|

시장보고서

상품코드

1708202

폐렴구균 백신 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Pneumococcal Vaccine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

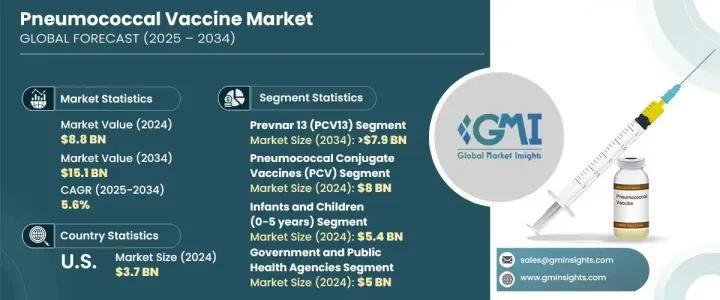

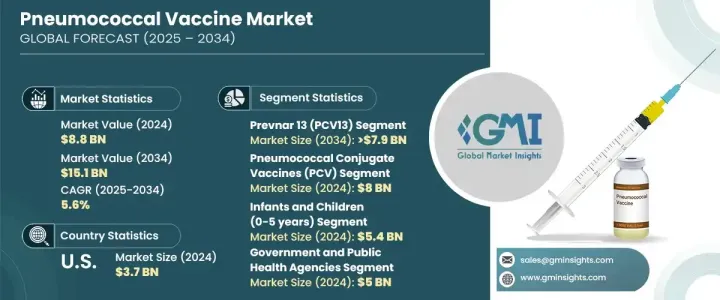

폐렴구균 백신 세계 시장은 2024년 88억 달러로 평가되었고, 2025년부터 2034년까지 연평균 5.6% 성장할 것으로 예측됩니다.

폐렴구균 감염증의 유병률 증가, 백신 접종의 중요성에 대한 대중의 인식 증가, 세계 각국 정부의 적극적인 예방접종 프로그램 추진 등 여러 가지 요인이 이러한 성장에 기여하고 있습니다. 백신 접종률의 급격한 증가는 특히 소아 및 고위험군에 대한 의무적인 백신 접종 스케줄을 시행하려는 의료 당국의 노력이 활발해졌기 때문입니다. 연구 개발의 지속적인 발전으로 보다 효과적이고 혁신적인 폐렴구균 백신이 생산되고 있으며, 보다 다양한 혈청형에 대응할 수 있게 되었습니다. 이러한 백신은 폐렴구균으로 인한 폐렴, 수막염, 패혈증 등 폐렴구균으로 인한 생명을 위협하는 질병의 발생률을 줄이는 데 중요한 역할을 하고 있습니다.

각국 정부가 예방 의료를 우선시하고 폐렴구균 백신을 정기 예방접종 일정에 포함시킴에 따라 시장 수요가 크게 증가할 것으로 예측됩니다. 면역 결핍 환자 및 노인에 대한 예방 접종이 점점 더 중요해지면서 백신 제조업체에 새로운 기회가 창출되고 있습니다. 또한, 제약회사들은 국제보건기구와 긴밀히 협력하여 폐렴구균 감염이 공중보건에 큰 문제가 되고 있는 저소득 지역에서 이러한 백신에 대한 접근성을 확대하기 위해 노력하고 있습니다. 백신 연구에 대한 자금 지원 증가와 새로운 혈청형을 포괄하는 광범위 백신 개발 이니셔티브가 결합하여 향후 10년간 시장 성장을 더욱 촉진할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 88억 달러 |

| 예상 금액 | 151억 달러 |

| CAGR | 5.6% |

폐렴구균 백신은 심각한 세균 감염을 예방하는 데 크게 기여하고 있습니다. 가장 널리 사용되는 백신 중 하나인 폐렴구균 백신은 2034년까지 연평균 5.8%의 성장률을 보이며 79억 달러의 매출을 기록했습니다. 여러 폐렴구균 혈청형에 대한 효능이 입증된 이 백신은 특히 소아 및 고위험군 성인 집단에서 널리 사용되고 있습니다. 이 백신은 장기간에 걸쳐 면역을 획득할 수 있기 때문에 의료 서비스 제공자 및 정부 예방접종 캠페인에서 선호되고 있습니다. 폐렴, 패혈증, 수막염을 포함한 중증 폐렴구균성 질환에 대한 광범위한 적용 범위로 인해 이 백신은 전 세계 예방접종 프로그램에서의 입지를 지속적으로 강화하고 있습니다.

폐렴구균 백신 시장은 크게 결합형 백신과 다당체 백신의 두 가지로 나뉩니다. 결합형 백신은 폐렴구균 감염에 대한 예방 효과가 장기간 지속되어 2024년 80억 달러의 매출을 기록하며 시장을 주도하고 있습니다. 특히 5세 미만 소아에서 폐렴구균성 질환 예방 효과가 높다는 점이 수요 증가에 박차를 가하고 있습니다. 또한, 성인 집단, 특히 면역력이 저하된 사람이나 노년층에 대한 적용 확대가 결합형 백신의 채택을 가속화하고 있습니다. 폐렴구균 백신은 폐렴구균 감염의 전반적인 부담을 줄일 수 있는 능력으로 인해 정기 예방접종 스케줄에서 선호되는 백신으로 자리 잡고 있습니다.

미국 폐렴구균 백신 시장은 2024년 37억 달러 규모 시장을 형성했습니다. 노인은 면역 기능 저하로 인해 폐렴구균 감염에 걸릴 위험이 높기 때문입니다. 예방 의료에 대한 노력과 전국적인 백신 접종 프로그램으로 인해 백신 접종률이 크게 증가하여 고위험군에 대한 예방 효과가 높아지고 있습니다. 제약회사와 정부 기관은 보다 광범위한 폐렴구균 혈청형을 표적으로 하는 새로운 백신을 지속적으로 개발하여 백신 접종률을 지속적으로 높이고 있으며, 이는 장기적인 시장 확대를 더욱 촉진하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 파이프라인 분석

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업 - 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- Pneumosil (PCV10)

- Pneumovax 23 (PPSV23)

- Prevnar 13 (PCV13)

- Prevnar 20 (PCV20)

- Synflorix (PCV10)

- Vaxneuvance (PCV15)

- 기타 제품

제6장 시장 추산 및 예측 : 백신 유형별, 2021년-2034년

- 주요 동향

- 폐렴구균 결합 백신(PCV)

- 폐렴구균 다당체 백신(PPSV)

제7장 시장 추산 및 예측 : 연령층별, 2021년-2034년

- 주요 동향

- 유아 및 소아(0-5세)

- 성인(18-64세)

- 고령자(65세 이상)

제8장 시장 추산 및 예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 병원 약국

- 소매 약국

- 정부 및 공중위생 기관

- E-Commerce

제9장 시장 추산 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 개요

- Beijing Minhai Biological Technology

- Bio-Manguinhos/Fiocruz

- GlaxoSmithKline

- Merck &Co.

- Pfizer

- Serum Institute of India

- Walvax Biotechnology

The Global Pneumococcal Vaccine Market was valued at USD 8.8 billion in 2024 and is projected to grow at a CAGR of 5.6% between 2025 and 2034. Several factors are driving this growth, including the increasing prevalence of pneumococcal infections, rising public awareness about the importance of vaccination, and favorable government initiatives promoting immunization programs worldwide. The surge in vaccination rates can be attributed to growing efforts by healthcare authorities to implement mandatory vaccination schedules, particularly for children and high-risk populations. Ongoing advancements in research and development are leading to the production of more effective and innovative pneumococcal vaccines, catering to a wider range of serotypes. These vaccines play a crucial role in reducing the incidence of life-threatening conditions such as pneumonia, meningitis, and sepsis caused by Streptococcus pneumoniae.

As governments prioritize preventive healthcare and integrate pneumococcal vaccines into routine immunization schedules, market demand is set to rise significantly. The increasing focus on immunizing immunocompromised individuals and elderly populations is creating new opportunities for vaccine manufacturers. Furthermore, pharmaceutical companies are working closely with global health organizations to expand access to these vaccines in low-income regions, where pneumococcal diseases remain a major public health concern. Rising funding for vaccine research, coupled with initiatives to develop broad-spectrum vaccines that cover emerging serotypes, is expected to further boost market growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.8 Billion |

| Forecast Value | $15.1 Billion |

| CAGR | 5.6% |

The market is segmented based on product, with various pneumococcal vaccines contributing significantly to preventing severe bacterial infections. One of the most widely used vaccines is expected to experience notable growth, with a projected CAGR of 5.8%, generating USD 7.9 billion by 2034. Its proven efficacy in protecting against multiple Streptococcus pneumoniae serotypes has led to widespread adoption, especially in pediatric and high-risk adult populations. The vaccine's ability to provide long-term immunity makes it a preferred choice among healthcare providers and government vaccination campaigns. With its broad coverage against severe pneumococcal diseases, including pneumonia, sepsis, and meningitis, this vaccine continues to strengthen its position in global immunization programs.

The pneumococcal vaccine market is divided into two main types: conjugate vaccines and polysaccharide vaccines. Conjugate vaccines dominated the market in 2024, generating USD 8 billion due to their ability to offer long-lasting protection against pneumococcal infections. Their high effectiveness in preventing pneumococcal diseases, especially among children under five years old, has fueled their growing demand. Additionally, expanding applications among adult populations, particularly those with weakened immune systems and elderly individuals, are accelerating the adoption of conjugate vaccines. Their ability to reduce the overall burden of pneumococcal diseases has established them as the preferred choice for routine immunization schedules.

The U.S. pneumococcal vaccine market generated USD 3.7 billion in 2024. The rising elderly population in the country has been a key driver of this growth, as aging individuals face a higher risk of contracting pneumococcal infections due to declining immune function. Preventive healthcare efforts and nationwide vaccination programs have significantly increased vaccine uptake, ensuring better protection for high-risk populations. Pharmaceutical companies and government agencies continue to enhance vaccine coverage, with ongoing efforts to develop newer vaccines that target a broader range of pneumococcal serotypes, further supporting the market's long-term expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of pneumococcal diseases

- 3.2.1.2 Government immunization programs and initiatives

- 3.2.1.3 Growing aging population

- 3.2.1.4 Technological advancements and new product launches

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of vaccines

- 3.2.2.2 Vaccine hesitancy and low awareness

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Pipeline analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pneumosil (PCV10)

- 5.3 Pneumovax 23 (PPSV23)

- 5.4 Prevnar 13 (PCV13)

- 5.5 Prevnar 20 (PCV20)

- 5.6 Synflorix (PCV10)

- 5.7 Vaxneuvance (PCV15)

- 5.8 Other products

Chapter 6 Market Estimates and Forecast, By Vaccine Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pneumococcal conjugate vaccines (PCV)

- 6.3 Pneumococcal polysaccharide vaccines (PPSV)

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Infants and children (0–5 years)

- 7.3 Adults (18–64 years)

- 7.4 Elderly (65+ years)

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Government and public health agencies

- 8.5 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Beijing Minhai Biological Technology

- 10.2 Bio-Manguinhos/Fiocruz

- 10.3 GlaxoSmithKline

- 10.4 Merck & Co.

- 10.5 Pfizer

- 10.6 Serum Institute of India

- 10.7 Walvax Biotechnology