|

시장보고서

상품코드

1708171

내시경 검사용 AI 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)AI in Endoscopy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

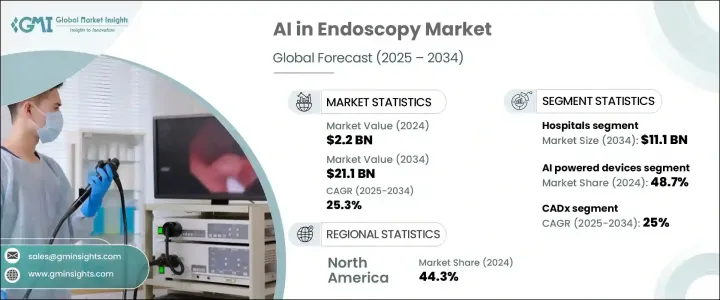

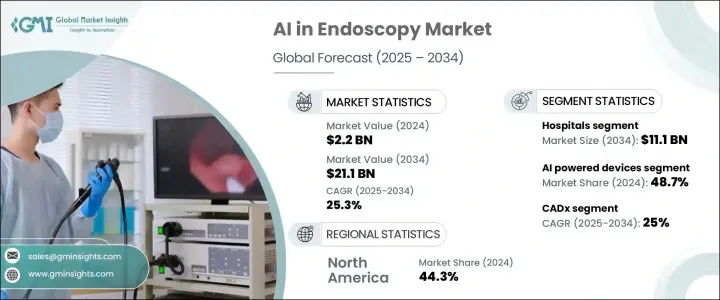

내시경 검사용 AI 세계 시장은 2024년 22억 달러로 평가되었고, 2025년부터 2034년까지 25.3%의 견고한 CAGR로 확대될 것으로 예측됩니다.

이 시장의 급격한 성장은 전 세계적으로 소화기 질환 및 관련 질환의 급증으로 인한 첨단 진단 도구에 대한 수요 증가를 반영하고 있습니다. 대장암, 염증성 장질환, 소화성 궤양과 같은 소화기 질환이 증가함에 따라 의료 시스템은 보다 정확하고 신속하며 신뢰할 수 있는 진단을 제공할 수 있는 솔루션이 절실히 요구되고 있습니다. AI 기반 내시경은 임상의가 실시간으로 이상을 발견하고 치료하는 혁신적인 도구로 부상하고 있습니다. 인공지능은 현재 진단 정확도를 높이고, 임상 워크플로우를 간소화하며, 예측적 통찰력을 제공하는 데 있어 매우 중요한 역할을 하고 있으며, 이 모든 것이 환자 예후 개선에 기여하고 있습니다.

내시경 검사에 AI를 도입하면 의사는 병변, 종양, 폴립을 보다 정확하게 식별할 수 있어 인적 오류를 크게 줄이고 조기 진단율을 향상시킬 수 있습니다. 전 세계 의료 서비스 제공업체들이 최소침습적 시술에 집중하는 가운데, AI 기술은 향상된 시각화, 실시간 분석, 자동 감지 기능을 제공하고 궁극적으로 임상적 의사결정 과정을 개선하는 데 필수적인 요소로 자리 잡고 있습니다. 플랫폼의 통합과 함께 AI 기반 내시경 솔루션에 대한 수요를 더욱 촉진하고 있으며, 이 시장은 의료기기 제조업체와 의료 기관에게도 마찬가지로 중요한 초점이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 22억 달러 |

| 예상 금액 | 211억 달러 |

| CAGR | 25.3% |

내시경 검사의 AI 시장은 위장, 비뇨기, 호흡기, 대장내시경, 기타 등 시술 유형에 따라 세분화됩니다. 이 중 소화기 내시경 검사 분야가 2023년 6억 3,120만 달러의 매출을 기록했습니다. 이는 주로 소화기 질환의 유병률 증가에 힘입은 것입니다. 컴퓨터 보조 검출(CADe) 시스템과 같은 AI 기반 솔루션은 용종이나 종양과 같은 이상을 정확하게 식별할 수 있게 함으로써 위장 내시경 검사에 변화를 가져오고 있으며, AI를 활용한 실시간 영상 분석 및 이미지 향상 기술을 특징으로 하는 도구는 진단 속도와 정확도를 향상시키고 진단 속도와 정확도를 향상시키고 신속한 임상 개입을 촉진하고 있습니다. 이러한 발전으로 병원 및 클리닉은 표준 진단 프로토콜의 일부로 AI 기반 내시경 검사 도구를 채택하고 있습니다.

구성 요소 측면에서 시장은 AI 기반 장치, 소프트웨어, 서비스로 구분되며, AI 기반 장치 부문은 첨단 진단 및 시각화 기술에 대한 선호도가 높아지면서 2024년 48.7%의 점유율을 차지했습니다. 이러한 기기들은 의료 서비스 제공업체가 보다 정밀하고 효율적인 내시경 시술을 수행할 수 있도록 지원하며, 보다 신속한 진단과 치료를 돕습니다. 최소침습적 개입으로의 전환은 실시간 AI 기능과 함께 최적화된 결과를 위해 AI 소프트웨어와 원활하게 통합된 소형의 고성능 내시경 도구 개발에 있어 중요한 기술 혁신을 주도하고 있습니다.

지역별로는 북미가 2024년 44.3%의 점유율로 내시경 검사 AI 시장을 주도했으며, 강력한 헬스케어 인프라와 AI 기술의 조기 도입으로 미국이 선두를 달리고 있습니다. 기술 제공업체와 의료기관의 지속적인 공동 개발이 혁신적인 제품 개발을 촉진하고 시장 침투를 가속화하고 있습니다. 이 지역의 R&D에 대한 적극적인 투자와 절차 효율성과 환자 치료를 개선하기 위한 AI 통합에 대한 집중적인 노력은 세계 시장에서 이 지역의 입지를 지속적으로 강화하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- 규제 상황

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업 - 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산 및 예측 : 내시경 유형별, 2021년-2034년

- 주요 동향

- 소화기 내시경

- 비뇨기 내시경

- 호흡기 내시경

- 대장 내시경

- 기타 유형

제6장 시장 추산 및 예측 : 컴포넌트별, 2021년-2034년

- 주요 동향

- AI 탑재 디바이스

- 소프트웨어

- 서비스

제7장 시장 추산 및 예측 : CAD 유형별, 2021년-2034년

- 주요 동향

- CADx

- CADe

제8장 시장 추산 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원

- 전문 클리닉

- 기타 최종 용도

제9장 시장 추산 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 개요

- Ambu

- Fujifilm

- Hoya

- Intuitive Surgical

- Iterative Scopes

- Magentiq Eye

- Medtronic

- NEC Corporation

- Odin Vision

- Olympus

- PENTAX Medical

- Wision Al

- Wuhan EndoAngel Medical Technology

The Global AI in Endoscopy Market was valued at USD 2.2 billion in 2024 and is projected to expand at a robust CAGR of 25.3% from 2025 to 2034. The rapid growth of this market reflects the increasing demand for advanced diagnostic tools driven by a surge in gastrointestinal and related disorders worldwide. As gastrointestinal diseases, including colorectal cancer, inflammatory bowel disease, and peptic ulcers, continue to rise, healthcare systems are urgently seeking solutions that offer more accurate, faster, and reliable diagnoses. AI-powered endoscopy is emerging as a transformative tool that is reshaping how clinicians detect and treat abnormalities in real time. Artificial intelligence is now playing a pivotal role in enhancing diagnostic accuracy, streamlining clinical workflows, and delivering predictive insights, all contributing to better patient outcomes.

The integration of AI in endoscopy procedures allows physicians to identify lesions, tumors, and polyps with higher precision, significantly reducing human error and improving early diagnosis rates. With healthcare providers worldwide focusing on minimally invasive procedures, AI technologies are becoming essential in providing enhanced visualization, real-time analysis, and automated detection, ultimately improving clinical decision-making processes. The continuous evolution of AI algorithms, coupled with the integration of high-definition imaging and robotic-assisted platforms, is further driving the demand for AI-based endoscopy solutions, making this market a critical focus for medical device manufacturers and healthcare institutions alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $21.1 Billion |

| CAGR | 25.3% |

The AI in endoscopy market is segmented based on procedure types, including gastrointestinal, urological, respiratory, colonoscopy, and others. Among these, the gastrointestinal endoscopy segment dominated the market and generated USD 631.2 million in 2023, largely propelled by the rising prevalence of gastrointestinal conditions. AI-driven solutions such as computer-aided detection (CADe) systems are transforming gastrointestinal endoscopy by enabling precise identification of abnormalities like polyps and tumors. Tools featuring AI-powered real-time video analysis and image enhancement technologies are improving diagnostic speeds and accuracy, facilitating quicker clinical interventions. These advancements are encouraging hospitals and clinics to adopt AI-based endoscopy tools as part of their standard diagnostic protocols.

From a component perspective, the market is divided into AI-powered devices, software, and services. The AI-powered devices segment accounted for a 48.7% share in 2024, underpinned by the growing preference for advanced diagnostic and visualization technologies. These devices are enabling healthcare providers to perform more targeted and efficient endoscopic procedures, supporting faster diagnosis and treatment. The shift toward minimally invasive interventions, coupled with real-time AI capabilities, is driving significant innovations in the development of compact, high-performance endoscopic tools that integrate seamlessly with AI software for optimized outcomes.

Regionally, North America led the AI in endoscopy market with a 44.3% share in 2024, spearheaded by the U.S. due to its strong healthcare infrastructure and early adoption of AI technologies. Ongoing collaborations between technology providers and healthcare institutions are fostering innovative product development and accelerating market penetration. The region's proactive investment in R&D and focus on integrating AI to improve procedural efficiency and patient care continue to strengthen its position in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of gastrointestinal and respiratory diseases

- 3.2.1.2 Rising adoption of minimally invasive surgeries

- 3.2.1.3 Advancements in AI algorithms for real-time imaging and diagnostics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and equipment costs

- 3.2.2.2 Regulatory and ethical challenges in AI deployment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type of Endoscopy, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Gastrointestinal endoscopy

- 5.3 Urological endoscopy

- 5.4 Respiratory endoscopy

- 5.5 Colonoscopy

- 5.6 Other types

Chapter 6 Market Estimates and Forecast, By Component, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 AI powered devices

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By Type of CAD, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 CADx

- 7.3 CADe

Chapter 8 Market Estimates and Forecast, End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 Fujifilm

- 10.3 Hoya

- 10.4 Intuitive Surgical

- 10.5 Iterative Scopes

- 10.6 Magentiq Eye

- 10.7 Medtronic

- 10.8 NEC Corporation

- 10.9 Odin Vision

- 10.10 Olympus

- 10.11 PENTAX Medical

- 10.12 Wision Al

- 10.13 Wuhan EndoAngel Medical Technology