|

시장보고서

상품코드

1665402

자동차용 벨트 스타터 발전기 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Belt Starter Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

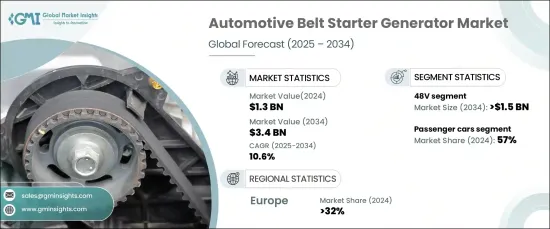

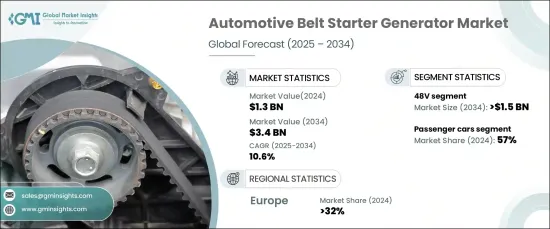

세계의 자동차용 벨트 스타터 발전기 시장은 2024년에는 13억 달러에 달하며, 2025-2034년에 CAGR 10.6%로 성장할 것으로 예측됩니다. 우수한 성능과 합리적인 가격으로 알려진 48V 시스템에 대한 수요가 증가하면서 특히 마일드 하이브리드 차량에서 BSG 시스템 채택이 증가하고 있습니다. 이 시스템은 더 높은 출력을 제공함으로써 기존 12V 시스템을 능가하여 마일드 하이브리드 파워트레인의 효율을 향상시킵니다. 또한 회생 제동 기능을 강화하여 제동시 많은 에너지를 회수 및 저장하여 연료 효율을 최적화합니다. 이러한 시스템은 엔진의 작업량을 줄이고 더 나은 에너지 관리를 가능하게 함으로써 운송의 지속가능성에 크게 기여합니다.

하이브리드 및 전기자동차로의 전환도 BSG 시장 성장에 중요한 역할을 하고 있습니다. 자동차 제조업체들은 더욱 강화된 배기가스 규제에 대응하고 친환경 모빌리티 솔루션에 대한 수요 증가에 대응하기 위해 이러한 시스템을 통합하고 있습니다. 스타터 모터와 발전기 기능을 결합한 BSG 시스템은 하이브리드 및 전기자동차의 파워트레인에 필수적인 구성 요소입니다. 에너지 사용을 개선하고, 회생 제동을 지원하며, 전반적인 차량 성능을 향상시키기 위해 친환경 자동차 기술로의 전환에 있으며, 중요한 혁신이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 13억 달러 |

| 예상 금액 | 34억 달러 |

| CAGR | 10.6% |

시장 규모는 제품별로 12V 시스템과 48V 시스템으로 구분되며, 2024년에는 48V 부문이 58% 이상 시장 점유율을 차지하고 2034년에는 15억 달러를 넘어설 것으로 예상됩니다. 이러한 시스템은 전동식 파워 스티어링, 에어컨, 회생 제동과 같은 중요한 차량 기능에 추가 전력을 공급할 수 있는 능력으로 인해 선호되고 있습니다. 이러한 시스템은 보다 부드러운 가속, 향상된 연비, 보다 효과적인 에너지 회수를 제공하여 엄격한 배기가스 규제에 대응하는 자동차 제조업체에게 이상적인 선택이 될 수 있습니다.

차종별로 시장은 승용차, 오프로드 차량, 상용차로 분류됩니다. 승용차는 2024년 시장 점유율의 약 57%를 차지합니다. 이들 차량은 48V BSG 시스템을 활용하여 연비 향상과 배출가스 감소를 달성하고, 전기자동차로 완전히 전환하지 않고도 비용 효율적인 솔루션을 원하는 소비자를 대상으로 합니다. 시동 및 정지 기능, 회생 제동, 내연기관 엔진의 추가 토크와 같은 기능은 이러한 시스템을 승용차 부문에 매우 매력적으로 만들어 시장 침투를 더욱 촉진하고 있습니다.

유럽은 2024년 세계 시장 점유율의 32% 이상을 차지하는 주요 지역으로 부상하며, 독일이 크게 기여하고 있습니다. 주요 기업이 하이브리드 및 전기자동차 기술에 많은 투자를 하고 있는 독일의 탄탄한 자동차 부문이 이러한 우위를 지원하고 있으며, CO2 배출을 억제하기 위한 엄격한 규제와 지속가능한 운송에 대한 관심은 자동차 제조업체들이 48V BSG 시스템을 광범위하게 채택하도록 유도하여 독일 시장 리더십을 강화하고 있습니다. 독일의 리더십을 강화하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 어프로치

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도 산출

- 시장 추정의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 정의

제2장 개요

제3장 산업 인사이트

- 에코시스템 분석

- 공급업체 상황

- 자동차 OEM

- 기술 프로바이더

- 애프터마켓과 서비스 프로바이더

- 최종사용자

- 이익률 분석

- 비용 내역 분석

- 기술과 혁신 전망

- 주요 뉴스와 구상

- 가격 분석

- 규제 상황

- 영향요인

- 촉진요인

- 배출 가스 규제의 강화

- 연료 효율에 대한 수요 증가

- 하이브리드차와 전기자동차의 채택 증가

- 촉진요인

48V 시스템의 성능과 비용 효율의 향상

- 벨트 스타터 발전기 설계의 기술적 진보

- 산업의 잠재적 리스크·과제

- 기술적·통합적 과제

- 풀하이브리드 및 전기 파워트레인과의 경쟁

- 성장 가능성 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정·예측 : 기술별, 2021-2034년

- 주요 동향

- 마일드 하이브리드

- 마이크로 하이브리드

제6장 시장 추정·예측 : 제품별, 2021-2034년

- 주요 동향

- 12V

- 48V

제7장 시장 추정·예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- LCV

- HCV

- OHV(Off highway vehicle)

제8장 시장 추정·예측 : 컴포넌트별, 2021-2034년

- 주요 동향

- 모터/발전기

- 파워 일렉트로닉스

- 기계식 커플링

- 제어 시스템

제9장 시장 추정·예측 : 냉각 유형별, 2021-2034년

- 주요 동향

- 공랭

- 액랭

- 하이브리드 냉각

제10장 시장 추정·예측 : 유통 채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제11장 시장 예측 : 지역별 시장 추정·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트

- 남아프리카공화국

- 사우디아라비아

제12장 기업 개요

- Bosch

- Continental

- Dayco

- Hyundai

- Infineon

- Magneti Marelli

- MTA

- Nexteer

- Onsemi

- Schaeffler Group

- SEG Automotive

- Sona Comstar

- Syensqo

- Valeo

- Vitesco Technologies

- ZF Friedrichshafen

The Global Automotive Belt Starter Generator Market was valued at USD 1.3 billion in 2024 and is anticipated to grow at a CAGR of 10.6% from 2025 to 2034. The increasing demand for 48V systems, known for their superior performance and affordability, is propelling the adoption of BSG systems, particularly in mild-hybrid vehicles. These systems outperform traditional 12V counterparts by delivering higher power output, which boosts the efficiency of mild-hybrid powertrains. They also enhance regenerative braking capabilities, capturing and storing more energy during braking to optimize fuel efficiency. By reducing the engine's workload and enabling better energy management, these systems contribute significantly to sustainability in transportation.

The shift towards hybrid and electric vehicles also plays a critical role in driving the BSG market. Automakers are integrating these systems to align with stricter emissions regulations and meet the growing demand for eco-friendly mobility solutions. BSG systems, which combine starter motor and generator functions, are vital components in hybrid and electric powertrains. They improve energy utilization, support regenerative braking, and enhance overall vehicle performance, making them a key innovation in the transition to greener automotive technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 10.6% |

The market is segmented by product into 12V and 48V systems. In 2024, the 48V segment accounted for over 58% of the market share and is projected to surpass USD 1.5 billion by 2034. These systems are preferred due to their ability to deliver additional electrical power for critical vehicle functions like electric power steering, air conditioning, and regenerative braking. They ensure smoother acceleration, improved fuel economy, and more effective energy recovery, positioning themselves as the ideal choice for automakers addressing stringent emissions standards.

In terms of vehicle type, the market is categorized into passenger cars, off-highway vehicles, and commercial vehicles. Passenger cars held approximately 57% of the market share in 2024. These vehicles leverage 48V BSG systems to achieve better fuel efficiency and reduced emissions, catering to consumers seeking cost-effective solutions without transitioning fully to electric vehicles. Features like start-stop functionality, regenerative braking, and additional torque for internal combustion engines make these systems highly attractive for the passenger car segment, further driving their market penetration.

Europe emerged as the leading region, capturing more than 32% of the global market share in 2024, with Germany being a significant contributor. The country's robust automotive sector, featuring key players heavily investing in hybrid and electric vehicle technologies, supports this dominance. Strict regulations to curb CO2 emissions and a focus on sustainable transportation have led to widespread adoption of 48V BSG systems among automakers, reinforcing Germany's leadership in the market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Automotive OEMs

- 3.2.2 Technology providers

- 3.2.3 Aftermarket and service providers

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Cost breakdown analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Pricing analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising implementation of stringent emission regulations

- 3.9.1.2 Growing demand for fuel efficiency

- 3.9.1.3 Increasing adoption of hybrid and electric vehicles

- 3.9.1 Growth drivers

3.9.1.4. Improved performance and cost-effectiveness of 48 V systems

- 3.9.1.5 Technological advancements in belt starter generator design

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Technological and integration challenges

- 3.9.2.2 Competition from full hybrid and electric powertrains

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Mild hybrid

- 5.3 Micro hybrid

Chapter 6 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 12V

- 6.3 48V

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 HCV

- 7.4 Off highway vehicle

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Motor/generator

- 8.3 Power electronics

- 8.4 Mechanical coupling

- 8.5 Control systems

Chapter 9 Market Estimates & Forecast, By Cooling Type, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Air-cooled

- 9.3 Liquid-cooled

- 9.4 Hybrid-cooled

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Bosch

- 12.2 Continental

- 12.3 Dayco

- 12.4 Hyundai

- 12.5 Infineon

- 12.6 Magneti Marelli

- 12.7 MTA

- 12.8 Nexteer

- 12.9 Onsemi

- 12.10 Schaeffler Group

- 12.11 SEG Automotive

- 12.12 Sona Comstar

- 12.13 Syensqo

- 12.14 Valeo

- 12.15 Vitesco Technologies

- 12.16 ZF Friedrichshafen