|

시장보고서

상품코드

1665315

육상 원격 조종식 포탑 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Land-Based Remote Weapon Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

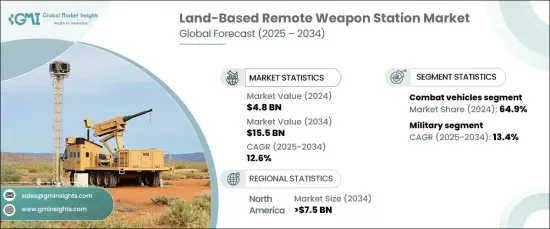

세계의 육상 원격 조종식 포탑 시장은 2024년에는 48억 달러로 평가되었고, 2025년부터 2034년까지 CAGR은 12.6%로 견조한 성장이 전망되고 있습니다. 시장 성장의 주요 원동력이 되고 있는 것은 선진적 방위 시스템에 대한 수요 증가와, 군비의 근대화가 진행되고 있는 것입니다. 각국이 전투의 유효성과 부대의 안전성을 높이는 것을 우선하는 가운데, 자동화된 원격 조작 무기 시스템의 채용이 현대 전쟁의 형태를 바꾸고 있습니다. 이러한 시스템은 뛰어난 정확성을 제공하고 운영자의 위험을 줄이고 진화하는 전투 전략에서 중요한 역할을 수행합니다.

시장은 플랫폼별로 분류되어 전투 차량이 선도하였고 2024년에는 64.9%의 압도적 점유율을 차지했습니다. 이 부문은 강화된 화력, 상황 인식, 새로운 위협으로부터의 보호에 대한 요구가 강화됨에 따라 계속 확대되고 있습니다. 전투 차량에 통합된 원격 조작 포탑(RCWS)을 통해 운영자는 차량에 안전하게 머무르고 높은 정확도로 목표를 공격할 수 있습니다. 이러한 시스템은 공격력과 방어력을 모두 제공하는 중요한 역할을 하며 현대의 장갑 플랫폼에 필수적인 요소가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 48억 달러 |

| 예측 금액 | 155억 달러 |

| CAGR | 12.6% |

용도별로 육상 원격 조종식 포탑 시장은 군사 부문과 국토 안보 부문으로 나뉩니다. 군사 부문이 가장 빠르게 성장하고 있으며, 2034년 CAGR은 13.4%로 예상됩니다. 전력 보호, 정밀 조준, 전체적인 운영 효율에 대한 수요가 이 성장의 원동력이 되고 있습니다. 원격 조종식 포탑은 장갑차, 방위 트럭 및 고정 군사 시설의 중요한 구성 요소입니다. 이러한 시스템은 모니터링과 조준의 정확성을 향상시킬 뿐만 아니라 대응 시간을 개선하고 동시에 적대적인 환경에 노출되는 인력을 최소화합니다. 그 광범위한 배치는 부대의 안전과 전투 능력을 높이는 데 중요한 역할을 한다는 것을 강조합니다.

북미에서는 육상 원격 조종식 포탑 시장이 2034년까지 75억 달러에 이를 것으로 예측됩니다. 이 성장의 원동력은 엄청난 국방 지출과 군사 현대화에 대한 지속적인 투자입니다. 특히 미국은 첨단 원격조작 시스템을 장갑차 및 방위 인프라에 통합함으로써 주도권을 잡고 있습니다. 이러한 시스템에서 인공지능과 자동화의 이용이 진행됨에 따라 기술 혁신이 더욱 촉진되고 조준 능력이 강화되어 운영효율이 향상되고 있습니다. 자율 방위 기술에 대한 지속적인 투자는 이 지역의 방위 태세를 강화하고 진화하는 안보 과제를 해결합니다.

목차

제1장 조사 방법 및 조사 범위

- 시장 범위 및 정의

- 기본 추정 및 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 데이터

- 유료 정보원

- 공적 정보원

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 변혁

- 장래 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스 및 대처

- 규제 상황

- 영향 요인

- 성장 촉진요인

- 현대전에서의 정밀 조준 수요 증가

- 선진적 육상 방위 시스템에 대한 군사 투자 증가

- 병사의 안전을 확보하기 위한 원격 조작 시스템 채용 증가

- 무기 시스템의 상호 운용성과 효율성을 높이는 기술 진보

- 지정학적 긴장이 첨단 군사 장비의 조달 촉진

- 산업의 잠재적 리스크 및 과제

- 첨단 무기 시스템의 높은 개발 및 통합 비용

- 세계 시장 기회에 영향을 미치는 규제와 수출의 과제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 플랫폼별(2021-2034년)

- 주요 동향

- 전투 차량

- 주력 탱크

- 보병 전투 차량

- 장갑 전투 차량

- 무인 지상 차량

- 기타

- 고정 구조물

제6장 시장 추정 및 예측 : 무기 유형별(2021-2034년)

- 주요 동향

- 치사성 무기

- 소구경

- 5.56mm

- 7.62mm

- 12.7mm

- 중구경

- 20mm

- 25mm

- 30mm

- 40mm

- 소구경

- 비치사성 무기

제7장 시장 추정 및 예측 : 모빌리티별(2021-2034년)

- 주요 동향

- 고정

- 이동

제8장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 군사

- 국토 안보

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Aselsan AS

- BAE Systems

- Bharat Electronics Limited(BEL)

- Copenhagen Sensor Technology

- Elbit Systems Ltd.

- EVPU Defense

- FN Herstal

- General Dynamics Corporation

- Hornet

- Israel Aerospace Industries(IAI)

- Kongsberg Gruppen

- Leonardo SpA

- Northrop Grumman Corporation

- Rafael Advanced Defense Systems

- Raytheon Technologies Corporation

- Rheinmetall AG

- Saab AB

- Singapore Technologies Engineering Ltd.

- Thales Group

The Global Land-Based Remote Weapon Station Market is projected to reach USD 4.8 billion in 2024 and is expected to grow at a robust CAGR of 12.6% from 2025 to 2034. The market growth is largely driven by the rising demand for advanced defense systems and the ongoing modernization of military forces. As nations prioritize enhancing combat effectiveness and troop safety, the adoption of automated and remote-controlled weapon systems is reshaping modern warfare. These systems offer superior precision, reduce the risk to operators, and play a crucial role in evolving combat strategies.

The market is categorized by platform, with combat vehicles taking the lead, holding a dominant share of 64.9% in 2024. This segment continues to expand as the need for enhanced firepower, situational awareness, and protection against emerging threats intensifies. Remote-controlled weapon stations (RCWS) integrated into combat vehicles allow operators to engage targets with high accuracy while remaining securely inside the vehicle. These systems are key to providing both offensive and defensive capabilities, making them an indispensable part of modern armored platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 billion |

| Forecast Value | $15.5 billion |

| CAGR | 12.6% |

In terms of application, the land-based remote weapon station market is divided into military and homeland security sectors. The military segment is the fastest-growing, expected to increase at a CAGR of 13.4% through 2034. Demand for force protection, precision targeting, and overall operational efficiency is driving this growth. Remote weapon stations are critical components of armored vehicles, defense trucks, and fixed military installations. These systems not only enhance surveillance and targeting accuracy but also improve response times, all while minimizing the exposure of personnel to hostile environments. Their widespread deployment underscores their vital role in enhancing troop safety and combat performance.

In North America, the land-based remote weapon station market is forecasted to reach USD 7.5 billion by 2034. This growth is fueled by significant defense spending and ongoing investments in military modernization. The United States, in particular, is leading the charge by integrating advanced remote-controlled systems into its armored vehicles and defense infrastructure. The increasing use of artificial intelligence and automation in these systems is further driving innovation, boosting targeting capabilities, and improving operational efficiency. Continued investments in autonomous defense technologies are strengthening the region's defense posture and addressing evolving security challenges.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for precision targeting in modern warfare operations

- 3.6.1.2 Increasing military investments in advanced land-based defense systems

- 3.6.1.3 Growing adoption of remote-operated systems for soldier safety

- 3.6.1.4 Technological advancements enhancing weapon system interoperability and efficiency

- 3.6.1.5 Geopolitical tensions driving procurement of advanced military equipment

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development and integration costs for advanced weapon systems

- 3.6.2.2 Regulatory and export challenges impacting global market opportunities

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Combat Vehicles

- 5.2.1 Main battle tanks

- 5.2.2 Infantry fighting vehicles

- 5.2.3 Armored fighting vehicles

- 5.2.4 Unmanned ground vehicles

- 5.2.5 Others

- 5.3 Stationary Structures

Chapter 6 Market Estimates & Forecast, By Weapon Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Lethal Weapons

- 6.2.1 Small Caliber

- 6.2.1.1 5.56mm

- 6.2.1.2 7.62mm

- 6.2.1.3 12.7mm

- 6.2.2 Medium Caliber

- 6.2.3 20mm

- 6.2.4 25mm

- 6.2.5 30mm

- 6.2.6 40mm

- 6.2.1 Small Caliber

- 6.3 Non-lethal Weapons

Chapter 7 Market Estimates & Forecast, By Mobility, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Fixed

- 7.3 Moving

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Military

- 8.3 Homeland Security

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aselsan A.S.

- 10.2 BAE Systems

- 10.3 Bharat Electronics Limited (BEL)

- 10.4 Copenhagen Sensor Technology

- 10.5 Elbit Systems Ltd.

- 10.6 EVPU Defense

- 10.7 FN Herstal

- 10.8 General Dynamics Corporation

- 10.9 Hornet

- 10.10 Israel Aerospace Industries (IAI)

- 10.11 Kongsberg Gruppen

- 10.12 Leonardo S.p.A.

- 10.13 Northrop Grumman Corporation

- 10.14 Rafael Advanced Defense Systems

- 10.15 Raytheon Technologies Corporation

- 10.16 Rheinmetall AG

- 10.17 Saab AB

- 10.18 Singapore Technologies Engineering Ltd.

- 10.19 Thales Group