|

시장보고서

상품코드

1665205

자동차 지능형 안테나 모듈 시장(2025-2034년) : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측Automotive Intelligent Antenna Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

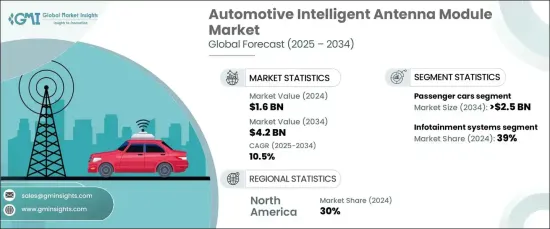

자동차 지능형 안테나 모듈 세계 시장은 2024년에 16억 달러로 평가되었으며, 2025-2034년에 걸쳐 10.5%의 연평균 복합 성장률(CAGR)로 견조하게 성장할 것으로 예측하고 있습니다.

이러한 현저한 성장은 자율주행차와 ADAS(첨단 운전자 보조 시스템)의 도입이 증가하고 있는 추세와 일치하고 있습니다. 이러한 기술이 현대의 이동성 솔루션에 필수적이 됨에 따라, 지능형 안테나 모듈은 차세대 자동차에 필요한 원활한 통신과 견고한 데이터 전송 기능을 촉진하는 중요한 구성 요소로 부상하고 있습니다.

자동차 연결성과 인포테인먼트 솔루션에 대한 수요 증가가 시장을 더욱 강화하고 있습니다. 오늘날의 소비자는 실시간 네비게이션, 음성 제어 기능, 블루투스나 Wi-Fi를 통한 스마트폰과의 간편한 연계 등의 기능을 갖춘 커넥티드 허브로서 자동차가 동작할 것을 기대하고 있습니다. 지능형 안테나 모듈은 이러한 첨단 시스템의 백본으로, 중단 없는 연결성을 확보하고 기술에 익숙한 운전자의 기대에 부응합니다. 스마트한 커넥티드카로의 이동이 진행되고 있는 가운데, 진화하는 소비자의 기호와 보조를 맞추고 우수한 차내 경험을 제공하는 데에 이러한 모듈의 역할이 강조되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작년 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 16억 달러 |

| 예측금액 | 42억 달러 |

| CAGR | 10.5% |

시장은 차종별로 승용차와 상용차로 구분됩니다. 2024년에는 승용차가 65%의 점유율을 차지하였고 2034년에는 25억 달러에 달할 것으로 예측됩니다. 승용차는 스마트 네비게이션, 미디어 재생, 실시간 교통 정보 기능을 제공하고 연결성을 높이는 지능형 안테나 모듈에 대한 의존도를 높이고 있습니다. 맞춤화되고 몰입감이 있는 차내 경험을 요구하는 소비자 수요 증가가 승용차에서 이러한 모듈의 채용을 지속 추진하여 최신 자동차에게 중요한 기능으로서의 역할을 강화하고 있습니다.

용도별로는 차량 간(V2V) 통신, 텔레매틱스, 인포테인먼트 시스템, ADAS, 차량과 도로 인프라 간(V2I) 통신이 포함됩니다. 2024년에는 음성 어시스턴트와 클라우드 기반 기능의 통합이 진행되고 있는 인포테인먼트 시스템이 시장 점유율의 39%를 차지했습니다. 지능형 안테나 모듈은 핸즈프리 작업, 원활한 미디어 재생, 지속적인 업데이트에 필요한 안정적인 연결성을 제공하며 첨단 인포테인먼트 솔루션에 필수적입니다.

북미 시장은 자율주행차 기술의 진보에 힘입어 2024년 세계 점유율의 30%를 차지했습니다. 이 지역은 자율주행차의 테스트와 배치로 시장을 주도하고 있으며, 이는 지능형 안테나 모듈 수요를 높이고 있습니다. 이 모듈은 중요한 V2X(Vehicle-to-Everything) 통신, GPS, 레이더 시스템, 원활한 데이터 전송을 가능하게 하며, 북미에서 자율 주행 시스템의 안전성, 효율성 및 신뢰성을 보장합니다. 이 지역의 지속적인 혁신은 지능형 안테나 기술을 채택하는 리더로서의 지위를 강화하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 기본 추정 및 계산

- 기준연도 산출

- 시장 추정의 주요 동향

- 예측 모델

- 1차 조사 및 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 범위 및 정의

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- Tier 1 공급업체

- 통신 제공업체

- 하이테크 기업 및 소프트웨어 제공업체

- 자동차 연결성 및 인프라 제공업체

- 유통업체

- 최종 사용자

- 공급자의 상황

- 이익률 분석

- 기술 혁신의 상황

- 특허 분석

- 주요 뉴스 및 이니셔티브

- 규제 상황

- 가격 분석

- 영향요인

- 성장 촉진요인

- 커넥티드카 및 자율주행차의 채용 확대

- 5G 네트워크 및 V2X 통신 기술의 전개

- 인포테인먼트 및 텔레매틱스 기능에 대한 소비자 수요 증가

- 자동차의 안전성과 연결성을 촉진하는 엄격한 규제

- 산업의 잠재적 리스크 및 과제

- 높은 비용 및 통합 복잡성

- 신호 간섭 및 네트워크 신뢰성 문제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 모듈별(2021-2034년)

- 주요 동향

- 5G

- V2X 통신

- 멀티밴드

- MIMO

- Wi-Fi/Bluetooth

제6장 시장 추정 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 안테나

- 신호프로세서

- 제어 유닛

- 고주파(RF) 유닛

- 필터

제7장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 텔레매틱스

- 인포테인먼트 시스템

- ADAS

- 차량 간(V2V)

- 차량과 도로 인프라 간(V2I)

제8장 시장 추정 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 내연기관

- 전기자동차

- 배터리 전기자동차(BEV)

- 플러그인 하이브리드 자동차(PHEV)

- 하이브리드 전기자동차(HEV)

제9장 시장 추정 및 예측 : 자동차별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV

- 기타

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제10장 시장 추정 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제11장 시장 예측 : 지역별 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제12장 기업 프로파일

- Antenova

- Aptiv

- Autotalks

- Continental

- Denso

- Ficosa

- Harman International

- Harxon

- Hella GmbH

- Hirschmann Car Communication

- Laird Connectivity

- Magna

- Mikros Technologies

- Pulse Electronics

- Robert Bosch

- Taoglas

- TE Connectivity

- Texas Instruments

- Valeo

The Global Automotive Intelligent Antenna Module Market, valued at USD 1.6 billion in 2024, is forecasted to grow at a robust CAGR of 10.5% between 2025 and 2034. This remarkable growth aligns with the increasing deployment of autonomous vehicles and advanced driver assistance systems (ADAS). As these technologies become integral to modern mobility solutions, intelligent antenna modules emerge as a critical component, facilitating seamless communication and robust data transfer capabilities required for next-generation vehicles.

The growing demand for in-car connectivity and infotainment solutions further propels the market. Today's consumers expect vehicles to operate as connected hubs equipped with features like real-time navigation, voice-controlled functionalities, and effortless smartphone integration via Bluetooth and Wi-Fi. Intelligent antenna modules are the backbone of these advanced systems, ensuring uninterrupted connectivity and meeting the expectations of tech-savvy drivers. The ongoing shift toward smart, connected vehicles underscores the role of these modules in delivering superior in-car experiences, keeping pace with evolving consumer preferences.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 10.5% |

The market is segmented by vehicle type into passenger cars and commercial vehicles. In 2024, passenger cars dominated the market with a 65% share and are projected to generate USD 2.5 billion by 2034. Passenger vehicles increasingly rely on intelligent antenna modules for enhanced connectivity, offering smart navigation, media streaming, and real-time traffic updates. Rising consumer demand for personalized and immersive in-car experiences continues to fuel the adoption of these modules in passenger cars, solidifying their role as a key feature in modern vehicles.

By application, the market includes vehicle-to-vehicle (V2V), telematics, infotainment systems, ADAS, and vehicle-to-infrastructure (V2I) communication. In 2024, infotainment systems accounted for 39% of the market share, driven by the growing integration of voice assistants and cloud-based features. Intelligent antenna modules provide the reliable connectivity required for hands-free operations, seamless media streaming, and continuous updates, making them indispensable for advanced infotainment solutions.

The North American market accounted for 30% of the global share in 2024, underpinned by advancements in autonomous vehicle technology. The region leads in the testing and deployment of self-driving cars, amplifying the demand for intelligent antenna modules. These modules enable critical vehicle-to-everything (V2X) communication, GPS, radar systems, and seamless data transfer, ensuring the safety, efficiency, and reliability of autonomous systems in North America. The continued innovation in this region positions it as a leader in the adoption of intelligent antenna technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Tier 1 suppliers

- 3.1.2 Telecommunications providers

- 3.1.3 Tech companies and software providers

- 3.1.4 Automotive connectivity & infrastructure provider

- 3.1.5 Distributors

- 3.1.6 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising adoption of connected and autonomous vehicles

- 3.9.1.2 Deployment of 5G networks and V2X communication technologies

- 3.9.1.3 Increasing consumer demand for infotainment and telematics features

- 3.9.1.4 Stringent regulations promoting vehicle safety and connectivity

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High costs and complexity of integration

- 3.9.2.2 Signal interference and network reliability issues

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Module, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 5G

- 5.3 V2X communication

- 5.4 Multiband

- 5.5 MIMO

- 5.6 Wi-Fi/Bluetooth

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Antennas

- 6.3 Signal processors

- 6.4 Control units

- 6.5 Radio Frequency (RF) Units

- 6.6 Filters

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Telematics

- 7.3 Infotainment systems

- 7.4 ADAS

- 7.5 Vehicle-to-Vehicle (V2V)

- 7.6 Vehicle-to-Infrastructure (V2I)

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Electric

- 8.3.1 Battery Electric Vehicles (BEV)

- 8.3.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 8.3.3 Hybrid Electric Vehicles (HEV)

Chapter 9 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger cars

- 9.2.1 Sedans

- 9.2.2 Hatchbacks

- 9.2.3 SUVs

- 9.2.4 Others

- 9.3 Commercial vehicles

- 9.3.1 Light Commercial Vehicles (LCVs)

- 9.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Antenova

- 12.2 Aptiv

- 12.3 Autotalks

- 12.4 Continental

- 12.5 Denso

- 12.6 Ficosa

- 12.7 Harman International

- 12.8 Harxon

- 12.9 Hella GmbH

- 12.10 Hirschmann Car Communication

- 12.11 Laird Connectivity

- 12.12 Magna

- 12.13 Mikros Technologies

- 12.14 Pulse Electronics

- 12.15 Robert Bosch

- 12.16 Taoglas

- 12.17 TE Connectivity

- 12.18 Texas Instruments

- 12.19 Valeo