|

시장보고서

상품코드

1708211

플라스틱 팔레트 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Plastic Pallets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

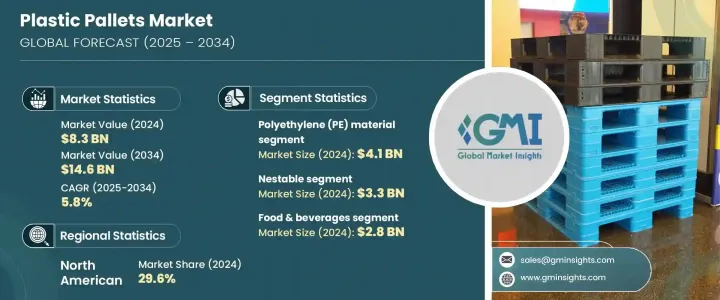

세계 플라스틱 팔레트 시장은 2024년 83억 달러로 평가되며, 2025년부터 2034년까지 연평균 5.8%의 성장률을 보일 것으로 예상됩니다. 효율적이고 지속가능하며 내구성이 뛰어난 포장 솔루션에 대한 수요 증가, 특히 E-Commerce, 소매, 제약, 냉장 창고 등의 분야에서 이러한 성장세를 주도하고 있습니다. 플라스틱 팔레트는 기존 목재 팔레트보다 내구성이 뛰어나고, 오염 위험이 적으며, 위생 기준을 준수하는 등 다양한 장점을 가지고 있습니다. 세계 무역이 확대되고 공급망이 복잡해짐에 따라 물류 효율성을 높이고 비용을 최소화하기 위해 플라스틱 팔레트를 선택하는 산업이 증가하고 있습니다. 탄소발자국을 줄이고 운송 중 제품의 안전을 보장하는 것이 중요해지면서 다양한 산업에서 플라스틱 팔레트의 채택이 더욱 가속화되고 있습니다.

또한, 창고 자동화를 촉진하는 기능을 포함한 플라스틱 팔레트 설계의 혁신으로 인해 플라스틱 팔레트는 현대의 공급망 관리에 필수적인 요소로 자리 잡았습니다. 플라스틱 팔레트와 관련된 장기적인 비용 이점에 대한 인식이 높아지면서 해충 발생 우려로 인해 목재 팔레트 사용을 억제하기 위한 정부 규제와 함께 시장 성장을 더욱 촉진하고 있습니다. 순환 경제 실천과 지속가능한 공급망 솔루션에 대한 전 세계적인 노력은 기업들이 재사용 및 재활용이 가능한 플라스틱 팔레트에 투자하도록 장려하고 있으며, 다양한 산업 분야에서 플라스틱 팔레트의 매력을 높이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 83억 달러 |

| 예상 금액 | 146억 달러 |

| CAGR | 5.8% |

플라스틱 팔레트 시장은 폴리에틸렌(PE), 폴리프로필렌(PP), 기타 재료가 주요 카테고리를 형성하고 있으며, PE 부문은 2024년 41억 달러로 평가되었습니다. 이 소재는 저렴한 가격, 경량 특성, 뛰어난 유연성으로 인해 제조업체들 사이에서 여전히 선호되고 있습니다. 폴리에틸렌 팔레트는 구조적 무결성을 유지하면서 가혹한 취급을 견딜 수 있기 때문에 소매 및 E-Commerce 분야에서 특히 인기가 있습니다. 또한, 충격 흡수 및 내충격성이 제품 안전에 중요한 요소인 음료 및 빠르게 움직이는 소비재(FMCG)의 운송에도 널리 사용되고 있습니다.

플라스틱 팔레트는 유형별로도 분류되며, 시장은 중첩형, 적층형, 랙형, 기타 유형으로 나뉩니다. 중첩형 플라스틱 팔레트 분야는 공간 절약적이고 비용 효율적인 물류 솔루션에 대한 수요 증가로 인해 2024년 33억 달러 규모의 시장을 창출했습니다. 중첩형 팔레트는 창고 공간을 줄이고 반송 비용을 최소화하는 실용적인 솔루션으로 대량 배송이 필요한 산업에 적합합니다. 운영 효율성과 탄소 배출량 감소를 우선시하는 기업들은 저장 공간을 최적화하고 전체 운송 비용을 절감할 수 있는 중첩형 팔레트에 점점 더 많은 관심을 기울이고 있습니다.

북미는 2024년 플라스틱 팔레트 시장에서 29.6%의 점유율을 차지했는데, 이는 공급망 간소화, 창고 자동화, 지속가능한 대체 포장에 대한 관심이 높아진 것을 반영합니다. 해충 방제 및 위생 문제로 인해 목재 팔레트 사용에 대한 정부 규제가 강화됨에 따라 이 지역에서는 플라스틱 팔레트로의 전환이 더욱 가속화되고 있습니다. 이러한 팔레트는 업계 요구 사항과 규제 표준을 모두 충족하고 내구성이 뛰어나며 오래 지속되고 비용 효율적인 솔루션을 제공합니다. 산업계가 자동화를 채택하고 공급망 최적화에 지속적으로 투자하고 있는 가운데, 플라스틱 팔레트는 다양한 분야에서 효율성과 지속가능성을 강화하는 데 있어 매우 중요한 역할을 할 준비가 되어 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 산업 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- E-Commerce와 소매 업계 성장

- 식품 및 음료 업계의 도입 증가

- 세계 무역과 공급망 최적화 증가

- 플라스틱 재활용 기술의 진보

- 냉장·화학 산업 확대

- 업계의 잠재적 리스크·과제

- 한정된 수리 가능성

- 플라스틱 폐기물에 대한 환경 문제

- 성장 촉진요인

- 성장의 가능성 분석

- 규제 상황

- 기술 동향

- 향후 시장 동향

- 격차 분석

- Porters 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 시장 점유율 분석

- 주요 시장 기업 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정과 예측 : 재료별, 2021-2034년

- 주요 동향

- 폴리에틸렌(PE)

- 고밀도 폴리에틸렌(HDPE)

- LDPE

- 폴리프로필렌(PP)

- 기타

제6장 시장 추정과 예측 : 유형별, 2021-2034년

- 주요 동향

- 네스터블

- 랙커블

- 스태커블

- 기타

제7장 시장 추정과 예측 : 최종 이용 산업별, 2021-2034년

- 주요 동향

- 식품 및 음료

- 화학제품

- 의약품

- 자동차

- 기타

제8장 시장 추정과 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

제9장 기업 개요

- Bekuplast

- Benoplast

- Cabka

- CHEP

- Craemer

- Loscam International

- Millwood

- Monoflo International

- Naeco Packaging

- Nilkamal Material Handling

- ORBIS Corporation

- Polymer Solutions International

- Premier Handling Solutions

- Rehrig Pacific

- Schoeller Allibert

- Smart-Flow

- TMF Corporation

- Werit Kunststoffwerke

The Global Plastic Pallets Market was valued at USD 8.3 billion in 2024 and is projected to grow at a CAGR of 5.8% between 2025 and 2034. The rising demand for efficient, sustainable, and durable packaging solutions is driving this growth, particularly in sectors such as e-commerce, retail, pharmaceuticals, and cold storage. Plastic pallets offer superior advantages over traditional wooden pallets, including better durability, reduced risk of contamination, and compliance with hygiene standards. As global trade continues to expand and supply chains become more complex, industries are increasingly opting for plastic pallets to enhance logistical efficiency and minimize costs. The growing emphasis on reducing carbon footprints and ensuring product safety during transit has further accelerated the adoption of plastic pallets in various industries.

Additionally, innovations in plastic pallet design, including features that facilitate automation in warehouses, are making these pallets an essential part of modern supply chain management. Rising awareness about the long-term cost benefits associated with plastic pallets, along with government regulations aimed at curbing the use of wooden pallets due to concerns about pest infestations, is further boosting market growth. The global push toward circular economy practices and sustainable supply chain solutions is encouraging companies to invest in reusable and recyclable plastic pallets, enhancing their appeal across diverse industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 5.8% |

The plastic pallets market is segmented based on material, with polyethylene (PE), polypropylene (PP), and other materials forming the key categories. The PE segment was valued at USD 4.1 billion in 2024. This material remains a preferred choice among manufacturers due to its affordability, lightweight properties, and remarkable flexibility. Polyethylene pallets are particularly popular in the retail and e-commerce sectors due to their ability to withstand rigorous handling while maintaining their structural integrity. They are also widely used in the transportation of beverages and fast-moving consumer goods (FMCG), where shock absorption and impact resistance are critical factors for product safety.

Plastic pallets are also categorized by type, with the market divided into nestable, stackable, rackable, and other types. The nestable plastic pallet segment generated USD 3.3 billion in 2024, driven by the increasing demand for space-saving and cost-effective logistics solutions. Nestable pallets offer a practical solution for reducing warehouse space requirements and minimizing return shipping costs, making them ideal for industries with high-volume shipping needs. Businesses that prioritize operational efficiency and lower carbon emissions are increasingly turning to nestable pallets for their ability to optimize storage space and reduce overall transportation costs.

North America held a 29.6% share of the plastic pallets market in 2024, reflecting a growing preference for streamlined supply chains, automation in warehouses, and a focus on sustainable packaging alternatives. Stricter government regulations concerning the use of wooden pallets, driven by pest control and hygiene concerns, have further accelerated the shift towards plastic pallets in this region. These pallets offer a more durable, long-lasting, and cost-effective solution that meets both industry requirements and regulatory standards. As industries continue to adopt automation and invest in supply chain optimization, plastic pallets are poised to play a pivotal role in enhancing efficiency and sustainability across various sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce & retail industry

- 3.2.1.2 Rising adoption in the food & beverage industry

- 3.2.1.3 Rise in global trade & supply chain optimization

- 3.2.1.4 Advancements in plastic recycling technology

- 3.2.1.5 Expansion of cold storage & chemical industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited repairability

- 3.2.2.2 Environmental concerns over plastic waste

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.2.1 HDPE

- 5.2.2 LDPE

- 5.3 Polypropylene (PP)

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Nestable

- 6.3 Rackable

- 6.4 Stackable

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Chemicals

- 7.4 Pharmaceuticals

- 7.5 Automotive

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bekuplast

- 9.2 Benoplast

- 9.3 Cabka

- 9.4 CHEP

- 9.5 Craemer

- 9.6 Loscam International

- 9.7 Millwood

- 9.8 Monoflo International

- 9.9 Naeco Packaging

- 9.10 Nilkamal Material Handling

- 9.11 ORBIS Corporation

- 9.12 Polymer Solutions International

- 9.13 Premier Handling Solutions

- 9.14 Rehrig Pacific

- 9.15 Schoeller Allibert

- 9.16 Smart-Flow

- 9.17 TMF Corporation

- 9.18 Werit Kunststoffwerke