|

시장보고서

상품코드

1698228

아토피 피부염 치료제 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Atopic Dermatitis Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

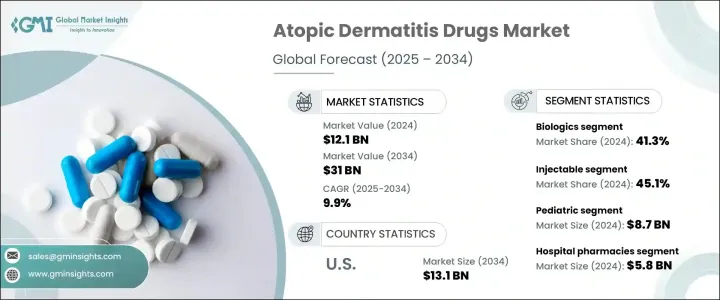

세계의 아토피 피부염 치료제 시장은 2024년에는 121억 달러로 평가되었고, 2025-2034년 연평균 복합 성장률(CAGR) 9.9%로 성장할 것으로 예측됩니다.

아토피 피부염 치료제는 피부의 염증, 가려움증, 건조함을 관리하고, 증상의 재연을 억제하며, 증상을 조절하는 데 도움이 됩니다. 이러한 치료에는 외용약, 전신요법, 생물학적 제제 등이 있으며 질환의 중증도에 따라 선택됩니다. 아토피 피부염의 유병률 상승, 강력한 의약품 파이프라인, 연구개발에 대한 투자의 증가가 시장 개척에 박차를 가하고 있습니다. 제약 기업은 신제품을 출시하고 있으며, 임상 시험의 양호한 결과가 수익 확대의 원동력이 되고 있습니다.

2023년 아토피 피부염 치료제 시장 규모는 111억 달러였으며, 2024년에는 생물학적 제제가 41.3%의 매출 점유율을 차지하여 시장을 견인했습니다. 생물학적 제제의 수요는, 그 뛰어난 치료 성적 및 제품 인가의 증가에 의해 상승을 계속하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 121억 달러 |

| 예측 금액 | 310억 달러 |

| CAGR | 9.9% |

투여 경로별로 시장은 주사제, 외용제, 경구제로 나뉩니다. 2024년 매출 점유율은 주사제가 45.1%로 우위를 차지했습니다. IL-4, IL-13, JAK 억제제 등 염증 경로를 표적으로 하는 새로운 생물학적 제제의 주사가 치료 옵션을 넓히고 있습니다. 규제 당국의 승인으로 제품의 상시가 가속화되어 주요 시장에서의 접근성과 채용률이 높아지고 있습니다.

환자층별 부문에는 소아와 성인 카테고리가 있습니다. 주로 소아에서 아토피 피부염의 이환율이 높기 때문에 2024년 매출은 소아 부문이 87억 달러로 최고였습니다. 소아 치료에 대한 수요는 규제 당국이 저 연령 환자를 위해 조정된 더 많은 치료법을 승인함에 따라 증가의 길을 따릅니다. 소아용으로 특별히 설계된 생물학적 제제의 신속한 승인은 시장 확대를 더욱 강화하고 있습니다.

유통 채널에는 병원 약국, 소매 약국, 전자상거래 등이 있습니다. 병원 약국은 2024년 58억 달러의 매출을 차지했습니다. 이 약국은 전문적인 치료 및 전신 치료가 필요한 환자를 관리하고 치료 결과와 잠재적 부작용을 적절하게 모니터링하는 데 중요한 역할을 합니다.

미국 시장은 상당한 성장을 이루고 있으며 매출액은 2023년 47억 달러에서 2034년 131억 달러에 달할 것으로 예측됩니다. 인지도 향상에 대한 노력과 광고 활동의 활성화는 연구 자금을 강화하고 고급 치료 옵션에 대한 환자 접근을 향상시킵니다. 규제 당국은 특히 중증 사례와 소아 환자에 대한 생물학적 제제의 승인을 계속해서 빠르게 진행하고 있으며, 시장 성장을 더욱 강화하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 아토피 피부염의 유병률 상승

- 생물학적 요법의 진보

- 피부과 의료에 대한 인식 및 접근 증가

- 업계의 잠재적 위험 및 과제

- 생물학적 제제 및 첨단 치료제의 고비용

- 부작용 및 컴플라이언스 문제

- 성장 촉진요인

- 성장 가능성의 분석

- 규제 상황

- 갭 분석

- 특허 분석

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 약제 클래스별(2021-2034년)

- 주요 동향

- 부신피질스테로이드제

- 칼시뉴린 억제제

- 생물제제

- 포스포디에스테라아제-4(PDE-4) 억제제

- 기타 약제 클래스별

제6장 시장 추계 및 예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 외용

- 경구

- 주사

제7장 시장 추계 및 예측 : 환자층별(2021-2034년)

- 주요 동향

- 소아

- 성인

제8장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 병원 약국

- 소매 약국

- 전자상거래

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AbbVie

- Arcutis Biotherapeutics

- Eli Lilly and Company

- Galderma Laboratories

- Incyte Corporation

- Leo Pharma

- Maruho

- Novartis

- Otsuka Pharmaceutical

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Viatris

The Global Atopic Dermatitis Drugs Market was valued at USD 12.1 billion in 2024 and is projected to grow at a 9.9% CAGR from 2025 to 2034. Atopic dermatitis drugs help manage skin inflammation, itching, and dryness, targeting flare-ups and controlling the condition. These treatments include topical medications, systemic therapies, and biologics, chosen based on disease severity. The rising prevalence of atopic dermatitis, strong drug pipelines, and increased investment in research and development are fueling market growth. Pharmaceutical companies are launching new products, and positive clinical trial results are driving revenue expansion.

In 2023, the atopic dermatitis drugs market was worth USD 11.1 billion. The biologics segment led the market in 2024, holding a 41.3% revenue share, driven by higher efficacy and long-term symptom control. The demand for biologics continues to rise due to their superior treatment outcomes and growing product approvals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.1 Billion |

| Forecast Value | $31 Billion |

| CAGR | 9.9% |

By route of administration, the market is divided into injectable, topical, and oral treatments. The injectable segment dominated in 2024 with a 45.1% revenue share. New biologic injections targeting inflammatory pathways, such as IL-4, IL-13, and JAK inhibitors, are expanding treatment options. Regulatory approvals have accelerated product launches, increasing accessibility and adoption rates in major markets.

The patient demographic segmentation includes pediatric and adult categories. The pediatric segment led with USD 8.7 billion in revenue in 2024, primarily due to the high incidence of atopic dermatitis in children. The demand for pediatric therapies continues to grow as regulatory bodies approve more treatments tailored for younger patients. Expedited approvals for biologic formulations specifically designed for pediatric use are further driving market expansion.

Distribution channels include hospital pharmacies, retail pharmacies, and e-commerce. Hospital pharmacies accounted for USD 5.8 billion in revenue in 2024. These pharmacies play a crucial role in managing patients who require specialized or systemic treatments, ensuring proper monitoring of therapy outcomes and potential side effects.

The U.S. market has witnessed significant growth, with revenue rising from USD 4.7 billion in 2023 to a projected USD 13.1 billion by 2034. Increased awareness efforts and advocacy initiatives are enhancing research funding and improving patient access to advanced treatment options. Regulatory agencies continue to fast-track the approval of biologics, particularly for severe cases and pediatric patients, further supporting market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of atopic dermatitis

- 3.2.1.2 Advancements in biologic therapies

- 3.2.1.3 Growing awareness and access to dermatological care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of biologic and advanced therapies

- 3.2.2.2 Side effects and compliance issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Pipeline analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroids

- 5.3 Calcineurin inhibitors

- 5.4 Biologics

- 5.5 Phosphodiesterase-4 (PDE-4) inhibitors

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Topical

- 6.3 Oral

- 6.4 Injectable

Chapter 7 Market Estimates and Forecast, By Patient Demographics, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatric

- 7.3 Adults

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Arcutis Biotherapeutics

- 10.3 Eli Lilly and Company

- 10.4 Galderma Laboratories

- 10.5 Incyte Corporation

- 10.6 Leo Pharma

- 10.7 Maruho

- 10.8 Novartis

- 10.9 Otsuka Pharmaceutical

- 10.10 Pfizer

- 10.11 Regeneron Pharmaceuticals

- 10.12 Sanofi

- 10.13 Viatris