|

시장보고서

상품코드

1708120

금속 캔 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Metal Cans Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

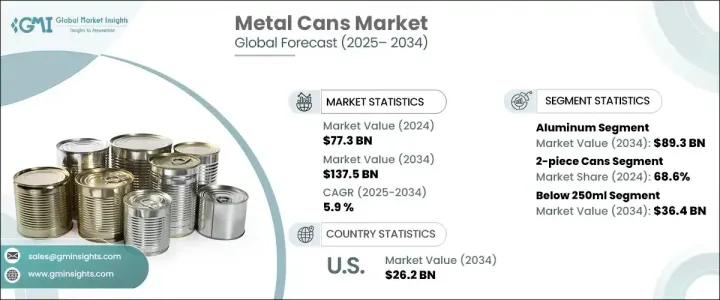

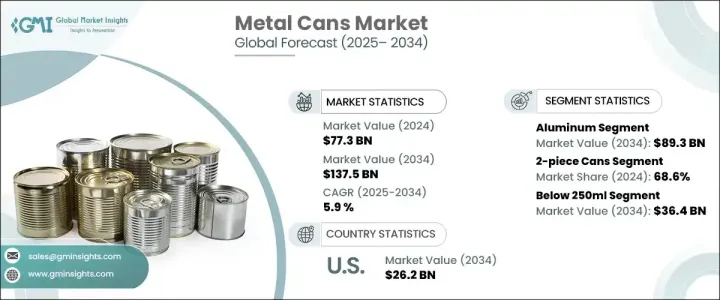

세계 금속 캔 시장은 2024년 773억 달러에 달했고, 2025-2034년 연평균 5.9% 성장할 것으로 예측됩니다.

금속 캔에 대한 수요 증가는 크래프트 맥주의 인기 급상승, 전자상거래의 확대, 지속 가능한 포장 솔루션에 대한 소비자 선호도 증가 등 몇 가지 주요 요인에 의해 촉진되고 있습니다. 환경 친화적이고 효율적이며 내구성이 뛰어난 포장에 대한 수요가 증가함에 따라 다양한 산업 분야의 기업들이 금속 캔으로 빠르게 전환하고 있습니다. 지속가능성이 최우선 과제로 떠오르면서 기업들은 플라스틱 폐기물을 줄이는 데 주력하고 있으며, 금속 캔은 재활용성, 경량성, 제품 보존성 향상으로 인해 매력적인 대안이 되고 있습니다.

수제 맥주 산업은 금속 캔 수요를 늘리는 데 중요한 역할을 하고 있습니다. 제품의 신선도와 품질을 효과적으로 유지할 수 있기 때문에 많은 독립 맥주 회사들이 알루미늄 캔을 채택하고 있습니다. 알루미늄 캔은 빛과 산소에 대한 보호 기능이 뛰어나 음료의 풍미를 유지하고 유통기한을 연장할 수 있습니다. 소비자의 선호도가 편리하고 지속 가능한 포장으로 계속 이동함에 따라 금속 캔에 대한 수요는 특히 음료 부문에서 가속화되고 있습니다. 기업들은 또한 고품질 인쇄와 선명한 디자인을 가능하게 하는 금속 캔이 제공하는 브랜딩 기회를 활용하여 선반에 대한 어필과 소비자의 관심을 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 773억 달러 |

| 예상 금액 | 1,375억 달러 |

| CAGR | 5.9% |

시장은 주로 알루미늄과 강철의 두 가지 재료 유형으로 나뉩니다. 알루미늄 캔은 2034년까지 893억 달러에 달할 것으로 예상되며, 그 우위는 재활용성, 경량성, 낮은 환경 영향에 기인합니다. 전 세계 정부와 환경 단체는 플라스틱 사용을 억제하기 위해 더 엄격한 규제를 시행하고 있으며, 산업계는 지속 가능한 대안으로 알루미늄 캔을 채택하도록 장려하고 있습니다. 또한, 각 브랜드는 알루미늄 포장으로 전환함으로써 지속가능성에 대한 약속을 강조하고 환경 친화적인 기업 이미지를 강화하기 위해 공동의 노력을 기울이고 있습니다. 이러한 변화는 소비자의 선호도에 의해 더욱 촉진되고 있으며, 친환경 포장 제품을 적극적으로 찾는 개인들이 증가하고 있습니다.

제품 유형별로 금속 캔은 2피스 유형과 3피스 유형으로 나뉩니다. 투피스 부문은 2024년 68.6% 시장 점유율을 차지했는데, 이는 주로 비용 효율성, 내구성, 낮은 재료 소비량으로 인한 것입니다. 투피스 캔은 특히 탄산음료, 조리식품 등 포장의 무결성과 사용 편의성이 중요한 요소인 음료 및 식품 산업에서 널리 선호되고 있습니다. 가볍고 재활용성이 높은 포장에 대한 수요는 향후 몇 년 동안 투피스 금속 캔의 채택을 촉진할 것으로 예측됩니다.

북미 금속 캔 시장은 2024년 25%의 점유율을 차지했으며, 지속가능성에 대한 노력이 이 지역의 괄목할 만한 성장을 주도하고 있습니다. 음료 제조업체들은 기업의 지속가능성 목표에 부합하고 진화하는 규제 기준을 준수하기 위해 알루미늄 캔으로 전환하고 있습니다. 친환경 대체품에 대한 수요는 환경 문제에 대한 우려뿐만 아니라 소비자의 기대에 힘입은 바 큽니다. 친환경 패키징을 장려하는 정부 프로그램과 플라스틱 폐기물을 줄이는 것을 우선시하는 주요 브랜드들의 노력으로 북미의 금속 캔 시장은 꾸준히 성장할 준비가 되어 있습니다. 기업들이 혁신적인 포장 솔루션과 재활용 이니셔티브에 투자함에 따라, 금속 캔은 다양한 산업 분야에서 지속가능한 포장의 미래를 형성하는 데 있어 매우 중요한 역할을 하게 될 것입니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 주요 시장 기업 - 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산 및 예측 : 재료별, 2021년-2034년

- 주요 동향

- 알루미늄

- 스틸

제6장 시장 추산 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- 2-piece cans

- 3-piece cans

제7장 시장 추산 및 예측 : 마개 타입별, 2021년-2034년

- 주요 동향

- Easy-open end (EOE)

- Peel-off end (POE)

- 기타

제8장 시장 추산 및 예측 : 용량별, 2021년-2034년

- 주요 동향

- 250ml 미만

- 250ml-1리터

- 1리터 이상

제9장 시장 추산 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 식품

- 과일 및 채소

- 편의 식품

- 반려동물 사료

- 육류 및 어개류

- 기타

- 음료

- 주류

- 탄산음료

- 스포츠 음료

- 기타

- 화장품 및 퍼스널케어

- 의약품

- 기타

제10장 시장 추산 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

제11장 기업 개요

- Ardagh Group

- Ball Corporation

- Canpack

- CCL Industries

- CPMC Holdings

- Crown Holdings

- DS Containers

- Envases Group

- Hindustan Tin Works

- Kian Joo Group

- Mauser Packaging

- P Wilkinson Containers

- Sapin

- Silgan Holdings

- Toyo Seikan

- Universal Can

- Visy

The Global Metal Cans Market reached USD 77.3 billion in 2024 and is projected to grow at a CAGR of 5.9% between 2025 and 2034. The increasing demand for metal cans is being fueled by several key factors, including the surging popularity of craft beer, the expansion of e-commerce, and a growing consumer inclination toward sustainable packaging solutions. Companies across industries are rapidly shifting to metal cans to meet the rising demand for eco-friendly, efficient, and durable packaging. With sustainability becoming a top priority, businesses are focusing on reducing plastic waste, making metal cans an attractive alternative due to their recyclability, lightweight nature, and enhanced product preservation capabilities.

The craft beer industry is playing a crucial role in boosting the demand for metal cans. Many independent breweries are embracing aluminum cans because they effectively maintain product freshness and quality. Aluminum cans offer superior protection against light and oxygen, which helps retain the flavor and extend the shelf life of beverages. As consumer preferences continue to shift toward convenient and sustainable packaging, the demand for metal cans is accelerating, particularly within the beverage sector. Companies are also capitalizing on the branding opportunities presented by metal cans, which allow for high-quality printing and vibrant designs, enhancing shelf appeal and consumer engagement.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $77.3 Billion |

| Forecast Value | $137.5 Billion |

| CAGR | 5.9% |

The market is primarily segmented into two material types: aluminum and steel. Aluminum cans are expected to reach USD 89.3 billion by 2034, with their dominance attributed to their recyclability, lightweight properties, and low environmental impact. Governments and environmental organizations worldwide are enforcing stricter regulations to curb plastic usage, prompting industries to adopt aluminum cans as a sustainable alternative. Brands are also making concerted efforts to highlight their sustainability commitments by switching to aluminum packaging, reinforcing their image as eco-conscious enterprises. This shift is further supported by consumer preferences, as a growing number of individuals actively seek out products with environmentally friendly packaging.

In terms of product type, metal cans are available in two-piece and three-piece formats. The two-piece segment held a 68.6% market share in 2024, largely due to its cost-effectiveness, durability, and lower material consumption. Two-piece cans are widely preferred in the food and beverage industry, especially for carbonated drinks and ready-to-eat meals, where packaging integrity and ease of use are critical factors. The demand for lightweight and highly recyclable packaging is expected to continue driving the adoption of two-piece metal cans in the coming years.

North America Metal Cans Market held a 25% share in 2024, with sustainability initiatives driving significant growth in the region. Beverage companies are increasingly transitioning to aluminum cans to align with their corporate sustainability goals and comply with evolving regulatory standards. The push for eco-friendly alternatives is not only being driven by environmental concerns but also by consumer expectations. With government programs promoting green packaging and leading brands prioritizing the reduction of plastic waste, the metal cans market in North America is poised for steady expansion. As businesses invest in innovative packaging solutions and recycling initiatives, metal cans are set to play a pivotal role in shaping the future of sustainable packaging across various industries.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Enhanced recycling efficiency and circular economy integration

- 3.2.1.2 Increasing sales of craft beer

- 3.2.1.3 Rising demand for on-the-go food and beverages

- 3.2.1.4 Global expansion of e-commerce platforms

- 3.2.1.5 Proliferation of non-alcoholic beverages in cans

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental impact of mining for metal

- 3.2.2.2 Increased regulatory scrutiny on metal packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Bn & Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

Chapter 6 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Bn & Units)

- 6.1 Key trends

- 6.2 2-piece cans

- 6.3 3-piece cans

Chapter 7 Market Estimates and Forecast, By Closure Type, 2021 - 2034 (USD Bn & Units)

- 7.1 Key trends

- 7.2 Easy-open end (EOE)

- 7.3 Peel-off end (POE)

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Capacity, 2021 - 2034 (USD Bn & Units)

- 8.1 Key trends

- 8.2 Below 250ml

- 8.3 250ml - 1 liter

- 8.4 Above 1 liter

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Bn & Units)

- 9.1 Key trends

- 9.2 Food

- 9.2.1 Fruits & vegetables

- 9.2.2 Convenience foods

- 9.2.3 Pet foods

- 9.2.4 Meat & seafood

- 9.2.5 Others

- 9.3 Beverages

- 9.3.1 Alcoholic beverages

- 9.3.2 Carbonated soft drinks

- 9.3.3 Sports & energy drinks

- 9.3.4 Others

- 9.5 Cosmetics and personal care

- 9.6 Pharmaceuticals

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Bn & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Ardagh Group

- 11.2 Ball Corporation

- 11.3 Canpack

- 11.4 CCL Industries

- 11.5 CPMC Holdings

- 11.6 Crown Holdings

- 11.7 DS Containers

- 11.8 Envases Group

- 11.9 Hindustan Tin Works

- 11.10 Kian Joo Group

- 11.11 Mauser Packaging

- 11.12 P Wilkinson Containers

- 11.13 Sapin

- 11.14 Silgan Holdings

- 11.15 Toyo Seikan

- 11.16 Universal Can

- 11.17 Visy