|

시장보고서

상품코드

1685053

정밀농업 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Precision Farming Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

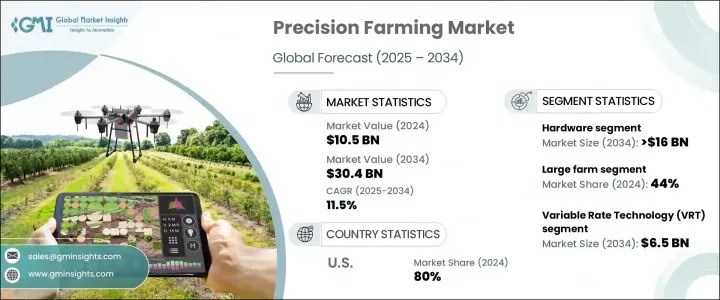

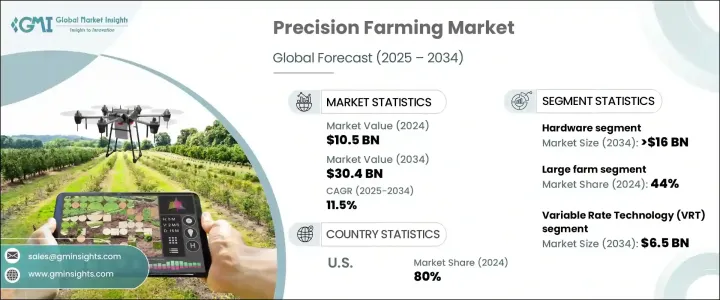

세계의 정밀농업 시장은 2024년에 105억 달러로 평가되었고, 2025년부터 2034년까지 11.5%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측되고 있습니다.

급속한 인구 증가 및 식량 수요 증가가 이 시장 확대의 주요 원동력이 되고 있습니다. 세계 인구가 매년 약 8,300만 명씩 증가하고 있는 가운데, 지속가능한 농업의 실천이 보다 급무가 되고 있습니다. 작물의 수율을 최적화하기 위해 첨단 기술을 활용하는 정밀농업은 이 문제에 대한 중요한 해결책으로 부상했습니다.

정밀농업의 도입을 촉진하는 데 있어서 세계 각국의 정부는 중요한 역할을 하고 있습니다. 보조금 및 조성금, 시책적 인센티브를 제공함으로써 환경에 미치는 영향을 최소화하면서 농업 생산성을 높이는 것을 목표로 하고 있습니다. 정밀농업은 IoT, AI, 드론, 데이터 분석 등의 기술을 통합하여 효율성을 높이고 자원 소비를 줄입니다. 이러한 기술 혁신은 농업 종사자의 생산성 향상, 운영 비용 절감, 친환경 실천을 지원하고 장기적으로 지속 가능한 식량 생산을 보장합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 105억 달러 |

| 예측 금액 | 304억 달러 |

| CAGR | 11.5% |

시장은 컴포넌트별로 구분되며, 2024년에는 하드웨어가 55% 이상 시장 점유율을 차지해 1위에 올랐습니다. 2034년까지 이 부문은 160억 달러 이상에 달할 것으로 예측됩니다. 농업에 있어서 GPS, 센서, 자동화 기기의 채용이 증가하고 있는 것이, 이 성장을 뒷받침하고 있습니다. 토양 센서, 웨더 스테이션, GPS 수신기 등의 하드웨어 도구를 통해 농업 종사자는 상태를 모니터링하고 관개를 최적화하고 심기 및 수확과 같은 중요한 작업을 자동화할 수 있습니다. 자동화는 더욱 효율을 높이고, 종래는 수작업으로 하고 있던 작업을 로봇 시스템이 실시했습니다.

농장 규모별로는 대규모 농장이 2024년 시장 점유율의 약 44%를 차지했습니다. 생산성 및 효율성을 향상시키기 위해 첨단 기술에 투자할 수 있는 것이 이 우위성의 원인이 되고 있습니다. GPS 유도 트랙터, 무인 항공기, 스마트 관개 시스템은 작물의 정확한 모니터링과 자원 관리를 가능하게 합니다. 대규모 농장이 운영 최적화를 목표로 하는 동안 정밀농업 솔루션에 대한 수요는 계속 증가하고 있습니다.

기술적 측면에서 가변 속도 기술(VRT)은 지배적인 부문이며 2034년까지 65억 달러를 창출할 것으로 예상됩니다. 이 기술을 통해 농업 종사자는 특정 농장 조건에 따라 비료, 씨앗 및 농약의 살포를 조정할 수 있습니다. 센서, GPS 및 고급 소프트웨어의 데이터를 활용하여 VRT는 최적의 투입 배분을 보장하고 수확량을 극대화하면서 낭비를 없애줍니다. 비용 효율성과 지속 가능한 농업이 중요해지면서 도입이 가속화되고 농업 기관의 지원도 증가하고 있기 때문에 이러한 시스템은 보다 친숙해지고 있습니다.

용도별로는 수율 모니터링이 2024년 점유율 25%로 시장을 선도했습니다. 이 시스템은 농업 종사자가 실시간으로 작물 생산을 추적하고 생산성을 높이기 위해 데이터 중심의 의사 결정을 가능하게 합니다. 센서 기술과 데이터 분석의 진보는 수율 패턴과 토양 상태에 대한 정확한 인사이트를 제공하고 장기적인 농장 관리를 개선합니다. 식량 수요가 증가함에 따라 정밀농업 솔루션은 농업 생산 최적화에 필수적입니다.

북미는 세계 시장을 선도하고 있으며, 2024년에는 미국이 80%의 점유율을 차지했습니다. 선진 농업 기술의 보급, 정부 보조금, 강력한 인프라가 정밀농업의 확대를 지원하고 있습니다. 무인 항공기, 센서 및 데이터 분석에 대한 의존도가 높아짐에 따라 농업 경영이 지속적으로 변화하여 농업이 더욱 효율적이고 수익성이 높아지고 있습니다.

목차

제1장 조사 방법 및 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정 및 계산

- 기준 연도의 산출

- 시장 추정의 주요 동향

- 예측 모델

- 1차 조사 및 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 범위 및 정의

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 하드웨어 제공업체

- 소프트웨어 제공업체

- 서비스 제공업체

- 기술 제공업체

- 최종 사용자

- 공급자의 상황

- 이익률 분석

- 기술 혁신의 상황

- 특허 분석

- 주요 뉴스 및 이니셔티브

- 규제 상황

- 정밀농업의 진화

- 이용 사례

- 영향요인

- 성장 촉진요인

- 지속 가능한 농업에 대한 요구 증가

- 세계 인구 증가 및 그에 따른 식량 증산에 대한 수요 증가

- 농업 기술에 대한 투자 증가

- 디지털농업 기술을 지원하는 정부의 대처 및 보조금

- 산업의 잠재적 리스크 및 과제

- 첨단 정밀농업 기계를 조작하는 숙련 노동자의 부족

- 시골 지역의 고속 인터넷 접속 제한

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 하드웨어

- 센서

- 자동 조타 시스템

- 드론, UAV 및 카메라

- 모바일 기기

- GPS 및 GNSS

- 기타

- 소프트웨어

- 농장 관리 소프트웨어(FMS)

- 데이터 분석 및 빅 데이터 솔루션

- 지리 정보 시스템(GIS) 소프트웨어

- 클라우드 기반 소프트웨어 솔루션

- 인공지능 및 머신러닝 소프트웨어

- 서비스

- 전문 서비스

- 매니지드 서비스

제6장 시장 추정 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 고정밀 측위 시스템

- 지오 매핑

- 리모트 센싱

- 통합 전자통신

- 가변 속도 기술(VRT)

제7장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 날씨 모니터링

- 수율 모니터링

- 현장 매핑

- 관개 관리

- 폐기물 관리

- 재무관리

- 기타

제8장 시장 추정 및 예측 : 농장 규모별(2021-2034년)

- 주요 동향

- 소규모 농장

- 중규모 농장

- 대규모 농장

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- AG Leader

- AGCO

- Agribotix

- AgSense

- AgSmarts

- Boumatic

- CNH

- CropMetrics

- CropX

- Delaval

- Dickey-John

- Farmers Edge

- GEA Group

- John Deere

- Monsanto

- Precision Planting

- Raven

- Topcon

- Trimble

- Yara

The Global Precision Farming Market was valued at USD 10.5 billion in 2024 and is projected to grow at an 11.5% CAGR from 2025 to 2034. Rapid population growth and the increasing demand for food are key drivers behind this expansion. With the global population rising by approximately 83 million annually, the need for sustainable agricultural practices has become more urgent. Precision farming, which leverages advanced technologies to optimize crop yields, has emerged as a critical solution to this challenge.

Governments worldwide are playing a crucial role in promoting the adoption of precision agriculture. By offering subsidies, grants, and policy incentives, they aim to boost agricultural productivity while minimizing environmental impact. Precision farming integrates technologies such as IoT, AI, drones, and data analytics to improve efficiency and reduce resource consumption. These innovations help farmers enhance productivity, cut operational costs, and implement eco-friendly practices, ensuring sustainable food production in the long run.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.5 billion |

| Forecast Value | $30.4 billion |

| CAGR | 11.5% |

The market is segmented based on components, with hardware leading in 2024, holding over 55% market share. By 2034, the segment is anticipated to surpass USD 16 billion. The increasing adoption of GPS, sensors, and automated equipment in farming operations is driving this growth. Hardware tools such as soil sensors, weather stations, and GPS receivers enable farmers to monitor conditions, optimize irrigation, and automate critical tasks like planting and harvesting. Automation further enhances efficiency, with robotic systems performing tasks traditionally handled manually.

By farm size, large farms accounted for approximately 44% of the market share in 2024. Their ability to invest in advanced technology for improved productivity and efficiency contributes to this dominance. GPS-guided tractors, drones, and smart irrigation systems allow for precise crop monitoring and resource management. As large-scale farms seek to optimize operations, demand for precision farming solutions continues to rise.

Technology-wise, variable rate technology (VRT) is a dominant segment, expected to generate USD 6.5 billion by 2034. This technology allows farmers to tailor the application of fertilizers, seeds, and pesticides based on specific field conditions. By leveraging data from sensors, GPS, and advanced software, VRT ensures optimal input distribution, reducing waste while maximizing yield. The growing emphasis on cost efficiency and sustainable farming is accelerating adoption, with increased support from agricultural institutions making these systems more accessible.

In terms of applications, yield monitoring led the market in 2024 with a 25% share. This system helps farmers track crop performance in real time, enabling data-driven decisions to enhance productivity. Advancements in sensor technology and data analytics provide precise insights into yield patterns and soil conditions, improving long-term farm management. With increasing food demand, precision farming solutions are becoming essential for optimizing agricultural output.

North America leads the global market, with the US holding an 80% share in 2024. The widespread adoption of advanced agricultural technologies, government subsidies, and strong infrastructure support precision farming expansion. Increased reliance on drones, sensors, and data analytics continues to transform farming operations, making agriculture more efficient and profitable.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Hardware providers

- 3.1.2 Software providers

- 3.1.3 Service providers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Evolution of precision farming

- 3.9 Use cases

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 The growing need for sustainable farming practices

- 3.10.1.2 The rising global population and the corresponding demand for higher food production

- 3.10.1.3 Increased investment in agricultural technologies

- 3.10.1.4 Government initiatives and subsidies supporting digital farming technologies

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 The lack of skilled labor to operate advanced precision farming equipment

- 3.10.2.2 Limited access to high-speed internet in rural areas

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensor

- 5.2.2 Automated steering system

- 5.2.3 Drone, UAV, and camera

- 5.2.4 Mobile device

- 5.2.5 GPS and GNSS

- 5.2.6 Others

- 5.3 Software

- 5.3.1 Farm Management Software (FMS)

- 5.3.2 Data analytics and big data solution

- 5.3.3 Geographic information system (GIS) software

- 5.3.4 Cloud-based software solution

- 5.3.5 Artificial intelligence and machine learning software

- 5.4 Services

- 5.4.1 Professional services

- 5.4.2 Managed services

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 High precision positioning system

- 6.3 Geo mapping

- 6.4 Remote sensing

- 6.5 Integrated electronic communication

- 6.6 Variable Rate Technology (VRT)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Weather monitoring

- 7.3 Yield monitoring

- 7.4 Field mapping

- 7.5 Irrigation management

- 7.6 Waste management

- 7.7 Financial management

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Farm Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Small farm

- 8.3 Medium farm

- 8.4 Large farm

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.2.7 Nordics

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 UAE

- 9.5.2 South Africa

- 9.5.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 AG Leader

- 10.2 AGCO

- 10.3 Agribotix

- 10.4 AgSense

- 10.5 AgSmarts

- 10.6 Boumatic

- 10.7 CNH

- 10.8 CropMetrics

- 10.9 CropX

- 10.10 Delaval

- 10.11 Dickey-John

- 10.12 Farmers Edge

- 10.13 GEA Group

- 10.14 John Deere

- 10.15 Monsanto

- 10.16 Precision Planting

- 10.17 Raven

- 10.18 Topcon

- 10.19 Trimble

- 10.20 Yara