|

시장보고서

상품코드

1708158

자동차 연료 공급 펌프 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automotive Fuel Feed Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

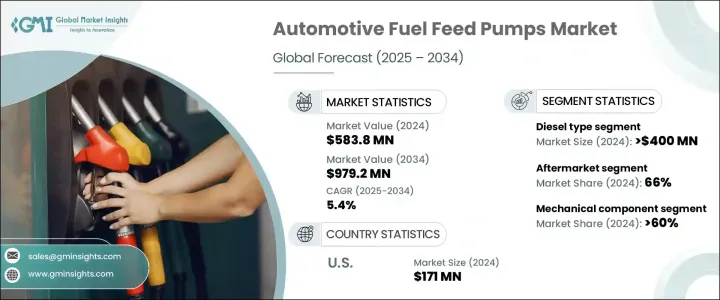

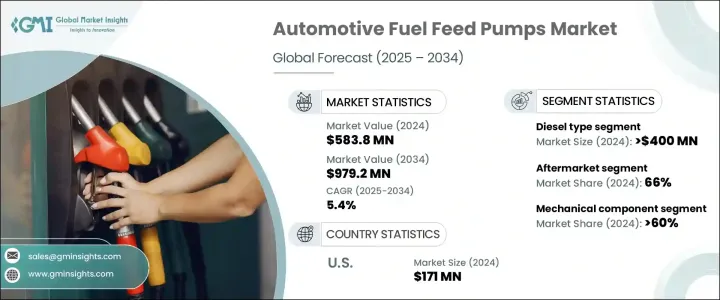

자동차 연료 공급 펌프 세계 시장은 2024년에는 5억 8,380만 달러에 달했고, 2025-2034년 5.4%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

이 시장은 선진국과 신흥 경제국의 자동차 생산 및 판매 급증에 힘입어 꾸준히 확대되고 있습니다. 중국, 인도, 브라질 등 급성장 시장에서 도시화가 가속화되고 가처분 소득이 증가함에 따라 승용차 및 상용차 수요도 급증하고 있습니다. 더 많은 차량이 운행됨에 따라 효율적인 연료 공급 펌프 시스템의 필요성이 증가하고 있습니다. 이러한 부품은 원활한 연료 공급과 엔진 성능 유지에 중요한 역할을 하기 때문입니다.

또한, 연비 향상과 배기가스 규제 강화 등 자동차 공학의 기술적 진보도 첨단 연료 공급 펌프의 채택을 촉진하고 있습니다. 또한, 자동차 제조업체들이 엔진의 내구성과 연료 사용량 최적화를 우선순위에 두면서 세계 자동차 부문이 하이브리드 엔진과 첨단 내연기관으로 전환하고 있는 것도 고성능 연료 공급 펌프 시스템에 대한 수요를 자극하고 있습니다. 또한, 자동차 보유량의 노후화로 인한 교체 부품에 대한 수요 증가와 자동차 배기가스 및 성능에 대한 정부 규제 강화는 시장 역학에 영향을 미치며 전 세계 OEM 및 애프터마켓 공급업체 모두에게 일관된 성장 기회를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 5억 8,380만 달러 |

| 예상 금액 | 9억 7,920만 달러 |

| CAGR | 5.4% |

자동차 연료 공급 펌프 시장은 엔진의 유형에 따라 가솔린과 디젤로 구분됩니다. 이 중 디젤 엔진용 연료 공급 펌프의 2024년 매출액은 4억 달러에 달했습니다. 디젤 엔진은 트럭, 버스, 건설기계와 같은 상용차 및 산업용 차량에 널리 사용되며, 모두 고효율 및 내구성이 뛰어난 연료 공급 시스템을 필요로 합니다. 디젤 연료 공급 펌프는 엔진 출력을 최적화하고, 연료 효율을 개선하며, 엔진의 장기적인 신뢰성을 보장하는 고압 연료 분사 시스템을 지원하는 데 필수적입니다. 특히 건설, 물류, 대중교통 분야에서 대형 차량에 대한 세계 수요가 증가함에 따라 견고한 디젤 연료 공급 펌프에 대한 요구가 증가하고 있습니다. 이러한 펌프는 가혹한 운전 조건에 대응할 수 있는 능력으로 인해 다양한 산업 분야의 고성능 차량에 필수적인 부품으로 자리 잡고 있습니다.

자동차 연료 공급 펌프의 판매는 OEM 채널과 애프터마켓 채널로 나뉩니다. 애프터마켓 부문은 2024년 66%의 점유율을 차지할 것으로 예상되며, 이는 자동차의 노후화로 인해 펌프 교체 수요가 증가하고 있기 때문입니다. 연료 공급 펌프는 시간이 지남에 따라 마모되어 차량의 성능과 안전성을 유지하기 위해 교체가 필요합니다. 소비자와 차량 운영자 모두 쉽게 구할 수 있고, 다양한 차종에 적합하며, 비용 효율적이고 신뢰할 수 있는 애프터마켓 솔루션을 원하고 있습니다. 애프터마켓의 다양한 제품 가용성과 합리적인 가격은 다양한 고객층을 계속 끌어들이고 있으며, 시장 상황의 중요한 부분을 차지하고 있습니다.

미국의 자동차 연료 공급 펌프 시장은 2024년에 1억 7,100만 달러 규모에 달했으며, 2025년부터 2034년까지 연평균 5.5%의 성장률을 보일 것으로 예측됩니다. 이러한 성장의 주요 원동력은 미국의 높은 자동차 보유량과 강력한 자동차 제조 생태계에 기인합니다. 미국에서는 자동차의 평균 연식이 증가함에 따라 애프터마켓 연료 공급 펌프에 대한 수요가 증가하고 있습니다. 미국의 견고한 교체 시장은 성능과 수명에 대한 소비자의 기대에 부응하는 고품질의 내구성 있는 연료 공급 펌프의 필요성을 강조하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 원재료 제조업체

- 부품 제조업체

- 제조업체

- 기술 제공업체

- 유통 채널 분석

- 최종 용도

- 이익률 분석

- 공급업체 상황

- 기술 및 혁신 전망

- 특허 분석

- 규제 상황

- 비용 내역 분석

- 주요 뉴스 및 이니셔티브

- 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추산 및 예측 : 엔진별, 2021년-2034년

- 주요 동향

- 가솔린

- 디젤

제6장 시장 추산 및 예측 : 컴포넌트별, 2021년-2034년

- 주요 동향

- 메커니컬

- 전동

- 터보 펌프

제7장 시장 추산 및 예측 : 자동차별, 2021년-2034년

- 주요 동향

- 승용차

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 이륜차

제8장 시장 추산 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 직접 분사 시스템

- 멀티 포인트 분사 시스템

- 연료 분사 시스템

- Carbureted engines

- 고성능차

제9장 시장 추산 및 예측 : 판매채널별, 2021년-2034년

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추산 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카공화국

- 사우디아라비아

제11장 기업 개요

- Aisin Seiki

- AST Otomotiv

- Carter Fuel

- Continental

- Daimler

- Delphi Automotive

- DENSO

- DEUTZ

- Devendra

- HELLA

- Hitachi Astemo

- Johnson Electric

- Perkins Engines

- Rheinmetall

- Robert Bosch

- Scania

- Schaeffler

- SHW

- Valeo

- ZF Friedrichshafen

The Global Automotive Fuel Feed Pumps Market was valued at USD 583.8 million in 2024 and is projected to grow at a CAGR of 5.4% between 2025 and 2034. The market is witnessing steady expansion driven by surging vehicle production and sales across both developed and emerging economies. As urbanization accelerates and disposable incomes rise in fast-growing markets like China, India, and Brazil, the demand for passenger and commercial vehicles is also rising sharply. With more vehicles on the road, the need for efficient fuel feed pump systems is growing, as these components play a crucial role in ensuring seamless fuel delivery and maintaining engine performance.

Additionally, technological advancements in automotive engineering, including the push toward better fuel efficiency and emission control, are fueling the adoption of advanced fuel feed pumps. The global automotive sector's shift toward hybrid and advanced internal combustion engines is also stimulating the demand for high-performance fuel feed pump systems as automakers prioritize engine durability and optimized fuel usage. Furthermore, the increasing need for replacement parts due to aging vehicle fleets, combined with stricter government regulations for vehicle emissions and performance, is influencing market dynamics and creating consistent growth opportunities for both OEM and aftermarket suppliers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $583.8 Million |

| Forecast Value | $979.2 Million |

| CAGR | 5.4% |

The automotive fuel feed pump market is segmented based on engine type into gasoline and diesel categories. Among these, diesel engine fuel feed pumps accounted for USD 400 million in revenue in 2024. Diesel-powered engines are widely used in commercial and industrial vehicles, including trucks, buses, and construction machinery, all of which require highly efficient and durable fuel delivery systems. Diesel fuel feed pumps are essential in supporting high-pressure fuel injection systems that optimize engine power, improve fuel efficiency, and ensure long-term engine reliability. As global demand for heavy-duty vehicles grows, particularly in the construction, logistics, and public transportation sectors, the need for robust diesel fuel feed pumps is rising. These pumps are favored for their ability to handle extreme operating conditions, making them indispensable components in high-performance vehicles across a range of industries.

Sales of automotive fuel feed pumps are classified into OEM (original equipment manufacturer) and aftermarket channels. The aftermarket segment dominated with a 66% share in 2024, largely due to the rising need for replacement pumps as vehicles age. Over time, fuel feed pumps experience wear and require replacement to maintain vehicle performance and safety. Consumers and fleet operators alike seek cost-effective and reliable aftermarket solutions that are readily available and compatible with a variety of vehicle models. The aftermarket's broad product availability and affordability continue to attract a diverse customer base, making it a critical part of the market landscape.

The U.S. automotive fuel feed pumps market generated USD 171 million in 2024, with expectations to grow at a CAGR of 5.5% from 2025 to 2034. This growth is primarily driven by the country's substantial vehicle fleet and a strong automotive manufacturing ecosystem. The rising average age of vehicles in the U.S. amplifies the demand for aftermarket fuel feed pumps as replacements become essential to keep vehicles operational and efficient. The robust replacement market in the U.S. highlights the need for high-quality, durable fuel feed pumps that align with consumer expectations for performance and longevity.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing vehicle production & sales

- 3.7.1.2 Stringent emission regulations

- 3.7.1.3 Growing demand for fuel-efficient vehicles

- 3.7.1.4 Advancements in automotive technology

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High R&D costs for innovation

- 3.7.2.2 Stricter vehicle safety & performance standards

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Diesel

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Mechanical

- 6.3 Electric

- 6.4 Turbopump

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicle

- 7.3 Commercial Vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

- 7.4 Two wheelers

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Direct injection system

- 8.3 Multipoint injection system

- 8.4 Fuel injection system

- 8.5 Carbureted engines

- 8.6 High-performance vehicles

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 AST Otomotiv

- 11.3 Carter Fuel

- 11.4 Continental

- 11.5 Daimler

- 11.6 Delphi Automotive

- 11.7 DENSO

- 11.8 DEUTZ

- 11.9 Devendra

- 11.10 HELLA

- 11.11 Hitachi Astemo

- 11.12 Johnson Electric

- 11.13 Perkins Engines

- 11.14 Rheinmetall

- 11.15 Robert Bosch

- 11.16 Scania

- 11.17 Schaeffler

- 11.18 SHW

- 11.19 Valeo

- 11.20 ZF Friedrichshafen