|

시장보고서

상품코드

1716700

바이오 농약 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Biopesticides Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

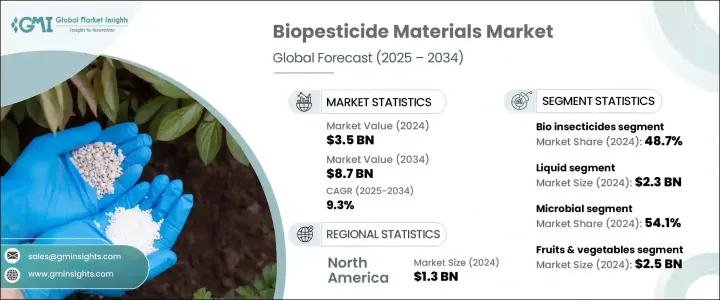

세계의 바이오 농약 시장은 2024년에 35억 달러에 이르렀고, 유기농산물에 대한 수요 증가와 세계 소비자의 건강지향 증가에 힘입어 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 9.3%로 강력한 성장을 이룰 것으로 전망되고 있습니다.

합성농약의 악영향에 대한 우려가 계속 높아지는 가운데, 바이오 농약은 보다 안전하고 지속 가능한 농작물 보호의 대체 수단으로서 급속히 대두하고 있습니다. 오늘의 소비자는 관행 재배의 과일이나 야채에 잔류 농약이 포함되어 있는 것을 보다 강하게 인식하고 있어 유기농법의 도입을 크게 추진하고 있습니다.

바이오 농약은 박테리아, 균류, 바이러스, 식물 유래 물질 등 천연 유래의 것이기 때문에 종합적 해충 관리 프로그램이나 지속 가능한 농업에 점점 선호되고 있습니다. 세계 각국의 정부도 유기농업의 대처에 유리한 정책과 보조금 지원을 통해 바이오 농약의 사용을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 35억 달러 |

| 예측 금액 | 87억 달러 |

| CAGR | 9.3% |

바이오 농약 시장은 바이오 살충제, 바이오 제초제, 바이오 살균제 및 기타 제품으로 구분되며, 바이오 농약은 2024년에 48.7%의 최대 시장 점유율을 차지했습니다. 2034년까지 연평균 9.2%의 성장률로 성장할 것으로 예상됩니다. 천연 미생물 또는 식물 기반 활성 화합물로 구성된 바이오 농약은 특히 농가가 화학 살충제에 대한 의존을 줄이려고 하기 때문에 현대 농업에 필수적인 요소가 되어 바이오 농약의 채용이 확대되고 있는 배경에는 종합적 해충관리(IPM) 시스템에 있어서의 바이오 농약의 역할과 유기농법기준의 적합성이 있으며, 관행농법과 유기농법의 양쪽 모두의 생산자에게 지지되고 있습니다.

제품 형태에 따라 시장은 건조제와 액체제로 나뉘며, 액체바이오 농약은 2024년에 23억 달러를 창출했고 2034년까지 연평균 복합 성장률(CAGR) 9.4%로 성장할 것으로 예측됩니다. 액체 제제는 사용하기 쉬운 용도, 높은 효능, 뛰어난 보존 안정성에 의해 인기를 끌고 있습니다. 현탁 농축액, 유화성 농축액, 가용성 액체로서 입수 가능한 이러한 제제는 식물 표면에의 보다 좋은 부착을 보증해, 기존의 살포 장치를 사용해 간단하게 살포할 수 있어 효율적인 해충 방제를 원하는 농부들 사이에서 널리 사용되고 있습니다.

지역별로 북미는 2024년에 13억 달러의 바이오 농약 매출을 올렸으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 9%로 성장할 전망입니다. 이 지역은 미국과 캐나다의 농업 바이오테크놀러지에 대한 많은 투자를 배경으로 세계 시장에서 주도적 지위를 유지하고 있습니다. 북미에서의 바이오 농약 수요를 뒷받침하고 있으며, 첨단 농업기술과 종합적인 해충관리의 실천이 광범위하게 실시되고 있는 것도, 이 급증하는 시장에 있어서의 이 지역의 아성을 보다 견고한 것으로 하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 유기농 제품에 대한 소비자의 기호

- 규제 당국의 지원과 정부의 대처

- 기술의 진보

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용

- 화학농약에 비해 작용이 느린

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 규모와 예측 : 제품별, 2021년-2034년

- 주요 동향

- 바이오 제초제

- 바이오 살충제

- 바이오 살균제

제6장 시장 규모와 예측 : 형태별, 2021년-2034년

- 주요 동향

- 건식

- 액체

제7장 시장 규모와 예측 : 원료별, 2021년-2034년

- 주요 동향

- 미생물

- 생화학

- 기타

제8장 시장 규모와 예측 : 작물별, 2021년-2034년

- 주요 동향

- 곡물 및 유량씨

- 과일 및 야채

- 사과

- 포도

- 감자

- 기타

- 기타

제9장 시장 규모와 예측 : 용도별, 2021년-2034년

- 주요 동향

- 종자 처리

- 잎면 살포

- 토양 스프레이

제10장 시장 추계·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제11장 기업 프로파일

- BASF SE

- Bayer AG

- Syngenta AG

- UPL Limited

- FMC Corporation

- Marrone Bio Innovations

- Novonesis

- Nufarm

- Isagro SpA

- Certis USA LLC

- Koppert Biological Systems

- Biobest Group NV

- Valent BioSciences

- STK Bio-Ag Technologies

The Global Biopesticides Market reached USD 3.5 billion in 2024 and is projected to witness robust growth at a CAGR of 9.3% from 2025 to 2034, fueled by the growing demand for organic produce and increasing health consciousness among consumers worldwide. As concerns over the adverse effects of synthetic pesticides continue to rise, biopesticides are rapidly emerging as a safer and more sustainable alternative for crop protection. Consumers today are more aware of pesticide residues found in conventionally grown fruits and vegetables, which is significantly pushing the adoption of organic farming practices.

Since biopesticides are derived from natural sources such as bacteria, fungi, viruses, and plant-based substances, they are increasingly preferred for integrated pest management programs and sustainable agriculture. Moreover, the global focus on eco-friendly agricultural practices, coupled with stricter regulations against chemical pesticide usage, is accelerating the shift toward biopesticides. Governments worldwide are also promoting biopesticide use through favorable policies and subsidy support for organic farming initiatives. Additionally, the rising prevalence of pest resistance to synthetic pesticides is compelling farmers to explore more effective and environmentally responsible solutions, adding further momentum to the biopesticides market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 9.3% |

The biopesticides market is segmented into bio insecticides, bio herbicides, bio fungicides, and other products, with bio insecticides accounting for the largest market share of 48.7% in 2024. This segment is projected to expand at a CAGR of 9.2% through 2034, driven by the rising need for pest control solutions that minimize environmental harm while maintaining high crop yields. Bio insecticides, composed of natural microorganisms or plant-based active compounds, have become essential components in modern agriculture, especially as farmers seek to reduce dependency on chemical insecticides. Their growing adoption is supported by their role in integrated pest management (IPM) systems and their compatibility with organic farming standards, making them a favored choice for both conventional and organic growers.

Based on product form, the market is divided into dry and liquid formulations, with liquid biopesticides generating USD 2.3 billion in 2024 and anticipated to grow at a CAGR of 9.4% through 2034. Liquid formulations are gaining traction due to their user-friendly application, higher efficacy, and superior shelf stability. Available as suspension concentrates, emulsifiable concentrates, and soluble liquids, these formulations ensure better adherence to plant surfaces and are easily applied using existing spraying equipment, driving widespread usage among farmers seeking efficient pest control.

Regionally, North America generated USD 1.3 billion in biopesticides sales in 2024 and is poised to grow at a CAGR of 9% between 2025 and 2034. The region maintains a leading position in the global market, backed by significant investments in agricultural biotechnology across the United States and Canada. The ongoing shift toward sustainable farming methods and organic agriculture continues to bolster the demand for biopesticides in North America. Furthermore, the widespread implementation of advanced farming techniques and integrated pest management practices reinforces the region's stronghold in this rapidly expanding market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Consumer preference for organic products

- 3.6.1.2 Regulatory support and government initiatives

- 3.6.1.3 Technological advancements

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High Production Costs

- 3.6.2.2 Slow action compared to chemical pesticides

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Bio herbicides

- 5.3 Bio insecticides

- 5.4 Bio fungicides

Chapter 6 Market Size and Forecast, By Form, 2021 – 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Dry

- 6.3 Liquid

Chapter 7 Market Size and Forecast, By Source, 2021 – 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Microbial

- 7.3 Biochemical

- 7.4 Others

Chapter 8 Market Size and Forecast, By Crop, 2021 – 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Grain & oil seeds

- 8.3 Fruit & vegetables

- 8.3.1 Apples

- 8.3.2 Grapes

- 8.3.3 Potatoes

- 8.3.4 Others

- 8.4 Others

Chapter 9 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Seed treatment

- 9.3 Foliar spray

- 9.4 Soil spray

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 BASF SE

- 11.2 Bayer AG

- 11.3 Syngenta AG

- 11.4 UPL Limited

- 11.5 FMC Corporation

- 11.6 Marrone Bio Innovations

- 11.7 Novonesis

- 11.8 Nufarm

- 11.9 Isagro S.p.A

- 11.10 Certis USA L.L.C.

- 11.11 Koppert Biological Systems

- 11.12 Biobest Group NV

- 11.13 Valent BioSciences

- 11.14 STK Bio-Ag Technologies