|

시장보고서

상품코드

1666966

반려동물용 암 치료제 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Pet Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

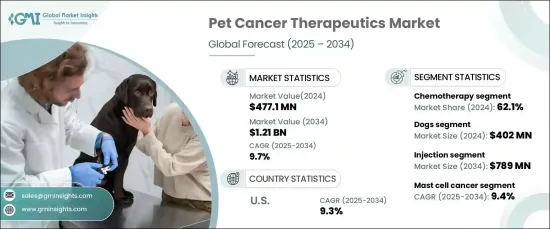

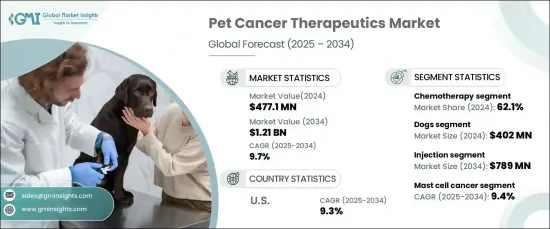

반려동물용 암 치료제 세계 시장은 2024년 4억 7,710만 달러로 평가되며 2025-2034년 동안 연평균 9.7%로 성장할 것으로 예상됩니다.

이러한 성장의 주요 요인은 반려동물 보호자들이 동물에 대한 높은 수준의 건강관리를 점점 더 우선시하게 되면서 반려동물의 인간화 추세가 증가하고 있기 때문입니다. 진단 능력의 향상과 표적 치료 및 면역요법을 포함한 최첨단 치료법은 수의사의 암 치료에 대한 접근성과 효과를 더욱 향상시키고 있습니다.

반려동물의 고령화로 인해 암 발병률이 증가하면서 종양학 솔루션에 대한 수요가 크게 증가하고 있습니다. 이러한 소비자 행동의 변화는 수의학의 끊임없는 발전과 함께 반려동물을 위한 혁신적인 생명 연장 치료에 대한 시장의 요구가 증가하고 있음을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 4억 7,710만 달러 |

| 예상 금액 | 12억 1,000만 달러 |

| CAGR | 9.7% |

시장은 동물 종별로 개, 고양이, 기타 동물로 구분됩니다. 개가 가장 큰 시장 점유율을 차지하며 2024년 시장 규모는 4억 200만 달러에 달했습니다. 이러한 우위는 다른 반려동물에 비해 개가 림프종, 골육종, 유선종양과 같은 암 발생률이 높기 때문입니다. 반려견 종양학에 대한 전문적인 치료의 필요성이 증가함에 따라 효과적인 치료 옵션에 대한 수요가 계속 증가하고 있습니다.

치료법별로는 화학요법, 면역요법, 표적 치료제, 병용요법 등이 있습니다. 화학요법은 2024년 62.1%의 점유율을 차지하며 주요 부문으로 부상했습니다. 암세포를 표적으로 삼고 그 증식을 억제하는 효과로 잘 알려진 화학요법은 다양한 암, 특히 림프종과 비만세포종 치료의 핵심으로 자리 잡고 있습니다. 특히 일반적인 반려견의 암에 대한 높은 관해 성공률은 수의사의 암 치료에서 화학요법의 지속적인 우위를 보장하고 있습니다.

미국의 반려동물용 암 치료제 시장은 2025-2034년 동안 연평균 9.3%의 성장률을 기록할 것으로 예상됩니다. 이러한 리더십은 미국의 탄탄한 수의학 의료 인프라, 높은 반려동물 사육률, 첨단 암 치료에 대한 광범위한 인식에 기인합니다. 수의 종양학 연구와 기술에 대한 막대한 투자는 면역요법 및 표적 치료제를 포함한 혁신적인 치료법 개발을 가능하게 하여 미국 시장을 더욱 강화시키고 있습니다.

또한, 고령화된 반려동물의 암 유병률이 증가함에 따라 고품질 치료 솔루션에 대한 수요가 지속적으로 증가하고 있습니다. 첨단 수의학적 치료에 대한 인식과 채택이 증가함에 따라 반려동물용 암 치료제 시장은 전 세계적으로 강력한 성장이 예상되며, 북미는 업계 동향을 형성하는 데 있어 매우 중요한 역할을 하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 반려동물 인간화 증가

- 반려동물 암 이환율 상승

- 수의 종양학의 진단과 치료 진보

- 인식과 진단 능력 향상

- 업계의 잠재적 리스크와 과제

- 고액의 치료비

- 부작용과 동물에 대한 내성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 파이프라인 분석

- 향후 시장 동향

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정과 예측 : 동물 종류별, 2021-2034년

- 주요 동향

- 개

- 고양이

- 기타

제6장 시장 추정과 예측 : 치료법별, 2021-2034년

- 주요 동향

- 화학요법

- 면역요법

- 표적요법

- 병용요법

제7장 시장 추정과 예측 : 투여 경로별, 2021-2034년

- 주요 동향

- 경구

- 주사

제8장 시장 추정과 예측 : 암종별, 2021-2034년

- 주요 동향

- 림프종

- 비만세포종

- 흑색종

- 유선암, 편평상피암

- 기타

제9장 시장 추정과 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제10장 기업 개요

- AB Science

- Boehringer Ingelheim International

- CureLab Oncology

- Dechra Pharmaceuticals

- Elanco Animal Health

- ELIAS Animal Health

- NovaVive

- Qbiotics

- Pfizer

- Torigen

- Vibrac

- Vivesto

- Zoetis

The Global Pet Cancer Therapeutics Market reached USD 477.1 million in 2024 and is anticipated to grow at a CAGR of 9.7% from 2025 to 2034. This growth is primarily attributed to the rising trend of pet humanization, as pet owners increasingly prioritize advanced healthcare for their animals. Enhanced diagnostic capabilities and cutting-edge treatments, including targeted therapies and immunotherapies, are further boosting the accessibility and effectiveness of veterinary cancer care.

The aging pet population has led to a higher prevalence of cancer, significantly driving the demand for oncology solutions. This evolution in consumer behavior, combined with continual advancements in veterinary medicine, underlines the growing market need for innovative and life-prolonging treatments for pets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $477.1 Million |

| Forecast Value | $1.21 Billion |

| CAGR | 9.7% |

The market is segmented by species into dogs, cats, and other animals. Dogs held the largest market share, valued at USD 402 million in 2024. This dominance is attributed to the higher incidence of cancers such as lymphoma, osteosarcoma, and mammary tumors in dogs compared to other pets. The growing need for specialized treatments in canine oncology continues to propel the demand for effective therapeutic options.

By therapy, the market includes chemotherapy, immunotherapy, targeted therapy, and combination therapy. Chemotherapy emerged as the leading segment, generating a 62.1% share in 2024. Known for its efficacy in targeting and inhibiting the growth of cancer cells, chemotherapy remains a cornerstone of treatment for various cancers, particularly lymphoma and mast cell tumors. Its high success rates in remission, especially for common canine cancers, ensure its continued prominence in veterinary oncology.

U.S. pet cancer therapeutics market held a CAGR of 9.3% throughout 2025-2034. This leadership is driven by the country's robust veterinary healthcare infrastructure, high pet ownership rates, and widespread awareness of advanced cancer treatments. Significant investments in veterinary oncology research and technology enable the development of innovative therapies, including immunotherapy and targeted treatments, further strengthening the U.S. market.

Additionally, the increasing prevalence of cancer among aging pets continues to fuel the demand for high-quality therapeutic solutions. As awareness and adoption of advanced veterinary care rise, the pet cancer therapeutics market is expected to witness robust growth globally, with North America maintaining a pivotal role in shaping industry trends.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet humanization

- 3.2.1.2 Rising cancer incidence in pets

- 3.2.1.3 Advancements in veterinary oncology diagnosis and treatment

- 3.2.1.4 Growing awareness and diagnostic capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Side effects and animal tolerance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Species, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dogs

- 5.3 Cats

- 5.4 Other species

Chapter 6 Market Estimates and Forecast, By Therapy, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapy

- 6.3 Immunotherapy

- 6.4 Targeted therapy

- 6.5 Combination therapy

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injection

Chapter 8 Market Estimates and Forecast, By Cancer Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Lymphoma

- 8.3 Mast cell cancer

- 8.4 Melanoma

- 8.5 Mammary and squamous cell cancer

- 8.6 Other cancer types

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AB Science

- 10.2 Boehringer Ingelheim International

- 10.3 CureLab Oncology

- 10.4 Dechra Pharmaceuticals

- 10.5 Elanco Animal Health

- 10.6 ELIAS Animal Health

- 10.7 NovaVive

- 10.8 Qbiotics

- 10.9 Pfizer

- 10.10 Torigen

- 10.11 Vibrac

- 10.12 Vivesto

- 10.13 Zoetis