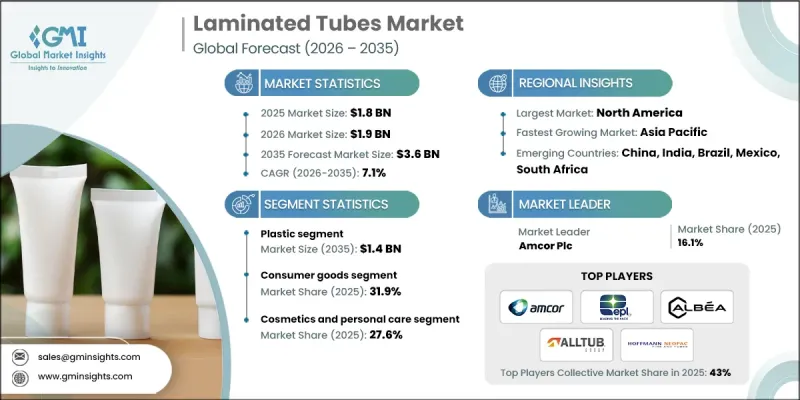

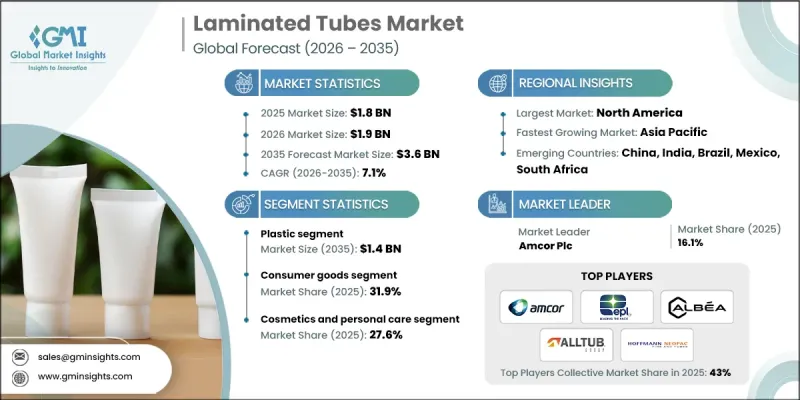

세계 라미네이트 튜브 시장은 2025년에 18억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 7.1%로 성장하여 36억 달러에 이를 것으로 예측됩니다.

시장 성장은 환경 책임에 대한 규제 기준의 엄격화와 소비자 의식 증가에 의해 지원됩니다. 기업은 순환형 경제의 목표에 부합하기 때문에 재활용 가능 소재와 생분해성 소재를 포함한 지속 가능한 포장 방법을 점점 채택하고 있습니다. 라미네이트 튜브는 재료 폐기물을 줄이고 재활용성을 향상시키기 위해 설계되었으며 브랜드가 지속가능성 목표를 달성함과 동시에 변화하는 소비자의 기대에 부응하는 데 도움이 됩니다. 또한 규제 대상 제품을 중심으로 안전하고 높은 배리어성, 규제 준수 포장 솔루션에 대한 수요가 높아지고 있는 것도 수요 증가의 요인입니다. 라미네이트 튜브는 습기, 산소, 외부 오염물질에 강한 내성을 제공하는 동시에 제어된 정확한 토출을 가능하게 합니다. 업계가 안전성, 보존 기간 연장, 규제 준수를 더욱 중시함에 따라 라미네이트 튜브 포장 수요가 계속 확대되고 있습니다. 지속적인 재료혁신과 제조기술의 향상은 다수의 최종 용도 분야에서 시장의 성장 전망을 더욱 강화하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 18억 달러 |

| 예측 금액 | 36억 달러 |

| CAGR | 7.1% |

플라스틱 부문은 2035년까지 14억 달러에 달할 것으로 예측됩니다. 경량성, 비용 효율, 유연성, 뛰어난 배리어 성능 등 소재 특성이 강한 수요를 지원하고 있습니다. 재생가능한 폴리머와 다층 구조에서의 지속적인 기술 진보로 수용이 확대되고 응용 범위가 넓어지고 있습니다.

소비재 부문은 2025년에 31.9%의 점유율을 차지했습니다. 성장은 내구성, 편의성, 시각적 매력을 결합한 포장 솔루션에 대한 수요에 의해 견인되고 있습니다. 사용자 경험, 선반에서의 시인성, 브랜드 차별화에 대한 주목 증가가 튜브 구조, 재료, 인쇄 기술의 혁신을 지속적으로 촉진하고 있습니다.

북미 라미네이트 튜브 시장은 2025년 30%의 점유율을 차지했습니다. 지역 수요는 프리미엄 및 맞춤형 포장 솔루션의 적극적인 채택, 지속가능성에 중점을 두고 첨단 패키징 제조업체와 세계 브랜드 소유자의 존재에 의해 지원되고 있으며, 이들은 함께 지속적인 제품 개발을 촉진하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 수익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속가능하고 환경친화적인 포장으로의 전환

- 퍼스널케어 및 화장품 업계의 성장

- 튜브 인쇄 기술의 진보

- 의약품 포장에 대한 수요 증가

- 업계의 잠재적 위험 및 과제

- 복잡한 재활용 프로세스

- 변동하는 원재료 가격

- 시장 기회

- 퍼스널케어 및 화장품 포장의 고부가가치화

- 에코 라벨과 브랜드 차별화

- 성장 촉진요인

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재의 기술 동향

- 신규기술

- 신규 비즈니스 모델

- 컴플라이언스 요건

- 지속가능성 대책

- 지속 가능한 재료의 평가

- 탄소발자국 분석

- 순환형 경제의 도입

- 지속가능성 인증 및 기준

- 지속가능성 ROI 분석

- 특허 및 지적재산 분석

- 지정학적 및 무역 동향

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴 아메리카

- 중동 및 아프리카

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무실적 비교

- 매출

- 영업이익률

- 연구개발

- 제품 포트폴리오 비교

- 제품 라인 범위

- 기술

- 혁신

- 지역별 전개 비교

- 글로벌 진출 범위

- 서비스 네트워크 커버리지

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더

- 도전자

- 추종자

- 틈새 기업

- 전략적 전망 매트릭스

- 재무실적 비교

- 주요 발전, 2021-2024

- 합병 및 인수

- 제휴 및 공동 사업

- 기술적 진보

- 확대 및 투자 전략

- 디지털 전환의 대처

- 신규/스타트업 경쟁의 동향

제5장 시장 추정 및 예측 : 재료별, 2022-2035

- 플라스틱

- 알루미늄

- 폴리포일

제6장 시장추정 및 예측 : 용량별, 2022-2035

- 50ml 미만

- 50ml-100ml

- 100ml-150ml

- 150ml-200ml

- 200ml 초과

제7장 시장 추정 및 예측 : 용도별, 2022-2035

- 화장품 및 퍼스널케어

- 스킨케어

- 헤어케어

- 구강케어

- 연고 및 크림

- 조미료 및 소스

- 식용 페이스트

- 접착제 및 실란트

- 기타

제8장 시장 추정 및 예측 : 최종 이용 산업별, 2022-2035

- 소비재

- 의약품

- 식음료

- 산업용

- 기타

제9장 시장 추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- 세계 주요 기업

- Amcor Plc

- Albea Group

- EPL Limited

- Hoffmann Neopac AG

- 지역별 주요 기업

- 북미

- CCL Industries Inc.

- Plastube Inc.

- Perfect Containers Group

- 유럽

- Alltub Group

- Pirlo GmbH & Co. KG

- Tubapack AS

- 아시아태평양

- Kyodo Printing(Vietnam) Co., Ltd.

- Antilla Propack

- BRK Packwell Private Limited.

- 북미

- 틈새 기업/디스 랩터

- Burhani Packaging

- CTLpack

- Huhtamaki Oyj

- Montebello Packaging

- Norway Pack

- Perfektup Ambalaj

- Prutha Packaging Pvt. Ltd.

- REGO

- Shreeji Enterprises

- STS Pack Holding

- Zeal Life Sciences Pvt. Ltd.

The Global Laminated Tubes Market was valued at USD 1.8 billion in 2025 and is estimated to grow at a CAGR of 7.1% to reach USD 3.6 billion by 2035.

Market growth is supported by stricter regulatory standards and rising consumer awareness related to environmental responsibility. Companies are increasingly adopting sustainable packaging approaches, including recyclable and biodegradable materials, to align with circular economy objectives. Laminated tubes are designed to reduce material waste and improve recyclability, helping brands meet sustainability goals while responding to evolving consumer expectations. Demand is also rising due to the need for secure, high-barrier, and compliant packaging solutions, particularly for regulated products. Laminated tubes offer strong resistance to moisture, oxygen, and external contaminants while enabling controlled and accurate dispensing. As industries place greater emphasis on safety, shelf-life extension, and regulatory compliance, laminated tube packaging continues to gain traction. Ongoing material innovation and improved manufacturing techniques further strengthen the market's growth outlook across multiple end-use sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 7.1% |

The plastic segment is expected to reach USD 1.4 billion by 2035. Strong demand is supported by the material's lightweight nature, cost efficiency, flexibility, and excellent barrier performance. Continuous advancements in recyclable polymers and multilayer structures are increasing acceptance and expanding application scope.

The consumer goods segment accounted for 31.9% share in 2025. Growth is driven by demand for packaging solutions that combine durability, convenience, and visual appeal. Increased focus on user experience, shelf visibility, and brand differentiation continues to encourage innovation in tube structure, materials, and printing technologies.

North America Laminated Tubes Market held a 30% share in 2025. Regional demand is supported by strong adoption of premium and customized packaging solutions, emphasis on sustainability, and the presence of advanced packaging manufacturers and global brand owners, which together promote continuous product development.

Key companies operating in the Global Laminated Tubes Market include Amcor Plc, CCL Industries Inc., Albea Group, EPL Limited, Alltub Group, Pirlo GmbH & Co. KG, Tubapack A.S., Plastube Inc., STS Pack Holding, CTLpack, BRK Packwell Private Limited, Antilla Propack, Burhani Packaging, Shreeji Enterprises, Prutha Packaging Pvt. Ltd., REGO, and Zeal Life Sciences Pvt. Ltd. Companies in the Global Laminated Tubes Market strengthen their market position through material innovation, sustainable product development, and expanded manufacturing capabilities. Firms focus on developing recyclable and lightweight tube structures that meet regulatory and environmental standards. Investment in advanced barrier technologies helps improve product protection and shelf life. Strategic partnerships with brand owners support customized packaging solutions and long-term contracts.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Material trends

- 2.2.2 Capacity trends

- 2.2.3 Application trends

- 2.2.4 End use industry trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward sustainable and eco-friendly packaging

- 3.2.1.2 Growth in personal care and cosmetics industry

- 3.2.1.3 Advancements in tube printing technology

- 3.2.1.4 Rising demand for pharmaceutical packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex recycling process

- 3.2.2.2 Fluctuating raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Premiumization of personal care and cosmetics packaging

- 3.2.3.2 Eco-labeling and brand differentiation

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Emerging business models

- 3.8 Compliance requirements

- 3.9 Sustainability measures

- 3.9.1 Sustainable materials assessment

- 3.9.2 Carbon footprint analysis

- 3.9.3 Circular economy implementation

- 3.9.4 Sustainability certifications and standards

- 3.9.5 Sustainability ROI analysis

- 3.10 Patent and IP analysis

- 3.11 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Mn & Mn Units)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Aluminum

- 5.4 Polyfoil

Chapter 6 Market Estimates and Forecast, By Capacity, 2022 - 2035 ($ Mn & Mn Units)

- 6.1 Key trends

- 6.2 Less than 50ml

- 6.3 50ml to 100ml

- 6.4 100ml to 150ml

- 6.5 150ml to 200ml

- 6.6 Above 200ml

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn & Mn Units)

- 7.1 Key trends

- 7.2 Cosmetics and personal care

- 7.2.1 Skin care

- 7.2.2 Hair care

- 7.2.3 Oral care

- 7.3 Ointments and creams

- 7.4 Condiments and sauces

- 7.5 Edible pastes

- 7.6 Adhesives and sealants

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use industry, 2022 - 2035 ($ Mn & Mn Units)

- 8.1 Key trends

- 8.2 Consumer goods

- 8.3 Pharmaceuticals

- 8.4 Food and beverages

- 8.5 Industrial

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn & Mn Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Amcor Plc

- 10.1.2 Albea Group

- 10.1.3 EPL Limited

- 10.1.4 Hoffmann Neopac AG

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 CCL Industries Inc.

- 10.2.1.2 Plastube Inc.

- 10.2.1.3 Perfect Containers Group

- 10.2.2 Europe

- 10.2.2.1 Alltub Group

- 10.2.2.2 Pirlo GmbH & Co. KG

- 10.2.2.3 Tubapack A.S.

- 10.2.3 APAC

- 10.2.3.1 Kyodo Printing (Vietnam) Co., Ltd.

- 10.2.3.2 Antilla Propack

- 10.2.3.3 BRK Packwell Private Limited.

- 10.2.1 North America

- 10.3 Niche Players / Disruptors

- 10.3.1 Burhani Packaging

- 10.3.2 CTLpack

- 10.3.3 Huhtamaki Oyj

- 10.3.4 Montebello Packaging

- 10.3.5 Norway Pack

- 10.3.6 Perfektup Ambalaj

- 10.3.7 Prutha Packaging Pvt. Ltd.

- 10.3.8 REGO

- 10.3.9 Shreeji Enterprises

- 10.3.10 STS Pack Holding

- 10.3.11 Zeal Life Sciences Pvt. Ltd.