|

시장보고서

상품코드

1708190

푸드서비스용 일회용품 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Food Service Disposable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

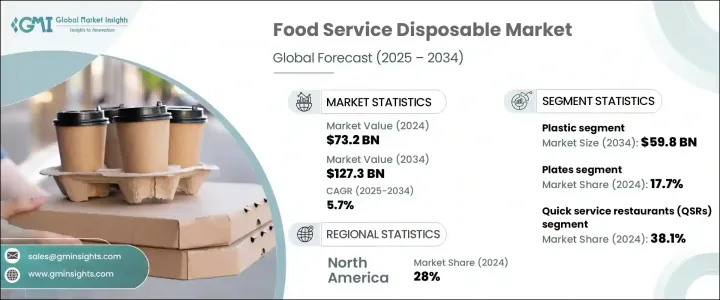

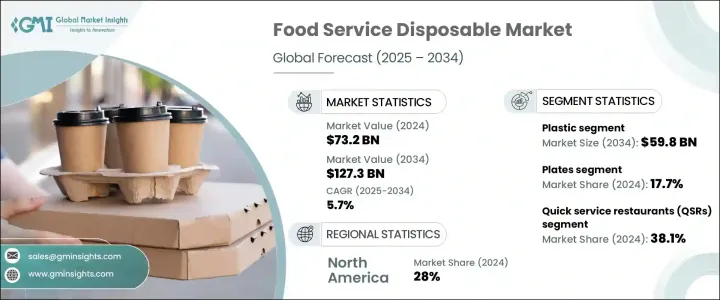

세계의 푸드서비스용 일회용품 시장은 2024년에 732억 달러로 평가되며, 2025-2034년에 CAGR 5.7%로 성장할 것으로 예측됩니다.

이러한 성장의 주요 원인은 퀵서비스 레스토랑(QSR)의 급격한 확장과 온라인 음식 배달 플랫폼의 급격한 증가에 기인합니다. 도시화와 소비자 라이프스타일의 변화로 인해 편의성에 대한 선호도가 높아지면서 QSR은 위생, 운영 효율성 및 비용 효율성을 보장하기 위해 다양한 푸드서비스용 일회용품을 사용하게 되었습니다. 이 분야의 제조업체는 QSR 증가하는 수요를 충족시키기 위해 고품질의 비용 효율적이고 환경적으로 지속가능한 일회용 제품 생산에 집중해야 합니다. 시장이 계속 확대됨에 따라 위생과 기능성을 향상시키는 친환경 소재와 혁신적인 디자인에 대한 투자는 외식 산업의 진화하는 요구 사항을 충족하는 데 매우 중요합니다.

동시에 전 세계에서 온라인 음식 배달 서비스가 증가함에 따라 내구성이 뛰어나고 안전한 일회용 포장에 대한 수요가 증가하고 있습니다. 디지털 주문, 앱 기반 푸드서비스, 클라우드 키친의 인기가 높아짐에 따라 포장 업체는 식품 안전과 배송 효율성을 유지하면서 오래 지속되고, 누출 방지 및 변조 방지 기능을 갖춘 포장 솔루션을 개발해야 합니다. 소비자들 사이에서 건강에 대한 관심이 높아지면서 식품에 안전하고 지속가능한 생분해성 소재에 대한 관심도 높아지고 있습니다. 푸드서비스용 일회용품 제조업체는 온라인 식품 주문 시스템의 급속한 성장을 지원할 뿐만 아니라 친환경적인 선택을 원하는 소비자의 선호에 부합하는 포장재 개발에 중점을 두어야 합니다.

| 시장 범위 | |

|---|---|

| 개시연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 개시 금액 | 732억 달러 |

| 예측 금액 | 1,273억 달러 |

| CAGR | 5.7% |

시장은 재료별로 종이/판지, 플라스틱, 알루미늄, 기타로 구분됩니다. 플라스틱 분야는 2034년까지 598억 달러 규모 시장을 창출할 것으로 예상됩니다. 지속가능성에 대한 우려와 규제 압력이 증가함에 따라 플라스틱 분야는 재활용 및 생분해성 솔루션 개발로 전환하고 있습니다. 퇴비화 가능한 플라스틱과 첨단 재활용 기술의 새로운 혁신은 친환경 포장에 대한 고객의 요구와 외식업계의 편의성 및 내구성 요구 사이의 균형을 맞추기 위한 기업의 노력으로 인해 호응을 얻고 있습니다.

제품 유형별로 시장은 접시, 트레이, 그릇, 컵, 조개껍데기, 랩 필름, 호일, 기타로 나뉩니다. 접시는 2024년 시장 점유율의 17.7%를 차지했습니다. 접시에 대한 수요는 QSR, 포장마차, 온라인 푸드서비스의 성장으로 인해 편리하고 이동 중에도 먹을 수 있는 솔루션에 대한 요구가 높아진 데 따른 것입니다. 일회용, 위생적인 식용 솔루션에 대한 소비자의 선호도가 이 부문의 성장에 더욱 기여하고 있습니다. 또한 지속가능한 대안을 찾는 움직임으로 인해 종이, 대나무, 사탕수수 등의 재료를 사용한 퇴비화 및 생분해성 접시 개발이 진행되고 있습니다.

최종 용도별로는 QSR, 풀 서비스 레스토랑(FSR), 케이터링 서비스, 온라인 배달, 기타로 구분되며, 2024년에는 QSR 부문이 38.1%의 점유율로 시장을 주도할 것으로 예상됩니다. 세계 및 지역적 QSR 체인의 확장과 급속한 현대화는 테이크아웃 및 배달시 음식의 품질을 유지하면서 휴대성을 향상시키는 가볍고 내구성이 뛰어나며 유연한 재료를 채택하는 데 박차를 가하고 있습니다.

북미는 2024년 세계 시장 점유율의 28%를 차지했습니다. 이 지역의 소비자 선호도는 점점 더 지속가능한 포장 솔루션에 대한 선호도가 높아지면서 생분해성 및 퇴비화 가능한 포장재 채택을 촉진하고 있습니다. 이는 편리성, 위생, 지속가능성에 대한 소비자의 기대에 부응하고, 견고하고 누출 방지 및 변조 방지 기능을 갖춘 포장에 대한 수요 증가를 반영합니다.

목차

제1장 조사 방법과 조사 범위

제2장 개요

제3장 업계 인사이트

- 산업 에코시스템 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 컨비니언스 푸드에 대한 수요 증가

- 온라인 식품 딜리버리 플랫폼의 성장

- 신흥 국가에서 가처분소득의 증가

- 퀵서비스 레스토랑(QSR)의 확대

- 기업·시설 부문에서 케이터링 서비스의 부상

- 업계의 잠재적 리스크·과제

- 일회용 플라스틱에 관한 환경 문제 및 규제

- 원재료 가격의 변동

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 향후 시장 동향

- GAP 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산·예측 : 재료별, 2021-2034년

- 주요 동향

- 플라스틱

- 폴리프로필렌(PP)

- 폴리에틸렌(PE)

- 폴리에틸렌 테레프탈레이트(PET)

- 폴리스티렌(PS)

- 생분해성 플라스틱

- 기타

- 종이·판지

- 알루미늄

- 기타

제6장 시장 추산·예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 플레이트

- 트레이

- 볼

- 컵

- 클램쉘

- 랩·필름

- 포일

- 기타

제7장 시장 추산·예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 퀵서비스 레스토랑(QSR)

- 풀 서비스 레스토랑(FSR)

- 케이터링 서비스

- 온라인 딜리버리

- 기타

제8장 시장 추산·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

제9장 기업 개요

- Anchor Packaging

- Berry Global

- Billerud

- Contital

- D&W Fine Pack

- Dart Container

- Georgia-Pacific

- Graphic Packaging International

- Huhtamaki

- Oji Fibre Solutions

- Pactiv Evergreen

- Plus Pack

- ProAmpac

- Stora Enso

- Vegware

- WestRock

- WinCup

The Global Food Service Disposable Market was valued at USD 73.2 billion in 2024 and is projected to grow at a CAGR of 5.7% from 2025 to 2034. This growth is primarily driven by the rapid expansion of quick-service restaurants (QSRs) and the surge in online food delivery platforms. Urbanization and changing consumer lifestyles have increased the preference for convenience, prompting QSRs to adopt a wide range of food service disposables to ensure hygiene, operational efficiency, and cost-effectiveness. Manufacturers in this space must focus on producing high-quality, cost-effective, and environmentally sustainable disposable products to cater to the growing demand from QSRs. As the market continues to expand, investments in eco-friendly materials and innovative designs that enhance hygiene and functionality will be pivotal in meeting the evolving requirements of the food service industry.

Simultaneously, the global rise in online food delivery services is fueling the demand for durable and secure disposable packaging. The increasing popularity of digital ordering, app-based food services, and cloud kitchens has pushed packaging providers to develop long-lasting, leak-proof, and tamper-evident packaging solutions that maintain food safety and delivery efficiency. As health consciousness grows among consumers, the focus on food-safe, sustainable, and biodegradable materials is becoming more pronounced. Food service disposable producers must emphasize the development of packaging that not only supports the rapid growth of online food ordering systems but also aligns with consumers' preferences for environmentally friendly options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $73.2 Billion |

| Forecast Value | $127.3 Billion |

| CAGR | 5.7% |

The market is segmented by material into paper and paperboard, plastic, aluminum, and others. The plastic segment is anticipated to generate USD 59.8 billion by 2034. Due to sustainability concerns and increasing regulatory pressures, the plastic segment is witnessing a shift towards the development of recyclable and biodegradable solutions. New innovations in compostable plastics and advanced recycling technologies are gaining traction as businesses strive to balance customer demand for eco-friendly packaging with the need for convenience and durability in the food service sector.

By product type, the market is divided into plates, trays, bowls, cups, clamshells, wraps and films, foils, and others. Plates accounted for 17.7% of the market share in 2024. Demand for plates is rising due to the increasing need for convenient, on-the-go eating solutions, driven by the growth of QSRs, street food vendors, and online food services. Consumers' preference for single-use, hygienic eating solutions is further contributing to segment growth. Moreover, the push for sustainable alternatives has led to the development of compostable and biodegradable plates made from materials such as paper, bamboo, and bagasse.

The market is also segmented by end-use into QSRs, full-service restaurants (FSRs), catering services, online delivery, and others. The QSR segment dominated the market with a 38.1% share in 2024. Global and regional QSR chain expansion, combined with rapid modernization, has spurred the adoption of lightweight, durable, and flexible materials that enhance portability while maintaining food quality during takeout and delivery.

North America accounted for 28% of the global market share in 2024. Consumer preferences in the region are increasingly leaning towards sustainable packaging solutions, driving the adoption of biodegradable and compostable packaging materials. The US food service disposable market alone generated USD 16.6 billion in 2024, reflecting the growing demand for robust, leak-proof, and tamper-evident packaging that meets consumer expectations for convenience, hygiene, and sustainability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for convenience food

- 3.2.1.2 Growth of online food delivery platforms

- 3.2.1.3 Rising disposable income in emerging economies

- 3.2.1.4 Expansion of quick-service restaurants (QSRs)

- 3.2.1.5 Rise of catering services in corporate and institutional sectors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental concerns and regulations on single-use plastics

- 3.2.2.2 Fluctuating raw material prices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 GAP analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Bn & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastic

- 5.2.1 Polypropylene (PP)

- 5.2.2 Polyethylene (PE)

- 5.2.3 Polyethylene terephthalate (PET)

- 5.2.4 Polystyrene (PS)

- 5.2.5 Biodegradable plastic

- 5.2.6 Others

- 5.3 Paper & paperboard

- 5.4 Aluminum

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Bn & Kilo Tons)

- 6.1 Key trends

- 6.2 Plates

- 6.3 Trays

- 6.4 Bowls

- 6.5 Cups

- 6.6 Clamshells

- 6.7 Wraps & films

- 6.8 Foils

- 6.9 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Bn & Kilo Tons)

- 7.1 Key trends

- 7.2 Quick service restaurants (QSRs)

- 7.3 Full-service restaurants (FSRs)

- 7.4 Catering services

- 7.5 Online delivery

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anchor Packaging

- 9.2 Berry Global

- 9.3 Billerud

- 9.4 Contital

- 9.5 D&W Fine Pack

- 9.6 Dart Container

- 9.7 Georgia-Pacific

- 9.8 Graphic Packaging International

- 9.9 Huhtamaki

- 9.10 Oji Fibre Solutions

- 9.11 Pactiv Evergreen

- 9.12 Plus Pack

- 9.13 ProAmpac

- 9.14 Stora Enso

- 9.15 Vegware

- 9.16 WestRock

- 9.17 WinCup