|

시장보고서

상품코드

1716511

재사용 발사체 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Reusable Launch Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

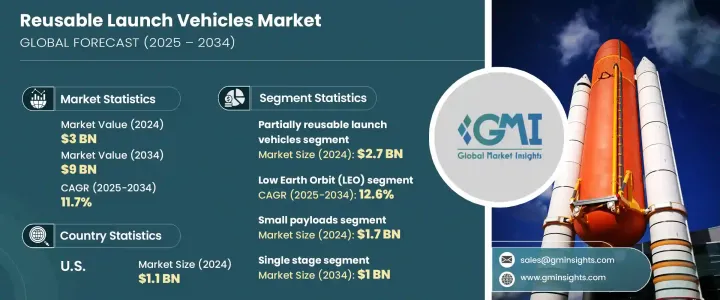

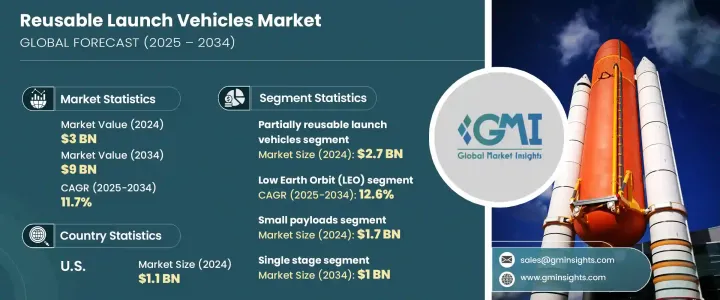

세계 재사용 발사체 시장은 2024년 30억 달러 규모에 달했으며, 2025년부터 2034년까지 연평균 11.7%의 성장률을 보일 것으로 전망됩니다.

재사용 발사체(RLV)은 기존의 일회용 로켓에 비해 경제적인 대안을 제공하기 때문에 비용 효율적이고 신뢰할 수 있는 우주 접근에 대한 수요가 증가함에 따라 재사용 발사체(RLV)의 성장에 박차를 가하고 있습니다. 통신, 지구관측, 항법, 방위 등의 용도로 위성 발사 빈도가 증가함에 따라 재사용 가능한 솔루션의 필요성이 대두되고 있습니다. 이러한 로켓은 동일한 하드웨어로 여러 번의 발사를 가능하게 함으로써 우주 탐사 비용을 크게 절감하고, 우주 탐사 및 위성 배치를 보다 지속 가능하고 상업적으로 실행 가능한 것으로 만들어 줍니다.

우주여행에 대한 관심 증가와 민간 주도의 항공우주산업 증가도 시장 성장에 기여하고 있습니다. 우주 기관과 민간 기업 모두 페이로드 용량 향상, 소요 시간 단축, 운영 효율성 향상을 위해 차세대 RLV 개발에 많은 투자를 하고 있습니다. 또한, 재료, 추진 시스템, AI를 활용한 발사 기술의 발전은 재사용 가능한 부품의 수명 연장에 기여하고 있으며, 이는 이러한 차량의 채택을 더욱 촉진하고 있습니다. 세계 시장에서는 과학 연구, 국방 및 상업용 용도를 위한 지속적인 발사를 지원하는 견고한 우주 인프라를 구축하기 위한 정부 및 민간 투자가 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 30억 달러 |

| 예상 금액 | 90억 달러 |

| CAGR | 11.7% |

재사용 발사체 시장은 로켓 유형과 궤도 범위에 따라 구분됩니다. 로켓 유형에는 부분 재사용 발사체과 완전 재사용 발사체이 있습니다. 완전 재사용 발사체은 2034년까지 12억 달러 시장 규모가 예상됩니다. 이 분야는 아직 개발 초기 단계에 있으며, 현재 진행 중인 연구개발은 소요 시간 단축과 운영 비용 최소화에 초점을 맞추었습니다. 우주 탐사, 위성 메가 컨스텔레이션, 행성 간 임무에 대한 관심이 높아지는 가운데, 완전 재사용 발사체은 발사 비용 절감, 배치 주기 단축 등 장기적으로 큰 이점을 제공할 준비가 되어 있습니다. 열 차폐, 착륙 시스템, 신속한 개보수 프로세스 개선을 위한 투자 증가는 미래 임무를 위한 완전 재사용 시스템의 실현 가능성을 가속화하고 있습니다.

시장은 또한 정지궤도(GEO), 저궤도(LEO), 중궤도(MEO), 지구궤도(BEO) 등 궤도 유형별로 분류되며, MEO 부문은 2024년 8.9% 시장 점유율을 차지할 것으로 예상되며, 이는 주로 안전한 군용 통신에 대한 수요 증가와 이러한 궤도에 대형의 긴 수명을 가진 위성을 효율적으로 배치할 수 있는 재사용 가능한 로켓의 능력에 기인합니다. 재사용 가능한 로켓이 이러한 궤도에 대형, 장수명 위성을 효율적으로 배치할 수 있는 능력에 의해 주도될 것입니다. 군사 및 상업적 용도가 계속 확대됨에 따라 재사용 발사체을 통한 MEO에 대한 접근성을 향상시키는 발전은 시장의 성장을 가속할 것으로 예측됩니다.

미국의 재사용 발사체 시장 규모는 2024년 11억 달러에 달했으며, 이는 미국의 탄탄한 우주 산업과 재사용 발사체 기술을 전문으로 하는 대형 제조업체의 존재에 힘입은 것으로 분석됩니다. 미국 내 우주 발사 활동 증가는 비용 효율성과 신뢰성 향상에 대한 강조와 함께 시장 성장을 가속하고 있습니다. 우주 개발 분야의 지속적인 기술 혁신과 정부 및 민간 부문의 지속적인 투자로 미국은 앞으로도 재사용 발사체 개발 및 채택에 있어 세계 리더로 남을 것으로 예측됩니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크와 과제

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 서브시스템 분석

- 유도, 항행 및 제어 시스템

- 추진 시스템

- 텔레메트리, 트래킹 및 커멘드 시스템

- 전력 시스템

- 기타

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산·예측 : 비클 유형별, 2021년-2034년

- 주요 동향

- 부분 재사용 발사체

- 완전 재사용 발사체

제6장 시장 추산·예측 : 궤도 유형별, 2021년-2034년

- 주요 동향

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

- Beyond Earth Orbit (BEO)

제7장 시장 추산·예측 : 페이로드 용량별, 2021년-2034년

- 주요 동향

- 소형 페이로드(2,000kg 이하)

- 중형 페이로드(2,000kg-10,000kg)

- 중량 페이로드(10,000kg 이상)

제8장 시장 추산·예측 : 구성별, 2021년-2034년

- 주요 동향

- 싱글 스테이지

- 멀티 스테이지

제9장 시장 추산·예측 : 용도별, 2021년-2034년

- 주요 동향

- 위성 발사

- 우주 탐사

- 우주 관광

- 화물 운송

- 기타

제10장 시장 추산·예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 정부

- 상업

제11장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

제12장 기업 개요

- Arianespace

- Blue Origin

- Boeing

- China Aerospace Science and Technology Corporation(CASC)

- Lockheed Martin

- Mitsubishi Heavy Industries

- Northrop Grumman

- Relativity Space

- Rocket Lab

- Roscosmos

- Sierra Nevada Corporation

- SpaceX

- Virgin Galactic

The Global Reusable Launch Vehicles Market generated USD 3 billion in 2024 and is projected to grow at a CAGR of 11.7% between 2025 and 2034. The rising demand for cost-effective and reliable space access is fueling this growth, as reusable launch vehicles (RLVs) offer a more economical alternative to traditional expendable rockets. With the increasing frequency of satellite launches for applications such as communication, Earth observation, navigation, and defense, the need for reusable solutions is becoming more pronounced. These vehicles significantly reduce the cost of space missions by enabling multiple launches with the same hardware, making space exploration and satellite deployment more sustainable and commercially viable.

The growing interest in space tourism and the increasing number of private-sector initiatives in the aerospace industry are also contributing to market growth. Space agencies and private companies alike are investing heavily in developing next-generation RLVs to improve payload capacities, reduce turnaround times, and enhance operational efficiencies. Moreover, advancements in materials, propulsion systems, and AI-driven launch technologies are helping extend the lifespan of reusable components, further driving the adoption of these vehicles. The global market is witnessing increased government and private investments aimed at establishing a robust space infrastructure that supports continuous launches for scientific research, defense, and commercial applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $9 Billion |

| CAGR | 11.7% |

The market for reusable launch vehicles is segmented by vehicle type and orbital range. Vehicle types include partially reusable and fully reusable launch vehicles. Fully reusable launch vehicles are expected to generate USD 1.2 billion by 2034. This segment is still in the early stages of development, with ongoing research and development focused on enhancing turnaround times and minimizing operational costs. As interest in space exploration, satellite mega-constellations, and interplanetary missions grows, fully reusable launch vehicles are poised to offer substantial long-term benefits, including reduced launch costs and faster deployment cycles. Increasing investments in improving thermal shielding, landing systems, and rapid refurbishment processes are accelerating the viability of fully reusable systems for future missions.

The market is also classified by orbit type, including Geostationary Orbit (GEO), Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Beyond Earth Orbit (BEO). The MEO segment held an 8.9% market share in 2024, primarily driven by the increasing demand for secure military communications and the ability of reusable launch vehicles to efficiently deploy large, long-life satellites into these orbits. As military and commercial applications continue to expand, advancements in making MEO more accessible to reusable launch vehicles are expected to stimulate further market growth.

The U.S. reusable launch vehicles market was valued at USD 1.1 billion in 2024, driven by the country's well-established space industry and the presence of leading manufacturers specializing in reusable launch technologies. The growing number of space launch activities in the U.S., coupled with a focus on improving cost-efficiency and reliability, is propelling market growth. With continuous innovation in space exploration and sustained government and private sector investments, the U.S. is expected to remain a global leader in reusable launch vehicle development and adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for satellites orbiting the Earth

- 3.2.1.2 Increasing government and military investments

- 3.2.1.3 Technological advancements in reusability

- 3.2.1.4 Rise of space tourism and suborbital flights

- 3.2.1.5 Increase in space-based manufacturing and research

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial development costs

- 3.2.2.2 Limited reusability cycles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Subsystem analysis

- 3.10.1 Guidance, navigation & control systems

- 3.10.2 Propulsion systems

- 3.10.3 Telemetry, tracking & command systems

- 3.10.4 Electrical power systems

- 3.10.5 Others

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Vehicle Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Partially reusable launch vehicles

- 5.3 Fully reusable launch vehicles

Chapter 6 Market Estimates and Forecast, By Orbit Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Low Earth Orbit (LEO)

- 6.3 Medium Earth Orbit (MEO)

- 6.4 Geostationary Orbit (GEO)

- 6.5 Beyond Earth Orbit (BEO)

Chapter 7 Market Estimates and Forecast, By Payload Capacity, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Small payloads (up to 2,000 kg)

- 7.3 Medium payloads (2,000 kg to 10,000 kg)

- 7.4 Heavy payloads (above 10,000 kg)

Chapter 8 Market Estimates and Forecast, By Configuration, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Single stage

- 8.3 Multi-stage

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Satellite launch

- 9.3 Space exploration

- 9.4 Space tourism

- 9.5 Cargo transport

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Government

- 10.3 Commercial

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Arianespace

- 12.2 Blue Origin

- 12.3 Boeing

- 12.4 China Aerospace Science and Technology Corporation (CASC)

- 12.5 Lockheed Martin

- 12.6 Mitsubishi Heavy Industries

- 12.7 Northrop Grumman

- 12.8 Relativity Space

- 12.9 Rocket Lab

- 12.10 Roscosmos

- 12.11 Sierra Nevada Corporation

- 12.12 SpaceX

- 12.13 Virgin Galactic