|

시장보고서

상품코드

1684648

레이더 시뮬레이터 시장 : 기회 및 성장 촉진요인, 산업 동향 분석(2025-2034년)Radar Simulators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

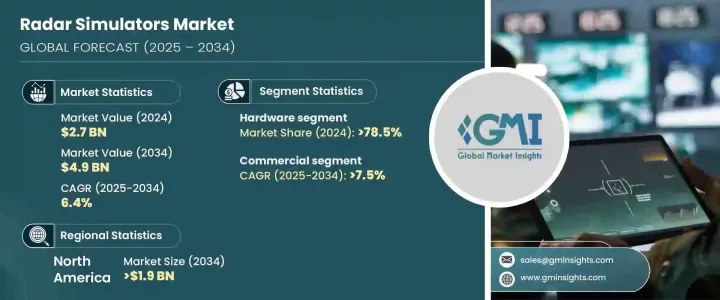

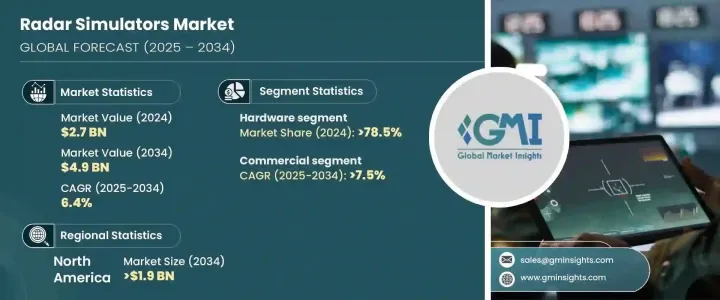

세계의 레이더 시뮬레이터 시장은 2024년에 27억 달러로 평가되었고, 2025년부터 2034년까지 연평균 성장률(CAGR) 6.4%로 성장할 것으로 예측됩니다.

이러한 성장은 주로 첨단 방위 시스템과 최첨단 미사일 기술에 대한 수요 증가에 의해 주도되고 있습니다. 이와 함께 인공 지능(AI)과 엣지 컴퓨팅이 레이더 시스템에 통합되면서 이러한 시뮬레이션이 더욱 스마트하고 효율적으로 구현되어 전반적인 시스템 성능이 향상되고 있습니다.

레이더 시뮬레이터 시장은 하드웨어와 소프트웨어 구성 요소로 분류되며, 2024년에는 하드웨어 부문이 78.5%의 압도적 점유율을 차지했습니다. 이러한 혁신 덕분에 고성능 기능을 제공하면서도 더 작고 휴대성이 뛰어난 레이더 시뮬레이터를 생산할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 27억 달러 |

| 예측 금액 | 49억 달러 |

| CAGR | 6.4% |

용도의 관점에서 시장은 상업용과 군사 및 방위 부문으로 나뉩니다. 상업 부문은 2034년까지 7.5%의 놀라운 연평균 성장률을 보일 것으로 예상됩니다. 이러한 성장의 주요 동인은 자동차 산업에서 특히 첨단 운전자 지원 시스템(ADAS) 테스트를 위한 레이더 시뮬레이터의 채택이 증가하고 있다는 점입니다. 차량의 자율 주행이 확대됨에 따라 적응형 크루즈 컨트롤, 자동 긴급 제동, 차선 유지 지원과 같은 ADAS 기능은 테스트 및 검증을 위해 레이더 시뮬레이터 기술에 크게 의존하고 있습니다.

북미, 특히 미국은 레이더 시뮬레이터 시장을 독점할 전망이며, 2034년까지 19억 달러 시장 가치가 예측되고 있습니다. 이 지역의 국방, 자동차, 통신 부문에서 레이더 시뮬레이션 기술을 빠르게 도입한 것이 이러한 성장의 주요 요인입니다. 또한 AI와 머신 러닝의 혁신은 특히 자율 주행 차량 테스트 및 차세대 방위 시스템과 같은 분야에서 레이더 시뮬레이터의 기능을 향상시키고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 자료

- 유료

- 공적

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혼란

- 장래의 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 자율 주행 기술에 대한 수요 증가

- 국방 및 군사 현대화

- AI와 머신러닝의 통합

- 5G 네트워크의 출시와 레이더 기반 통신 기술의 발전

- 첨단 운전자 지원 시스템(ADAS) 수요 증가

- 업계의 잠재적 위험 및 과제

- 높은 개발 비용

- 시뮬레이션 정확도의 복잡성

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 시스템 테스트

- 고정형

- 휴대용

- 운영자 교육

- 고정형

- 휴대용

제6장 시장 추계 및 예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 하드웨어

- 소프트웨어

제7장 용도별 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 상업용

- 군사 및 방위

- 항공기

- 해상

- 지상

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Acewavetech

- Adacel Technologies

- ARI Simulation

- Buffalo Computer Graphics

- Cambridge Pixel

- L3Harris Technologies

- Mercury Systems

- Mistral Solutions

- RTX

- Textron Systems

- Ultra Intelligence &Communications

The Global Radar Simulators Market was valued at USD 2.7 billion in 2024 and is forecasted to expand at a CAGR of 6.4% from 2025 to 2034. This growth is primarily driven by the escalating demand for advanced defense systems and cutting-edge missile technology. As governments and defense organizations around the world seek to enhance the accuracy, efficiency, and operational capabilities of their radar systems, the adoption of radar simulators has become crucial. These simulators allow for real-time virtual testing, helping to simulate various operational scenarios without the risks associated with live trials. Alongside this, the integration of artificial intelligence (AI) and edge computing into radar systems is making these simulations smarter and more efficient, improving overall system performance. The combination of technological advancements in these areas ensures that radar simulators are essential for modernizing both defense strategies and personnel training programs.

The radar simulators market is segmented into hardware and software components, with the hardware segment holding a dominant share of 78.5% in 2024. This segment is projected to continue growing at a rapid pace, driven by ongoing advancements in semiconductor technology. These innovations enable the production of smaller, more portable radar simulators that still deliver high-performance capabilities. This trend is especially critical in sectors like defense and automotive, where compact, mobile systems are necessary for operational flexibility and effectiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.7 Billion |

| Forecast Value | $4.9 Billion |

| CAGR | 6.4% |

In terms of application, the market is divided into commercial and military & defense segments. The commercial segment is set to grow at an impressive CAGR of 7.5% through 2034. A major driver of this growth is the increasing adoption of radar simulators in the automotive industry, particularly for testing advanced driver-assistance systems (ADAS). As vehicles become more autonomous, ADAS features such as adaptive cruise control, automatic emergency braking, and lane-keeping assistance rely heavily on radar simulator technologies for their testing and validation. This growing demand in automotive applications is a significant factor pushing the commercial segment's expansion.

North America, particularly the United States, is poised to dominate the radar simulators market, with a projected market value of USD 1.9 billion by 2034. The region's rapid adoption of radar simulation technologies in defense, automotive, and telecommunications sectors is a key factor in this growth. Additionally, innovations in AI and machine learning are enhancing radar simulators' capabilities, especially in areas like autonomous vehicle testing and next-generation defense systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for autonomous driving technologies

- 3.6.1.2 Defense and military modernization

- 3.6.1.3 Integration of AI and machine learning

- 3.6.1.4 Rollout of 5G networks and advancements in radar-based communication technologies

- 3.6.1.5 Rising demand for Advanced Driver Assistance Systems (ADAS)

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development costs

- 3.6.2.2 Complexity in simulation accuracy

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 System testing

- 5.2.1 Fixed

- 5.2.2 Portable

- 5.3 Operator training

- 5.3.1 Fixed

- 5.3.2 Portable

Chapter 6 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Software

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Commercial

- 7.3 Military & defense

- 7.3.1 Airborne

- 7.3.2 Marine

- 7.3.3 Ground

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Acewavetech

- 9.2 Adacel Technologies

- 9.3 ARI Simulation

- 9.4 Buffalo Computer Graphics

- 9.5 Cambridge Pixel

- 9.6 L3Harris Technologies

- 9.7 Mercury Systems

- 9.8 Mistral Solutions

- 9.9 RTX

- 9.10 Textron Systems

- 9.11 Ultra Intelligence & Communications