|

시장보고서

상품코드

1913362

전기자동차 레인지 익스텐더 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2026-2035년)Electric Vehicle Range Extender Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

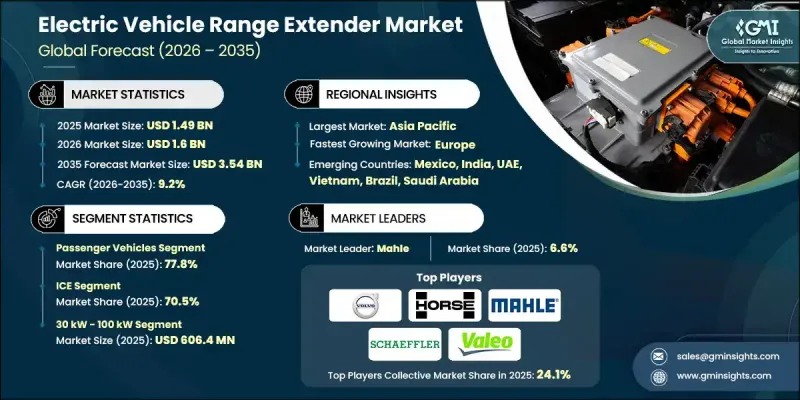

세계의 전기자동차 레인지 익스텐더 시장은 2025년에 14억 9,000만 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 9.2%로 성장할 전망이며, 35억 4,000만 달러에 이를 것으로 예측되고 있습니다.

세계의 전동모빌리티로의 전환 가속화가 시장 확대를 뒷받침하고 있으며, EV 판매량 증가가 주행 거리에 대한 우려를 해결하는 기술 수요를 직접적으로 높이고 있습니다. 공공 충전 네트워크가 개발되지 않은 지역에서는 레인지 익스텐더의 중요성이 커지고 있습니다. 기술 진보의 지속으로 현대의 레인지 익스텐더 시스템의 비용 효율성 및 성능이 향상되어 대규모 도입의 가능성이 높아지고 있습니다. 이러한 시스템은 차량 효율 향상, 환경 부하 저감, 주행 거리 연장에 기여하며, 개인 및 상용 이용 모두에서 전동 이동성의 매력을 높이고 있습니다. 한편, 배터리 분야의 혁신은 경쟁 압력을 낳고 있으며, 배터리 에너지 밀도의 향상과 급속 충전 능력의 향상에 의해 보조 동력 시스템에 대한 의존도가 저하되고 있습니다. 이러한 과제가 있음에도 불구하고 레인지 익스텐더는 장거리 이동의 제약을 해결하고 다양한 이용 사례에서의 EV의 보급을 촉진함으로써 시장 성장을 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 당초 시장 규모 | 14억 9,000만 달러 |

| 시장 규모 예측 | 35억 4,000만 달러 |

| CAGR | 9.2% |

승용차 부문은 2025년에 77.8%의 점유율을 차지했습니다. 충전 빈도의 감소는 편의성과 EV 소유에 대한 신뢰성을 높이기 위해 소비자는 일상적인 도시 및 교외에서의 사용에 있어서 항속 거리의 연장을 점점 중시하고 있습니다. 레인지 익스텐더의 통합은 항속 거리에 대한 불안과 관련된 초기 도입 장벽의 완화에 기여하여 전기 승용차가 세계적으로 강한 견인력을 얻을 수 있게 했습니다.

내연기관 기반 솔루션 부문은 2025년에 70.5%의 점유율을 차지했으며, 2026-2035년 CAGR 9.6%로 성장할 것으로 예측됩니다. 제조업체는 기술적 성숙도, 확립된 공급망 및 새로운 발전 대체 기술에 비해 낮은 개발 및 제조 비용으로 이러한 시스템을 지속적으로 지지하고 있습니다.

미국의 전기자동차 레인지 익스텐더 시장은 2025년 3억 970만 달러 규모에 달했습니다. 주 차원의 인센티브, 세제 우대 조치, 전기자동차에 대한 규제 측면의 지원이 국내 생산과 투자를 지속적으로 촉진하고 있으며, 미국 시장 성장을 강화하고 있습니다.

자주 묻는 질문

목차

제1장 분석 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 높아지는 소비자의 항속 거리 불안

- 전기 상용차 및 플릿 차량의 성장

- 신흥 시장에서의 전기자동차 보급 확대

- 지방 및 고속도로 연선에 있어서 충전 인프라의 부족

- 업계의 잠재적 위험 및 과제

- 급속 충전 인프라의 급속한 확대

- 배터리 에너지 밀도 향상 및 비용 저하

- 시장 기회

- 전기 트럭 및 밴용 레인지 익스텐더

- 기존 EV 플랫폼용 개조 솔루션

- 인프라 정비의 갭이 있는 신흥 시장

- 수소 및 e-연료 기반 범위 익스텐더 시스템

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 캘리포니아주 대기자원국(CARB) 선진 클린카 II(ACC II)

- EPA 온실가스(GHG) 기준

- IRA(인플레이션 삭감법) 세액 공제

- 유럽

- 유로 7 기준

- 유틸리티 계수(UF) 곡선 조정

- 유럽위원회

- 국제 클린 수송 평의회

- 아시아태평양

- 중국의 신에너지차정책

- 인도의 FAME-III(초안)

- 듀얼 크레딧 제도(CAFC와 NEV)

- 라틴아메리카

- 브라질의 무버 프로그램

- CONAMA(Conselho Nacional do Meio Ambiente)

- 중동 및 아프리카

- GSO(만안 표준화 기구) 규격

- 아랍에미리트(UAE)(UAE) 국가 전기자동차 정책

- 사우디아라비아 SASO 규제

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신 동향

- 현재 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출 및 수입

- 지속가능성 및 환경 영향

- 환경 영향 평가

- 사회적 영향 및 지역사회에 대한 공헌

- 거버넌스 및 기업의 사회적 책임

- 지속 가능한 금융 및 투자 동향

- 각 지역의 인프라 정비 상황 평가

- 충전 인프라 정비 상황 : 지역별

- 레인지 익스텐더 시스템용 연료 공급 상황

- 도시와 도시 간 인프라 격차

- 레인지 익스텐더 수요 전망에 미치는 영향

- 비용 내역 분석

- 엔진 및 에너지 생성 유닛의 단가

- 발전기 및 전기 및 전자 기기의 비용

- 연료 시스템 및 배출 가스 제어 비용

- 열 관리 및 냉각 시스템의 비용

- 제조 및 조립 비용

- 사례 연구

- 전망 및 기회

제4장 경쟁 구도

- 서문

- 기업별 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 레인지 익스텐더별(2022-2035년)

- ICE(내연 기관)

- 디젤

- 가솔린

- 로터리

- 대체 연료전지

- 천연가스

- 수소

- 바이오연료

제6장 시장 추계 및 예측 : 출력별(2022-2035년)

- 30kW 미만

- 30kW-100kW

- 100kW 이상

제7장 시장 추계 및 예측 : 컴포넌트별(2022-2035년)

- 배터리 팩

- 파워 컨버터

- 전기 모터

- 발전기

- 기타

제8장 시장 추계 및 예측 : 차량별(2022-2035년)

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 이륜차 및 삼륜차

제9장 시장 추계 및 예측 : 용도별(2022-2035년)

- 법인용 및 물류용 차량

- 라이드 쉐어링, 택시 및 렌터카 서비스

- 개인용 차량

제10장 시장 추계 및 예측 : 판매 채널별(2022-2035년)

- OEM

- 애프터마켓

제11장 시장 추계 및 예측 : 지역별(2022-2035년)

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- 세계 기업

- ZF Group

- Stellantis

- Hyundai Motor

- Volvo

- Mazda Motor

- BYD

- Li Auto

- Huawei

- Leapmotor

- Magna

- MAHLE Powertrain

- Ballard

- 지역 기업

- AVL

- FEV Group

- Plug Power

- Scout Motors

- Avatr Technologies

- Deepal

- Bosch Engineering

- XPeng Motors

- 신흥 기업

- Obrist Powertrain

- Delta Motorsports

- Ceres Power

- Symbio

- EP Tender

The Global Electric Vehicle Range Extender Market was valued at USD 1.49 billion in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 3.54 billion by 2035.

The accelerating shift toward electric mobility worldwide continues to support market expansion, as rising EV sales directly increase demand for technologies that address driving range concerns. Range extenders are gaining relevance in regions where public charging networks remain underdeveloped. Ongoing technological progress has improved the cost efficiency and performance of modern range extender systems, making them more viable for large-scale adoption. These systems help improve vehicle efficiency, reduce environmental impact, and extend driving distance, which strengthens the appeal of electric mobility for both private and commercial use. At the same time, innovation within the battery sector is creating competitive pressure, as higher battery energy density and faster charging capabilities reduce dependence on auxiliary power systems. Despite these challenges, range extenders continue to support market growth by addressing long-distance travel limitations and enabling wider EV acceptance across diverse use cases.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.49 Billion |

| Forecast Value | $3.54 Billion |

| CAGR | 9.2% |

The passenger vehicles segment accounted for 77.8% share in 2025. Consumers increasingly prioritize extended driving range for everyday urban and suburban usage, as reduced charging frequency improves convenience and confidence in EV ownership. Range extender integration has helped ease earlier adoption barriers related to range anxiety, allowing electric passenger vehicles to gain stronger global traction.

The internal combustion engine-based solutions segment held 70.5% share in 2025 and is forecast to grow at a CAGR of 9.6% from 2026 to 2035. Manufacturers continue to favor these systems due to their technical maturity, established supply chains, and lower development and manufacturing costs compared to newer power generation alternatives.

U.S. Electric Vehicle Range Extender Market garnered USD 309.7 million in 2025. State-level incentives, tax benefits, and regulatory support for electric vehicles continue to encourage domestic production and investment, strengthening market growth across the country.

Key companies active in the Global Electric Vehicle Range Extender Market include ZF Group, Hyundai Mobis, Mahle, Mazda, AVL, Li Auto, Schaeffler, AB Volvo, Valeo, and Horse Powertrain. Companies operating in the Electric Vehicle Range Extender Market focus on technology optimization, cost reduction, and strategic partnerships to reinforce their market position. Many players invest heavily in research and development to improve efficiency, durability, and system integration. Collaboration with vehicle manufacturers allows suppliers to align product design with evolving EV platforms. Firms also prioritize scalable manufacturing to meet rising demand while maintaining competitive pricing. Geographic expansion remains a key strategy, with companies strengthening regional production and distribution networks. In addition, players emphasize compliance with emission regulations and alignment with government incentive programs.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Range extender

- 2.2.3 Power Output

- 2.2.4 Component

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.2.7 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer range anxiety

- 3.2.1.2 Growth in electric commercial and fleet vehicles

- 3.2.1.3 Expansion of EV adoption in emerging markets

- 3.2.1.4 Limited charging infrastructure in rural and highway areas

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid expansion of fast-charging infrastructure

- 3.2.2.2 Increasing battery energy density and cost decline

- 3.2.3 Market opportunities

- 3.2.3.1 Range extenders for electric trucks and vans

- 3.2.3.2 Retrofitting solutions for existing EV platforms

- 3.2.3.3 Emerging markets with infrastructure gaps

- 3.2.3.4 Hydrogen and e-fuel-based range extender systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 CARB Advanced Clean Cars II (ACC II)

- 3.4.1.2 EPA Greenhouse Gas (GHG) Standards

- 3.4.1.3 IRA (Inflation Reduction Act) Tax Credits

- 3.4.2 Europe

- 3.4.2.1 Euro 7 Standards

- 3.4.2.2 Utility Factor (UF) Curve Adjustments

- 3.4.2.3 European Commission

- 3.4.2.4 International Council on Clean Transportation

- 3.4.3 Asia Pacific

- 3.4.3.1 China’s New Energy Vehicle Policy

- 3.4.3.2 India’s FAME-III (Draft)

- 3.4.3.3 Dual Credit System (CAFC & NEV)

- 3.4.4 Latin America

- 3.4.4.1 Brazil’s Mover Program

- 3.4.4.2 CONAMA (Conselho Nacional do Meio Ambiente)

- 3.4.5 Middle East & Africa

- 3.4.5.1 GSO (Gulf Standardization Organization) Standards

- 3.4.5.2 UAE National EV Policy

- 3.4.5.3 Saudi SASO Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Regional infrastructure readiness assessment

- 3.11.1 Charging infrastructure maturity by region

- 3.11.2 Fuel availability for range extender systems

- 3.11.3 Urban versus intercity infrastructure gaps

- 3.11.4 Impact on range extender demand outlook

- 3.12 Cost breakdown analysis

- 3.12.1 Engine or energy generation unit cost

- 3.12.2 Generator and power electronics cost

- 3.12.3 Fuel system and emissions control cost

- 3.12.4 Thermal management and cooling system cost

- 3.12.5 Manufacturing and assembly cost

- 3.13 Case studies

- 3.14 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Range Extender, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 ICE

- 5.2.1 Diesel

- 5.2.2 Gasoline

- 5.2.3 Rotary

- 5.3 Alternate fuel cell

- 5.3.1 Natural gas

- 5.3.2 Hydrogen

- 5.3.3 Biofuel

Chapter 6 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Less than 30 kW

- 6.3 30 kW - 100 kW

- 6.4 Above 100 kW

Chapter 7 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Battery pack

- 7.3 Power converter

- 7.4 Electric motor

- 7.5 Generator

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Sedan

- 8.2.2 SUV

- 8.2.3 Hatchback

- 8.3 Commercial vehicles

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

- 8.4 Two-Wheelers & Three-Wheelers

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Corporate/logistics fleet

- 9.3 Ridesharing/taxi/rental services

- 9.4 Personal vehicles

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Singapore

- 11.4.7 Malaysia

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 ZF Group

- 12.1.2 Stellantis

- 12.1.3 Hyundai Motor

- 12.1.4 Volvo

- 12.1.5 Mazda Motor

- 12.1.6 BYD

- 12.1.7 Li Auto

- 12.1.8 Huawei

- 12.1.9 Leapmotor

- 12.1.10 Magna

- 12.1.11 MAHLE Powertrain

- 12.1.12 Ballard

- 12.2 Regional companies

- 12.2.1 AVL

- 12.2.2 FEV Group

- 12.2.3 Plug Power

- 12.2.4 Scout Motors

- 12.2.5 Avatr Technologies

- 12.2.6 Deepal

- 12.2.7 Bosch Engineering

- 12.2.8 XPeng Motors

- 12.3 Emerging companies

- 12.3.1 Obrist Powertrain

- 12.3.2 Delta Motorsports

- 12.3.3 Ceres Power

- 12.3.4 Symbio

- 12.3.5 EP Tender