|

시장보고서

상품코드

1698264

스마트홈 보안 카메라 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Smart Home Security Camera Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

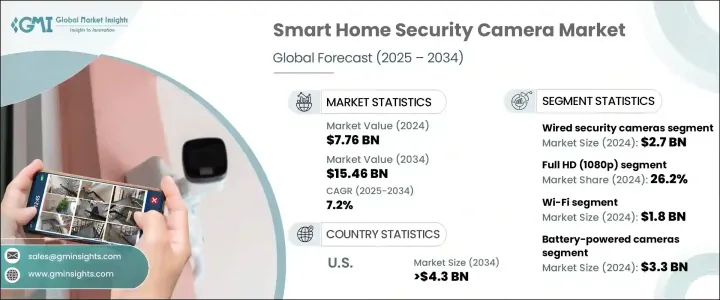

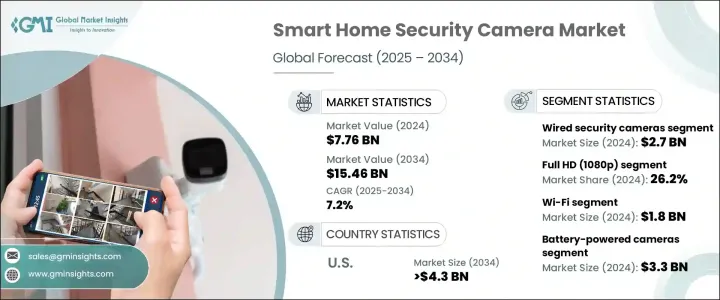

세계의 스마트홈 보안 카메라 시장 규모는 2024년에 77억 6,000만 달러로 평가되었고, 2025-2034년 연평균 복합 성장률(CAGR) 7.2%로 성장할 것으로 예측됩니다.

시장 확대는 스마트 홈 디바이스의 보급과 보안에 대한 관심 증가가 큰 요인이 되고 있습니다. 스마트 카메라, 잠금, 모션 센서는 필수적인 것이 되고 있으며, 홈 자동화 시스템과 매끄럽게 통합하면서 집을 원격 감시할 수 있습니다. 5G 네트워크 및 IoT 기술의 보급으로 스마트 보안 시스템의 성능은 크게 향상되고 있습니다. 게다가 스마트폰이나 음성 어시스턴트 유저수의 증가가 계속해서 시장의 성장을 지지하고 있어 보안 솔루션의 원활한 운용을 가능하게 하고 있습니다. 보안 위협의 고조는 고해상도 카메라, 클라우드 스토리지, AI 기반 위협 검출을 특징으로 하는 고급 감시 솔루션에 대한 요구를 더욱 높이고 있습니다.

시장은 유선 보안 카메라와 무선 보안 카메라로 나뉩니다. 2024년 유선 보안 카메라의 평가액은 27억 달러였습니다. 그 인기의 이유는 신뢰성 향상, 최적의 전력 공급, 뛰어난 영상 품질입니다. 게다가 파워 오버 이더넷(PoE) 기술에 의해 복수의 보안 기기 설치가 간소화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 77억 6,000만 달러 |

| 예측 금액 | 154억 6,000만 달러 |

| CAGR | 7.2% |

해상도별로는 HD(720p), 풀HD(1080p), 2K, 4K이상의 카메라가 포함되어 있습니다. 2024년 시장 점유율은 풀HD(1080p) 카메라가 26.2%를 차지했습니다. 이러한 카메라는, 신뢰성이 높은 접속성과 네트워크 비디오 레코더 및 집중 감시 시스템과의 호환성에 의해, 대규모 물건 및 상업 환경에서 널리 사용되고 있습니다.

이 시장은 Wi-Fi, Bluetooth, ZigBee 등의 연결 옵션에 따라 분류됩니다. Wi-Fi 지원 보안 카메라는 2024년에 18억 달러로 시장을 선도했습니다. Wi-Fi 대응 방범 카메라는 설치가 간단하고 홈 네트워크와의 원활한 통합이 가능하며 원격 액세스도 가능하기 때문에 보급이 진행되고 있습니다. 메쉬 와이파이 및 듀얼밴드 와이파이 기술 개발로 신뢰성이 향상되고 연결 문제와 시차가 감소하고 있습니다.

전원에 대해서는 시장은 전지식, 플러그인식, 태양전지식 카메라로 구성되어 있습니다. 2024년 평가액은 33억 달러로 배터리식 카메라가 이 분야를 지배했습니다. 태양열 충전, AI를 통한 에너지 관리, 리튬 이온 배터리 기술의 진보로 실내와 실외 모두에서 수요가 높아지고 있습니다. 포터블하고 DIY에 적합한 보안 솔루션에 대한 기호의 고조가, 계속 채용을 뒷받침하고 있습니다.

용도별로는 실내 보안이 급성장하고 있으며, CAGR은 10.4%로 예측되고 있습니다. 소비자도 기업도, 특히 아기나 애완동물의 감시, 고령자 케어를 위해, 실내 감시 솔루션에 대한 투자를 늘리고 있습니다. AI를 활용한 동체 감지, 얼굴 인식, 클라우드 스토리지는 이러한 보안 솔루션의 매력을 한층 더 높이고 있습니다.

유통 채널 부문에는 온라인 판매, 슈퍼마켓 및 하이퍼마켓, 전문점, 가전 양판점이 포함되어 있습니다. 온라인 판매는 2024년에 지배적인 부문으로 부상하여 30억 달러를 창출했습니다. 전자상거래에 대한 기호가 높아지고 있는 배경에는 경쟁력 있는 가격 설정, 제품의 다양성, 가격 비교의 편리성이 있습니다.

미국 시장은 범죄율 상승과 스마트 보안 솔루션 수요 증가에 힘입어 2034년에는 43억 달러 이상에 달할 것으로 예상되고 있습니다. 홈 자동화 및 보험 혜택과 보안 시스템의 통합이 시장 확대를 더욱 뒷받침하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 스마트 홈 디바이스의 보급 확대

- 보안에 대한 우려 증가

- 기술의 진보

- 접속성 향상 및 실시간 감시

- DIY에 의한 설치 및 비용 대비 효과

- 업계의 잠재적 위험 및 과제

- 고액의 초기 비용과 가입료

- 제한된 인터넷 연결 및 대역폭 문제

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 유선 보안 카메라

- 무선 보안 카메라

제6장 시장 추계 및 예측 : 해상도별(2021-2034년)

- 주요 동향

- HD(720p)

- 풀 HD(1080p)

- 2K

- 4K 이상

제7장 시장 추계 및 예측 : 커넥티비티별(2021-2034년)

- 주요 동향

- Wi-Fi

- Bluetooth

- Zigbee

- 기타

제8장 시장 추계 및 예측 : 동력원별(2021-2034년)

- 주요 동향

- 배터리 구동 카메라

- 플러그인 카메라

- 솔라 카메라

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 실내 보안

- 옥외 보안

제10장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 온라인 판매

- 전자상거래 플랫폼

- 브랜드 사이트

- 슈퍼마켓 및 하이퍼마켓

- 전문점

- 가전 양판점

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 뉴질랜드

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- UAE

- 사우디아라비아

- 남아프리카

제12장 기업 프로파일

- Abode Systems, Inc.

- ADT Inc.

- Arlo Technologies, Inc.

- Blink

- Canary Connect, Inc.

- D-Link Corporation

- Ecobee

- Eufy

- Frontpoint Security Solutions, LLC

- Google Nest

- Hikvision Digital Technology

- Lorex

- Reolink

- Ring

- Samsung Electronics Co., Ltd.

- SimpliSafe

- Synology

- TP-Link

- Ubiquiti Inc.

- Vivint Smart Home

- Wyze Labs, Inc.

- Xiaomi Inc.

- YI Technology

- Zmodo

The Global Smart Home Security Camera Market was valued at USD 7.76 billion in 2024 and is projected to grow at a CAGR of 7.2% from 2025 to 2034. Market expansion is largely driven by the increasing adoption of smart home devices and heightened security concerns. Smart cameras, locks, and motion sensors are becoming essential, allowing users to monitor their homes remotely while seamlessly integrating with home automation systems. The widespread adoption of 5G networks and IoT technology has significantly enhanced the performance of smart security systems. Moreover, the growing number of smartphone and voice assistant users continues to support market growth, enabling seamless operation of security solutions. Rising security threats have further fueled the need for advanced surveillance solutions featuring high-definition cameras, cloud storage, and AI-based threat detection.

The market is divided into wired and wireless security cameras. In 2024, wired security cameras held a valuation of USD 2.7 billion. Their popularity stems from enhanced reliability, optimal power supply, and superior video quality. Additionally, Power over Ethernet (PoE) technology has simplified the installation of multiple security devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.76 Billion |

| Forecast Value | $15.46 Billion |

| CAGR | 7.2% |

By resolution, the market includes HD (720p), Full HD (1080p), 2K, and 4K & above cameras. Full HD (1080p) cameras accounted for 26.2% of the market share in 2024. They are widely used in large properties and commercial settings due to their reliable connectivity and compatibility with network video recorders and centralized monitoring systems.

The market is also categorized by connectivity options, including Wi-Fi, Bluetooth, and ZigBee. Wi-Fi-enabled security cameras led the market with USD 1.8 billion in 2024. Their increasing adoption is attributed to easy installation, seamless integration with home networks, and remote access. The development of mesh and dual-band Wi-Fi technology has improved reliability while reducing connectivity issues and lag.

Regarding power sources, the market consists of battery-powered, plug-in, and solar-powered cameras. Battery-powered cameras dominated the segment with a valuation of USD 3.3 billion in 2024. Their demand is rising for both indoor and outdoor use due to advancements in solar charging, AI-driven energy management, and lithium-ion battery technology. The increasing preference for portable, DIY-friendly security solutions continues to drive adoption.

In terms of application, indoor security is witnessing rapid growth, with a projected CAGR of 10.4%. Consumers and businesses alike are increasingly investing in indoor surveillance solutions, particularly for baby and pet monitoring, as well as elderly care. AI-powered motion detection, facial recognition, and cloud storage further enhance the appeal of these security solutions.

The distribution channel segment includes online sales, supermarkets, hypermarkets, specialty stores, and electronics retailers. Online sales emerged as the dominant segment in 2024, generating USD 3 billion. The growing preference for e-commerce is driven by competitive pricing, product variety, and convenient price comparisons.

The U.S. market is expected to exceed USD 4.3 billion by 2034, fueled by rising crime rates and increased demand for smart security solutions. The integration of security systems with home automation and insurance incentives is further supporting market expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of smart home devices

- 3.2.1.2 Rising security concerns

- 3.2.1.3 Technological advancements

- 3.2.1.4 Improved connectivity and real-time monitoring

- 3.2.1.5 DIY installation and cost-effectiveness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost and subscription fees

- 3.2.2.2 Limited internet connectivity and bandwidth issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Mn)

- 5.1 Key trends

- 5.2 Wired security cameras

- 5.3 Wireless security cameras

Chapter 6 Market Estimates and Forecast, By Resolution, 2021 – 2034 (USD Mn)

- 6.1 Key trends

- 6.2 HD (720p)

- 6.3 Full HD (1080p)

- 6.4 2K

- 6.5 4K & Above

Chapter 7 Market Estimates and Forecast, By Connectivity, 2021 – 2034 (USD Mn)

- 7.1 Key trends

- 7.2 Wi-Fi

- 7.3 Bluetooth

- 7.4 Zigbee

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Power Source, 2021 – 2034 (USD Mn)

- 8.1 Key trends

- 8.2 Battery-powered cameras

- 8.3 Plug-in power cameras

- 8.4 Solar-powered cameras

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Mn)

- 9.1 Key trends

- 9.2 Indoor security

- 9.3 Outdoor security

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Mn)

- 10.1 Key trends

- 10.2 Online sales

- 10.2.1 E-commerce platforms

- 10.2.2 Brand websites

- 10.3 Supermarkets/Hypermarkets

- 10.4 Specialty stores

- 10.5 Electronics stores

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Abode Systems, Inc.

- 12.2 ADT Inc.

- 12.3 Arlo Technologies, Inc.

- 12.4 Blink

- 12.5 Canary Connect, Inc.

- 12.6 D-Link Corporation

- 12.7 Ecobee

- 12.8 Eufy

- 12.9 Frontpoint Security Solutions, LLC

- 12.10 Google Nest

- 12.11 Hikvision Digital Technology

- 12.12 Lorex

- 12.13 Reolink

- 12.14 Ring

- 12.15 Samsung Electronics Co., Ltd.

- 12.16 SimpliSafe

- 12.17 Synology

- 12.18 TP-Link

- 12.19 Ubiquiti Inc.

- 12.20 Vivint Smart Home

- 12.21 Wyze Labs, Inc.

- 12.22 Xiaomi Inc.

- 12.23 YI Technology

- 12.24 Zmodo