|

시장보고서

상품코드

1665194

자동차 전동 컴프레서 시장(2025-2034년) : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측Automotive E-Compressor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

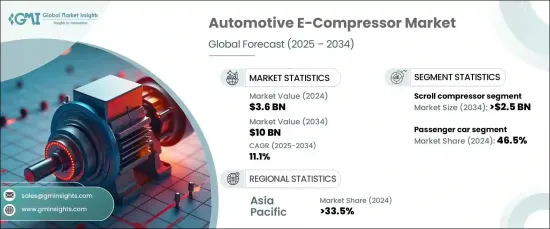

2024년 자동차 전동 컴프레서 세계 시장 규모는 36억 달러를 달성하였고 2025-2034년의 CAGR은 11.1%로 예상되어 현저한 성장을 전망하고 있습니다.

이러한 성장은 최신 전기자동차(EV) 및 하이브리드 자동차에 필수적인 구성 요소가 되고 있는 첨단 열 관리 시스템에 대한 수요 증가에 크게 뒷받침되었습니다. 이러한 자동차가 계속 발전함에 따라 배터리, 전기 모터, 캐빈, 파워 일렉트로닉스와 같은 중요한 부품의 온도 관리는 최적의 성능을 발휘하기 위해 점점 더 중요해지고 있습니다. 이 시스템에서 중요한 역할을 하는 자동차 전동 컴프레서는 에너지 효율과 내연기관(ICE)을 동력원으로 하는 기존의 기계식 컴프레서에 대한 의존도를 크게 줄일 수 있는 능력으로 높게 평가되고 있습니다. 이 기술 변화는 자동차산업에서 발생하는 지속 가능하고 에너지 효율적인 솔루션에 대한 폭넓은 추진과 일치하여 시장 성장을 더욱 가속화하고 있습니다.

자동차 전동 컴프레서 시장은 스크롤, 로터리, 레시프로, 스크류, 기타 등 컴프레서 유형별로 구분됩니다. 2024년에는 스크롤 컴프레서 부문이 33% 시장 점유율을 달성하였고 2034년까지 25억 달러를 창출할 것으로 예측됩니다. 스크롤 컴프레서는 신뢰성, 저소음 동작, 컴팩트한 디자인으로 특히 선호되며 최신 자동차 용도에 이상적입니다. 이러한 특징은 공간 효율성과 성능이 가장 중시되는 전기자동차 및 하이브리드 자동차에서 사용하기에 특히 적합합니다. 스크롤 컴프레서 기술에는 두 개의 나선형 스크롤이 있으며 하나는 정지 상태를 유지하고 다른 하나는 원을 그리듯이 움직여 냉매를 압축합니다. 이 프로세스는 EV 및 하이브리드 차량의 편안함과 기능성을 향상시키는 중요한 요소인 효율 향상 및 소음 수준 감소를 보장합니다.

| 시장 범위 | |

|---|---|

| 시작년 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 36억 달러 |

| 예측금액 | 100억 달러 |

| CAGR | 11.1% |

시장을 차종별로 보면, 자동차 전동 컴프레서 시장은 승용차, 상용차, 오프하이웨이 차로 나눌 수 있습니다. 2024년에는 승용차가 46.5% 시장 점유율을 달성하여 최대 부문이 되었습니다. 이러한 이점은 전기자동차와 하이브리드 자동차의 인기가 높아짐에 따라 커지고 있으며, 승용차는 환경친화적인 운송 솔루션으로의 전환을 이끌고 있습니다. 이러한 자동차는 전동 컴프레서가 기존의 벨트 구동 압축기를 대체하는 에너지 효율적인 옵션을 제공하여 에너지 소비를 최소화하면서 더 나은 열 관리를 보장합니다. 엔진이 에어컨을 구동하는 내연기관차와는 달리, 전기자동차는 차량의 배터리와 전기 모터를 동력원으로 하는 전동 컴프레서에 의존합니다.

아시아태평양은 2024년에 자동차 전동 컴프레서 세계 시장에서 33.5%의 점유율을 차지했으며, 이 지역의 전기자동차산업의 급속한 확대에 견인되었습니다. 특히 중국은 보조금, 세제 우대조치, 이산화탄소 배출량 감축을 목적으로 한 시책 등 정부의 강력한 대처에 힘입어 전기차의 최대 생산국 및 소비국이 되었습니다. BYD, NIO, XPeng, Geely 등 중국의 대기업 자동차 업체가 전기자동차의 개발과 판매를 주도하고 있으며, 이 지역의 자동차 전동 컴프레서 시장은 향후 수년간 지속적으로 성장할 전망입니다.

목차

제1장 조사 방법 및 조사 범위

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 기본 추정 및 계산

- 기준연도 산출

- 시장 추정의 주요 동향

- 예측 모델

- 1차 조사 및 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 정의

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 공급자의 상황

- 원료 공급업체

- 부품 제조업체

- 기술 제공업체

- 최종 사용자

- 이익률 분석

- 기술 및 혁신 전망

- 비용 내역

- 주요 뉴스 및 대처

- 규제 상황

- 가격 분석

- 영향요인

- 성장 촉진요인

- EV 도입의 급증

- 컴프레서 기술의 진보

- 첨단 기능에 대한 소비자 수요

- 열 관리 시스템에 대한 주목 증가

- 산업의 잠재적 리스크 및 과제

- 전동 컴프레서의 높은 초기 비용

- 기술적 및 통합적 과제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 컴프레서별(2021-2034년)

- 주요 동향

- 스크롤

- 로터리

- 레시프로

- 스크류

- 기타

제6장 시장 추정 및 예측 : 냉각 능력별(2021-2034년)

- 주요 동향

- 저용량(5kW 이하)

- 중용량(5-10 kW)

- 대용량(10kW 이상)

제7장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 캐빈 에어컨

- 배터리 열 관리

- 파워트레인 냉각

- 전동 드라이브트레인 냉각

- 기타

제8장 시장 추정 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 전기자동차

- 하이브리드

제9장 시장 추정 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- LCV

- HCV

- 오프하이웨이 자동차

제10장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- Bosch

- Boyard Compressor

- Denso

- Elgi Equipment

- Gardner Denver

- Garrett

- Guchen Industry

- Hanon Systems

- Highly Marelli

- Infineon

- Mahle

- Mitsubishi

- Novosense

- Sanden

- Siroco

- TCCI

- Toyota

- Valeo

- Vikas Group

- ZF Friedrichshafen

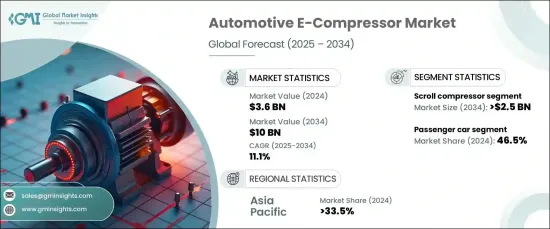

The Global Automotive E-Compressor Market, valued at USD 3.6 billion in 2024, is set to experience remarkable growth, with an expected CAGR of 11.1% from 2025 to 2034. This growth is largely driven by the increasing demand for advanced thermal management systems, which are becoming an essential component in modern electric vehicles (EVs) and hybrids. As these vehicles continue to evolve, managing the temperature of critical components such as batteries, electric motors, cabins, and power electronics has become increasingly important for optimal performance. Automotive e-compressors, which play a pivotal role in this system, are highly valued for their energy efficiency and their ability to significantly reduce reliance on traditional mechanical compressors powered by internal combustion engines (ICEs). This shift in technology aligns with the broader push towards sustainable and energy-efficient solutions in the automotive industry, further accelerating market growth.

The market for automotive e-compressors is segmented by compressor type, including scroll, rotary, reciprocating, screw, and others. In 2024, the scroll compressor segment commanded a substantial 33% market share and is projected to generate USD 2.5 billion by 2034. Scroll compressors are particularly favored for their reliability, quiet operation, and compact design, making them ideal for modern automotive applications. These features make them especially suitable for use in electric and hybrid vehicles, where space efficiency and performance are paramount. The technology behind scroll compressors involves two spiral-shaped scrolls, one of which remains stationary while the other moves in a circular motion to compress refrigerant. This process ensures high efficiency and reduced noise levels, critical factors for improving the comfort and functionality of EVs and hybrids.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $10 Billion |

| CAGR | 11.1% |

Looking at the market from a vehicle type perspective, the automotive e-compressor market is divided into passenger cars, commercial vehicles, and off-highway vehicles. In 2024, passenger cars represented the largest segment with a 46.5% market share. This dominance is largely due to the increasing popularity of electric and hybrid vehicles, with passenger cars leading the transition to more eco-friendly transportation solutions. In these vehicles, e-compressors offer a more energy-efficient alternative to traditional belt-driven compressors, ensuring better thermal management while minimizing energy consumption. Unlike ICE-powered vehicles, where the engine drives the air conditioning, electric vehicles rely on e-compressors powered by the vehicle's battery and electric motor.

Asia Pacific held a 33.5% share of the global automotive e-compressor market in 2024, driven by rapid expansion in the region's electric vehicle industry. China, in particular, has become the largest producer and consumer of electric vehicles, supported by strong government initiatives including subsidies, tax incentives, and policies aimed at reducing carbon emissions. With major Chinese automakers like BYD, NIO, XPeng, and Geely leading the charge in EV development and sales, the region's automotive e-compressor market is poised for continued growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Technology providers

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Cost breakdown

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Surge in EV adoption

- 3.9.1.2 Advancements in compressor technology

- 3.9.1.3 Consumer demand for advanced features

- 3.9.1.4 Increased focus on thermal management systems

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial cost of electric compressors

- 3.9.2.2 Technological and integration challenges

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Compressor, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Scroll

- 5.3 Rotary

- 5.4 Reciprocating

- 5.5 Screw

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Cooling Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Low capacity (Below 5 kW)

- 6.3 Medium capacity (5-10 kW)

- 6.4 High capacity (Above 10 kW)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Cabin air conditioning

- 7.3 Battery thermal management

- 7.4 Powertrain cooling

- 7.5 Electric drivetrain cooling

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Electric

- 8.3 Hybrid

Chapter 9 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger cars

- 9.2.1 Sedan

- 9.2.2 SUV

- 9.2.3 Hatchback

- 9.3 Commercial vehicle

- 9.3.1 LCV

- 9.3.2 HCV

- 9.4 Off highway vehicle

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Bosch

- 11.2 Boyard Compressor

- 11.3 Denso

- 11.4 Elgi Equipment

- 11.5 Gardner Denver

- 11.6 Garrett

- 11.7 Guchen Industry

- 11.8 Hanon Systems

- 11.9 Highly Marelli

- 11.10 Infineon

- 11.11 Mahle

- 11.12 Mitsubishi

- 11.13 Novosense

- 11.14 Sanden

- 11.15 Siroco

- 11.16 TCCI

- 11.17 Toyota

- 11.18 Valeo

- 11.19 Vikas Group

- 11.20 ZF Friedrichshafen