|

시장보고서

상품코드

1666978

차량 네트워킹 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Vehicle Networking Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

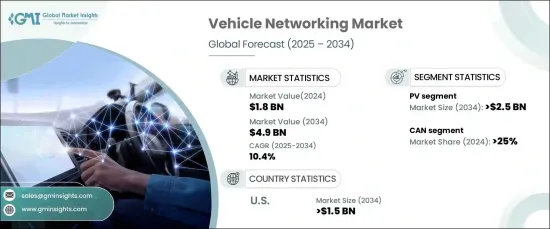

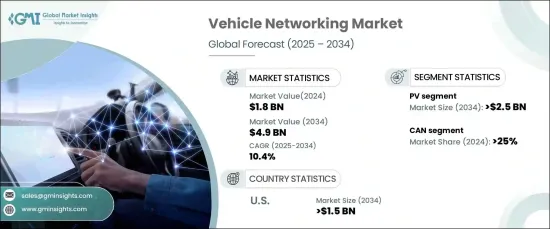

세계 차량 네트워킹 시장은 2024년 18억 달러로 평가되며 2025년부터 2034년까지 연평균 10.4%의 견고한 성장세를 보일 것으로 예상됩니다. 이러한 성장의 주요 원인은 사물인터넷(IoT)과 5G 네트워크의 통합으로 가속화되는 커넥티드카 기술의 채택에 기인합니다. 이러한 첨단 기술은 차량과 인프라 간의 원활한 실시간 통신을 가능하게 하여 안전, 효율성 및 전반적인 운전 경험을 향상시키고 있습니다. 자율주행 차량이 확대됨에 따라 첨단 네트워킹 솔루션에 대한 수요는 더욱 증가하고 있습니다. 효율적인 차량 대 차량(V2V) 및 차량 대 차량(V2I) 통신은 자율주행차가 원활하게 작동하기 위해 필수적이며, 자동차 산업의 미래에 중요한 요소로 자리 잡고 있습니다.

또한, 차량 진단 및 예지보전에 대한 중요성이 강조되고 있는 것도 시장의 주요 촉진요인으로 작용하고 있습니다. 첨단 네트워킹 기술의 도입으로 차량 성능의 지속적인 모니터링이 가능해져 잠재적인 문제를 조기에 발견할 수 있게 되었습니다. 이러한 조기 발견은 신뢰성을 향상시킬 뿐만 아니라, 유지보수 비용과 차량 가동 중단 시간을 줄여 개인 소비자와 차량 운영자 모두에게 혜택을 제공합니다. 또한, 실시간 충돌 방지 및 긴급 제동과 같은 안전 기능의 발전은 신뢰할 수 있는 고성능 차량 네트워킹 시스템의 필요성을 더욱 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 18억 달러 |

| 예상 금액 | 49억 달러 |

| CAGR | 10.4% |

차량 유형별로는 승용차(PV), 소형 상용차(LCV), 대형 상용차(HCV), 자율주행차(AGV)로 구분되며, PV 부문은 2024년 50%의 압도적인 점유율을 차지하며 2034년 25억 달러에 달할 것으로 예상됩니다. 이러한 우위는 인포테인먼트 시스템, 실시간 내비게이션, 강화된 안전 기능 등 승용차에 탑재되는 첨단 차량용 기술에 대한 소비자 수요 증가에 기인한 것으로 분석됩니다.

연결성 측면에서 차량 네트워킹 시장은 LIN, CAN, RF, 이더넷, FlexRay, MOST로 분류되며, CAN(Controller Area Network) 부문은 신뢰성, 견고성, 비용 효율성으로 인해 2024년 25%의 점유율을 차지하고 있습니다. CAN은 엔진 제어, 브레이크 등 중요한 자동차 시스템의 실시간 데이터 전송에 널리 사용되고 있으며, 전자기 간섭이 많은 열악한 환경에서도 우수한 성능을 발휘합니다.

2024년 차량용 네트워킹 시장은 미국이 세계 시장 점유율의 90%를 차지하며 선두를 달리고 있습니다. 미국의 자동차 시장은 2034년까지 15억 달러에 달할 것으로 예상되며, 이는 미국의 탄탄한 자동차 부문과 자율주행, 전기자동차, 5G 커넥티비티와 같은 혁신적인 기술의 급속한 도입에 힘입은 것입니다. 이러한 기술 혁신은 첨단 차량 네트워킹 솔루션에 크게 의존하고 있으며, 이는 미국 시장을 크게 성장시키는 원동력이 되고 있습니다. 소비자의 기대치가 높아지고 기술이 계속 발전함에 따라 차량 네트워킹 시장은 차량의 연결성과 성능을 향상시키는 혁신적인 솔루션을 제공하면서 괄목할 만한 성장을 거듭하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 설계

- 조사 접근법

- 데이터 수집 방법

- 기본 추정과 계산

- 기준 연도 산출

- 시장 추정의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 정의

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 테크놀러지 프로바이더

- 서비스 프로바이더

- 유통업체

- 최종 용도

- 이익률 분석

- 가격 분석

- 비용 내역

- 기술과 혁신 전망

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 정부에 의한 이산화탄소 배출량 절감에 대한 주력

- 전기자동차 판매 확대

- 자동차 부품 산업에 대한 정부 지원

- 시장 기업에 의한 전략적 이니셔티브

- 업계의 잠재적 리스크와 과제

- 전기자동차의 반도체 소비 증가

- 개발도상국이나 후발 개발도상국의 자율 이동 인프라의 부족

- 성장 촉진요인

- 성장 가능성 분석

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정과 예측 : 차량별, 2021-2034년

- 주요 동향

- PV

- LCV

- HCV

- AGV

제6장 시장 추정과 예측 : 연결성별, 2021-2034년

- 주요 동향

- CAN(컨트롤러 에어리어 네트워크)

- LIN(로컬 상호연결 네트워크)

- RF(무선주파수)

- FlexRay

- 이더넷

- MOST(미디어 지향 시스템 트랜스포트)

제7장 시장 추정과 예측 : 용도별, 2021-2034년

- 주요 동향

- 파워트레인

- 세이프티

- 바디 일렉트로닉스

- 섀시

- 인포테인먼트

제8장 시장 추정과 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카공화국

- 사우디아라비아

제9장 기업 개요

- Acome

- Analog Devices

- Bosch

- Broadcom

- Continental

- Intel

- Harman

- Marvell Semiconductor

- Microchip Technology

- NXP Semiconductors

- ON Semiconductor

- Qualcomm

- Renesas

- Sierra Wireless

- Spiarent

- Communications

- STMicroelectronics NV

- Texas Instrumental

- Toshiba

- Xilinx

The Global Vehicle Networking Market, with a valuation of USD 1.8 billion in 2024, is expected to grow at a robust CAGR of 10.4% from 2025 to 2034. This growth is primarily driven by the accelerating adoption of connected car technologies, fueled by the integration of the Internet of Things (IoT) and 5G networks. These cutting-edge technologies enable seamless real-time communication between vehicles and infrastructure, enhancing safety, efficiency, and the overall driving experience. The expansion of autonomous vehicles has further spurred demand for advanced networking solutions. Efficient vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication are vital for the smooth functioning of self-driving cars, making them a critical component in the future of the automotive industry.

Furthermore, the increasing emphasis on vehicle diagnostics and predictive maintenance is becoming a major market driver. With advanced networking technologies in place, continuous monitoring of vehicle performance is now possible, allowing for early detection of potential issues. This early detection not only ensures better reliability but also helps to reduce maintenance costs and vehicle downtime, benefiting both individual consumers and fleet operators. In addition, advancements in safety features, such as real-time collision avoidance and emergency braking, are pushing the need for reliable, high-performance vehicle networking systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 10.4% |

In terms of vehicle types, the market is segmented into Passenger Vehicles (PV), Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), and Autonomous Guided Vehicles (AGV). The PV segment held a dominant 50% share in 2024 and is forecast to reach USD 2.5 billion by 2034. This dominance is largely due to the growing consumer demand for advanced in-car technologies, including infotainment systems, real-time navigation, and enhanced safety features that are increasingly being incorporated into passenger vehicles.

On the connectivity front, the vehicle networking market is categorized into LIN, CAN, RF, Ethernet, FlexRay, and MOST. The CAN (Controller Area Network) segment held a 25% share in 2024 thanks to its reliability, robustness, and cost-effectiveness. It's widely used for real-time data transmission in critical automotive systems like engine control and braking, providing exceptional performance even in harsh environments with high electromagnetic interference.

The U.S. vehicle networking market was the leader in 2024, accounting for 90% of the global share. The market in the U.S. is expected to reach USD 1.5 billion by 2034, driven by the country's well-established automotive sector and rapid adoption of groundbreaking technologies such as autonomous driving, electric vehicles, and 5G connectivity. These innovations rely heavily on advanced vehicle networking solutions, propelling the U.S. market toward substantial growth. As consumer expectations rise and technology continues to evolve, the vehicle networking market is poised for remarkable expansion, delivering innovative solutions that enhance vehicle connectivity and performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 Service providers

- 3.2.3 Distributors

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Pricing analysis of

- 3.5 Cost breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Government focus on reducing carbon emissions

- 3.9.1.2 Growing sales of electric vehicles

- 3.9.1.3 Government support for automotive components industry

- 3.9.1.4 Strategic initiatives by market players

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Increasing consumption of semiconductors in electric vehicles

- 3.9.2.2 Lack of autonomous mobility infrastructure in developing and underdeveloped countries

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 PV

- 5.3 LCV

- 5.4 HCV

- 5.5 AGV

Chapter 6 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 CAN (Controller Area Network)

- 6.3 LIN (Local Interconnect Network)

- 6.4 RF (Radio Frequency)

- 6.5 FlexRay

- 6.6 Ethernet

- 6.7 MOST (Media Oriented Systems Transport)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Powertrain

- 7.3 Safety

- 7.4 Body electronics

- 7.5 Chassis

- 7.6 Infotainment

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Acome

- 9.2 Analog Devices

- 9.3 Bosch

- 9.4 Broadcom

- 9.5 Continental

- 9.6 Intel

- 9.7 Harman

- 9.8 Marvell Semiconductor

- 9.9 Microchip Technology

- 9.10 NXP Semiconductors

- 9.11 ON Semiconductor

- 9.12 Qualcomm

- 9.13 Renesas

- 9.14 Sierra Wireless

- 9.15 Spiarent

- 9.16 Communications

- 9.17 STMicroelectronics NV

- 9.18 Texas Instrumental

- 9.19 Toshiba

- 9.20 Xilinx