|

시장보고서

상품코드

1699399

데이터센터용 배터리 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Data Center Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

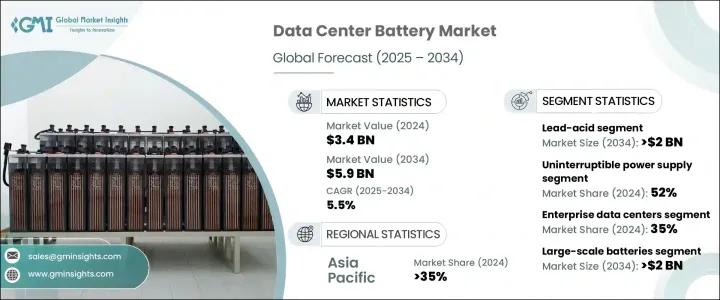

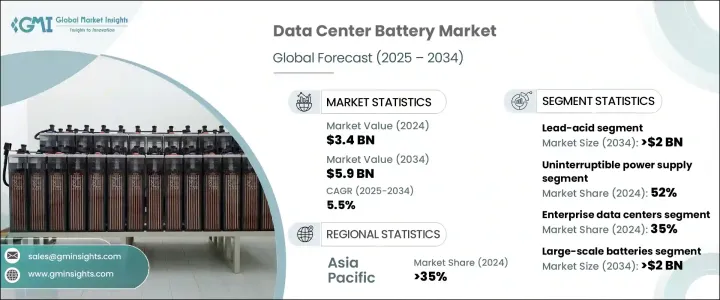

데이터센터용 배터리 세계 시장 규모는 2024년 34억 달러로 평가되었고, 2025-2034년 연평균 5.5% 성장할 것으로 예상됩니다.

에너지 효율적인 기술과 지속 가능한 솔루션에 대한 수요가 증가함에 따라 데이터센터 전원 관리의 전망이 재편되고 있습니다. 전 세계 기업들이 지속가능성을 우선시하는 가운데, 데이터센터는 환경에 미치는 영향을 최소화하기 위해 에너지 효율이 높은 배터리 솔루션으로 전략적으로 전환하고 있습니다. 재생 가능 에너지원의 채택이 증가하고 탄소 배출에 대한 정부 규제가 강화됨에 따라 첨단 배터리 기술에 대한 수요가 더욱 증가하고 있습니다.

이 진화하는 시장에서 가장 중요한 트렌드 중 하나는 기존 납축 배터리에서 리튬 이온 배터리로의 전환입니다. 기업들은 더 긴 수명, 더 높은 에너지 밀도, 더 적은 유지보수 요구 사항을 제공하는 고성능 에너지 저장 솔루션을 찾고 있습니다. 리튬 이온 배터리는 에너지 효율을 개선하고, 다운타임을 줄이며, 지속가능성 목표를 지원할 수 있는 능력으로 인해 선호되는 선택으로 부상하고 있습니다. 또한, 니켈-아연 및 기타 혁신적인 배터리 화학 물질과 같은 에너지 저장 기술의 발전은 보다 효율적이고 신뢰할 수 있는 솔루션을 제공함으로써 시장을 더욱 혁신적으로 변화시키고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 34억 달러 |

| 예상 금액 | 59억 달러 |

| CAGR | 5.5% |

데이터센터용 배터리 시장은 납축전지, 리튬 이온 배터리, 니켈 아연 배터리, 기타 기술 등 배터리 유형에 따라 분류되며, 2024년에는 납축전지가 시장 점유율의 40%를 차지할 것으로 예측됩니다. 오래된 기술임에도 불구하고 납축전지는 저렴한 가격과 신뢰성으로 인해 여전히 널리 사용되고 있습니다. 많은 데이터센터가 납축전지 시스템에 계속 투자하는 이유는 초기 비용이 저렴하고 무정전 전원 공급 장치(UPS) 용도에서 입증 된 실적이 있기 때문입니다. 또한, 밀폐형 납축전지의 발전으로 유지보수의 필요성이 최소화되어 기존 인프라에 실용적인 솔루션이 되고 있습니다.

UPS 시스템은 정전 시 즉각적인 백업 전력을 공급하고 원활한 운영을 보장하며 데이터 유출을 방지하기 위해 데이터센터에 중요한 역할을 하며, 2024년에는 UPS 분야가 52%의 점유율을 차지할 것으로 예상됩니다. 이러한 시스템은 또한 운영 중단으로 이어질 수 있는 전압 변동 및 전력 서지로부터 정밀 기기를 보호합니다. 리튬 이온 배터리는 긴 수명, 빠른 충전 기능, 높은 에너지 밀도로 인해 UPS 용도에서 인기를 얻고 있습니다. 데이터센터 사업자들이 보다 탄력적이고 효율적인 백업 전원 옵션을 요구함에 따라 리튬 이온 솔루션으로의 전환이 가속화되고 있습니다.

아시아태평양의 데이터센터용 배터리 시장은 2024년 35%의 점유율을 차지할 것으로 예상되며, 이는 다양한 산업 분야에서 디지털 인프라의 급속한 성장에 기인합니다. 클라우드 컴퓨팅, 인공지능, 데이터 기반 기술에 대한 의존도가 높아짐에 따라 이 지역에서는 안정적이고 지속 가능한 전력 솔루션에 대한 수요가 증가하고 있습니다. 아시아태평양 정부들은 재생 가능 에너지 도입을 적극적으로 추진하고 있으며, 이는 첨단 축전지 솔루션에 대한 투자 증가로 이어지고 있습니다. 이 지역의 데이터센터가 계속 확장됨에 따라 고성능의 친환경 에너지 저장 솔루션에 대한 수요는 향후에도 시장 성장의 주요 동력이 될 것으로 보입니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 원재료 공급업체

- 부품 공급업체

- 제조업체

- 기술 제공업체

- 서비스 제공업체

- 유통업체

- 최종 용도

- 공급업체 상황

- 이익률 분석

- 기술 및 혁신 전망

- 특허 분석

- 주요 뉴스와 이니셔티브

- 규제 상황

- 가격 동향

- 비용 내역 분석

- 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추산 및 예측 : 배터리별, 2021년-2034년

- 주요 동향

- 연산

- 구조별

- 침수형

- VRLA

- AGM

- 겔

- 구조별

- 리튬이온

- 화학별

- LFP

- LCO

- LTO

- NMC

- NCA

- LMO

- 화학별

- 니켈 아연

- 기타

제6장 시장 추산 및 예측 : 배터리 용량별, 2021년-2034년

- 주요 동향

- Small-scale batteries (Below 100 kWh)

- Medium-scale batteries (100 kWh - 1 MWh)

- Large-scale batteries (Above 1 MWh)

제7장 시장 추산 및 예측 : 데이터센터별, 2021년-2034년

- 주요 동향

- 기업 데이터센터

- 코로케이션 데이터센터

- 하이퍼스케일 데이터센터

- 엣지 데이터센터

제8장 시장 추산 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- UPS

- 백업 파워 써플라이 시스템

- 에너지 저장 시스템(ESS)

- 피크컷 및 load sharing

제9장 시장 추산 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카공화국

- 사우디아라비아

제10장 기업 개요

- Alpha Technologies

- C&D Technology

- Permanently closed

- Delta Electronics

- East Penn

- Energon

- EnerSys

- Exide Technologies

- FIAMM Energy Technology

- GS Yuasa

- Huawei Technologies

- Intercel

- Leoch

- LG Energy Solution

- MK BatteryUiPath

- Narada Power Source

- NorthStar Battery Company

- Power Sonic

- Saft Groupe

- Samsung SDI

The Global Data Center Battery Market was valued at USD 3.4 billion in 2024 and is expected to grow at a CAGR of 5.5% between 2025 and 2034. The increasing demand for energy-efficient technologies and sustainable solutions is reshaping the landscape of data center power management. As businesses worldwide prioritize sustainability, data centers are making strategic shifts toward energy-efficient battery solutions to minimize their environmental impact. The growing adoption of renewable energy sources and stringent government regulations on carbon emissions are further driving the demand for advanced battery technologies.

One of the most significant trends in this evolving market is the transition from traditional lead-acid batteries to lithium-ion batteries. Companies are seeking high-performance energy storage solutions that offer longer lifespans, higher energy density, and reduced maintenance requirements. Lithium-ion batteries are emerging as the preferred choice due to their ability to improve energy efficiency, reduce downtime, and support sustainability objectives. Additionally, advancements in energy storage technologies, such as nickel-zinc and other innovative battery chemistries, are further revolutionizing the market by providing more efficient and reliable solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 5.5% |

The data center battery market is categorized based on battery type, including lead-acid, lithium-ion, nickel-zinc, and other technologies. In 2024, lead-acid batteries accounted for 40% of the market share. Despite being an older technology, lead-acid batteries remain widely used due to their affordability and reliability. Many data centers continue to invest in lead-acid battery systems because of their lower initial costs and proven track record in uninterruptible power supply (UPS) applications. Additionally, sealed lead-acid battery advancements have minimized maintenance needs, making them a practical solution for existing infrastructure.

The market is also segmented by application, with the UPS segment holding a 52% share in 2024. UPS systems are critical for data centers as they provide immediate backup power during outages, ensuring seamless operations and preventing data loss. These systems also protect sensitive equipment from voltage fluctuations and power surges that can lead to operational disruptions. Lithium-ion batteries are gaining traction in UPS applications due to their extended lifespan, faster recharge capabilities, and higher energy density. This shift toward lithium-ion solutions is accelerating as data center operators seek more resilient and efficient backup power options.

Asia Pacific Data Center Battery Market held a 35% share in 2024, fueled by the rapid expansion of digital infrastructure across various industries. The increasing reliance on cloud computing, artificial intelligence, and data-driven technologies has heightened the need for stable and sustainable power solutions in the region. Governments in Asia Pacific are actively promoting renewable energy adoption, which has led to increased investments in advanced battery storage solutions. As data centers in this region continue to expand, the demand for high-performance and environmentally friendly energy storage solutions will remain a key market driver.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 Service providers

- 3.1.6 Distributors

- 3.1.7 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price trends

- 3.9 Cost breakdown analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Growing advancements in battery technology

- 3.10.1.2 Rising demand for Uninterrupted Power Supply (UPS)

- 3.10.1.3 Increase in data center power consumption

- 3.10.1.4 Rising construction of data centers across the globe

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial capital costs

- 3.10.2.2 Complexity in integration with existing infrastructure

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Lead-acid

- 5.2.1 By construction

- 5.2.1.1 Flooded

- 5.2.1.2 VRLA

- 5.2.1.2.1 AGM

- 5.2.1.2.2 GEL

- 5.2.1 By construction

- 5.3 Lithium-ion

- 5.3.1 By chemistry

- 5.3.1.1 LFP

- 5.3.1.2 LCO

- 5.3.1.3 LTO

- 5.3.1.4 NMC

- 5.3.1.5 NCA

- 5.3.1.6 LMO

- 5.3.1 By chemistry

- 5.4 Nickel zinc

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Battery Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Small-scale batteries (Below 100 kWh)

- 6.3 Medium-scale batteries (100 kWh - 1 MWh)

- 6.4 Large-scale batteries (Above 1 MWh)

Chapter 7 Market Estimates & Forecast, By Data Center, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Enterprise data centers

- 7.3 Colocation data centers

- 7.4 Hyperscale data centers

- 7.5 Edge data centers

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Uninterruptible power supply (UPS)

- 8.3 Backup power systems

- 8.4 Energy storage systems (ESS)

- 8.5 Peak shaving and load balancing

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alpha Technologies

- 10.2 C&D Technology

- 10.3 Permanently closed

- 10.4 Delta Electronics

- 10.5 East Penn

- 10.6 Energon

- 10.7 EnerSys

- 10.8 Exide Technologies

- 10.9 FIAMM Energy Technology

- 10.10 GS Yuasa

- 10.11 Huawei Technologies

- 10.12 Intercel

- 10.13 Leoch

- 10.14 LG Energy Solution

- 10.15 MK BatteryUiPath

- 10.16 Narada Power Source

- 10.17 NorthStar Battery Company

- 10.18 Power Sonic

- 10.19 Saft Groupe

- 10.20 Samsung SDI