|

시장보고서

상품코드

1740792

무선 심장 모니터링 시스템 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Wireless Cardiac Monitoring Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

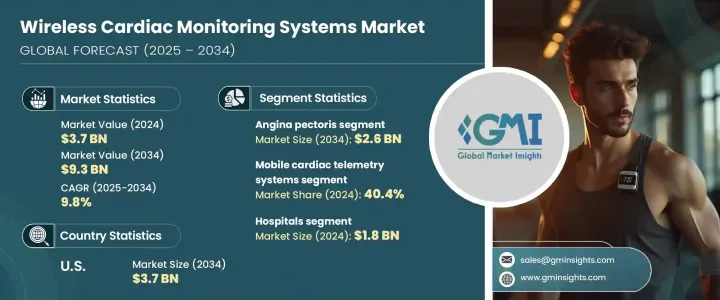

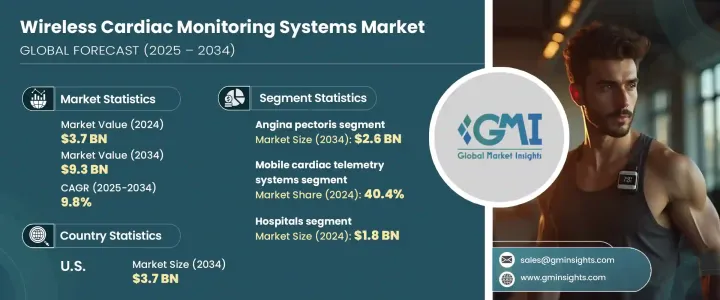

세계의 무선 심장 모니터링 시스템 시장 규모는 2024년 37억 달러로, 실시간 원격 심장 관리에 대한 수요 증가와 세계 심혈관 질환의 유병률 증가로 CAGR 9.8%로 성장해 2034년까지 93억 달러에 이를 것으로 예측됩니다.

무선 심장 모니터링 시스템은 건강 전문가가 심장 건강을 모니터링하는 방법을 변화시키고 지속적인 추적과 무선 데이터 전송을 가능하게합니다. 신속하고 정확한 임상 대응을 가능하게 하는 인사이트를 제공함으로써 중요한 역할을 수행하고 있습니다.

기술 혁신은 여전히 이 시장의 기세를 지원하는 중요한 촉매입니다. 새로운 세대의 장치는 현재 실시간 ECG 전송, AI 대응 분석, 클라우드 플랫폼과의 통합과 같은 고급 기능을 제공하여 임상가에게 심장 데이터를보다 효과적으로 해석하고 신속하게 행동하는 힘 이 도구는 진단의 정확성을 크게 향상, 특히 외래 및 원격 지역에서 환자의 치료 성과를 향상시킬 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 37억 달러 |

| 예측 금액 | 93억 달러 |

| CAGR | 9.8% |

시장 세분화는 이식 가능한 심장 모니터(ICM), 모바일 심장 텔레메트리(MCT) 시스템 및 기타 무선 심장 모니터 제품으로 분류됩니다. 2024년의 수익 점유율은 모바일 심장 텔레메트리 시스템이 40.4%를 차지했습니다. 이 기능은 비정상적인 심장 활동의 즉각적인 감지 및보고를 보장하며 전통적인 단기 모니터링은 간과되는 일시적인 부정맥 진단에 적극적인 접근법을 제공합니다. 비용 효율적인 모니터링 솔루션에 대한 선호도가 높아짐에 따라 더욱 뒷받침됩니다. 이러한 장점은 장기 요양이 필요한 환자와 재입원 및 입원 비용 절감에 중점을 둔 건강 관리 시스템에 특히 중요합니다.

무선 심장 모니터링 시스템은 협심증과 같은 병리학의 관리에서도 중요한 역할을 합니다. 실시간 모니터링은 증상 패턴과 유인의 평가를 용이하게 하고, 보다 개별화된 시기 적절한 개입을 가능하게 합니다. 증상이 예측 불가능하게 발생하거나, 비전형적으로 나타나는 경우, 지속적인 모니터링은 정적 검사법으로는 놓칠 가능성이 있는 중요한 인사이트를 제공해, 리스크 관리와 예방 의료 전략을 지원합니다.

최종 용도의 관점에서 시장은 병원, 전문 클리닉, 진단센터, 재택 케어 환경, 기타로 구분됩니다. 또한 AI 주도의 데이터 관리를 지원하는 기술에 대한 투자도 이러한 시설에서는 점점 널리 사용되고 있으며, 실시간 분석과 신속한 의료 판단을 가능하게 하고 있습니다. 또한 병원은 웨어러블 심전도 센서나 임베디드 디바이스 등의 최첨단 시스템을 적극적으로 채용해, 질 높은 케어의 제공과 업무의 효율화를 도모하고 있습니다.

미국의 무선 심장 모니터링 시스템 시장은 견고한 건강 관리 인프라와 심혈관 질환의 이환율 상승을 배경으로 2034년까지 37억 달러를 초과할 것으로 예측됩니다. 국내 기업과 연구 개발도 차세대 모니터링 솔루션 개발에 있어 매우 중요한 역할을 하고 있으며, 시장을 더욱 전진시키고 있습니다.

이 업계는 여전히 경쟁이 치열하며 Medtronic, Abbott Laboratories, Boston Scientific, iRhythm Technologies, Koninklijke Philips NV와 같은 주요 기업들이 세계 시장 점유율의 약 40%를 차지하고 있으며, 이러한 기업들은 이 급속도로 진화하는 시장에서 우위를 차지하기 위해 원격 모니터링, AI 지원 진단 및 원활한 데이터 전송 기술에서 획기적인 노력을 계속하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심혈관질환(CVD)의 유병률 증가

- 무선 심장 모니터링 기술의 기술적 진보

- 예방 건강 관리의 중요성 증가

- 업계의 잠재적 위험 및 과제

- 농촌나 미개발 지역에서는 입수가 한정된다

- 엄격한 규제 요건

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 국가별 대응

- 업계에 미치는 영향

- 공급측의 영향(제조 비용)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(소비자의 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(제조 비용)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 기술적 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 이식형 심장 모니터(ICM)

- 모바일 심장 텔레메트리 시스템

- 납 베이스

- 패치 베이스

- 기타 제품

제6장 시장 추계 및 예측 : 적응증별, 2021-2034년

- 주요 동향

- 관상동맥질환

- 협심증

- 동맥경화증

- 심부전

- 뇌졸중

- 기타 적응증

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 전문 클리닉

- 진단센터

- 재택 케어 환경

- 기타 용도

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott Laboratories

- AliveCor

- Baxter International

- Biotronik

- Boston Scientific

- InfoBionic

- iRhythm Technologies

- Koninklijke Philips NV

- Medtronic

- Nihon Kohden

- SmartCardia

- Vital Connect

The Global Wireless Cardiac Monitoring Systems Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 9.8% to reach USD 9.3 billion by 2034, driven by the rising demand for real-time, remote cardiac care and the increasing prevalence of cardiovascular diseases worldwide. Wireless cardiac monitoring systems are transforming how healthcare professionals monitor heart health, allowing continuous tracking and wireless data transmission. These systems play a critical role in the early identification of heart-related conditions such as atrial fibrillation, heart failure, and arrhythmias by providing near real-time insights that enable faster and more precise clinical responses. As demand for continuous monitoring rises in aging populations and patients with chronic conditions, the appeal of wireless cardiac monitoring becomes more pronounced.

Technological innovation remains a key catalyst behind this market's momentum. New-generation devices now offer advanced features such as real-time ECG transmission, AI-enabled analytics, and integration with cloud platforms, empowering clinicians to interpret cardiac data more effectively and act promptly. These tools significantly enhance the accuracy of diagnosis and improve patient care outcomes, especially in outpatient or remote settings. The increasing shift toward decentralized care and home-based monitoring further fuels this market expansion, making these systems an essential component of modern cardiac care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 9.8% |

In terms of product segmentation, the market is categorized into implantable cardiac monitors (ICMs), mobile cardiac telemetry (MCT) systems, and other wireless cardiac monitoring products. As of 2023, the global market was valued at USD 3.4 billion, with mobile cardiac telemetry systems accounting for 40.4% of the revenue share in 2024. MCT devices enable real-time, continuous monitoring of cardiac rhythms and autonomously transmit alerts using Bluetooth or cellular connectivity. This functionality ensures immediate detection and reporting of abnormal heart activity, offering a proactive approach to diagnosing transient arrhythmias that traditional short-term monitoring may overlook. The consistent growth of this segment is further supported by broader adoption in outpatient settings and an increasing preference for portable, cost-efficient monitoring solutions. These benefits are particularly significant for patients requiring long-term care and for healthcare systems focused on reducing hospital readmissions and in-patient costs.

Wireless cardiac monitoring systems also play a vital role in managing conditions like angina pectoris, which often require ongoing observation to identify ischemic events or irregularities that can precede serious cardiac episodes. Real-time monitoring facilitates better evaluation of symptom patterns and triggers, allowing for more personalized and timely interventions. When symptoms occur unpredictably or present atypically, continuous monitoring provides critical insights that static testing methods might miss, thereby supporting risk management and preventive care strategies.

From an end-use perspective, the market is segmented into hospitals, specialty clinics, diagnostic centers, homecare settings, and others. In 2024, the hospital segment alone reached USD 1.8 billion. Hospitals equipped with advanced cardiology departments and specialized staff are leading adopters of wireless cardiac technologies, using them to improve diagnostic precision and optimize patient care pathways. Investments in technologies that support cloud integration and AI-driven data management have also become increasingly common in these facilities, enabling real-time analysis and faster medical decisions. Additionally, hospitals are actively adopting cutting-edge systems, including wearable ECG sensors and implantable devices, to deliver high-quality care and streamline operations.

The United States wireless cardiac monitoring systems market is projected to surpass USD 3.7 billion by 2034, driven by robust healthcare infrastructure and rising incidence of cardiovascular disease. The country benefits from the rapid adoption of medical innovations and consistent support from both regulatory bodies and investors. Domestic companies and research institutes are also playing a pivotal role in developing next-generation monitoring solutions, further advancing the market. The rise in heart-related health concerns and demand for advanced diagnostic tools are pushing adoption rates higher across clinical and home settings.

This industry remains highly competitive, with key players like Medtronic, Abbott Laboratories, Boston Scientific, iRhythm Technologies, and Koninklijke Philips N.V. collectively accounting for around 40% of the global market share. These companies continue to focus on breakthroughs in remote monitoring, AI-assisted diagnostics, and seamless data transmission technologies to stay ahead in this fast-evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased prevalence of cardiovascular diseases (CVDs)

- 3.2.1.2 Technological advancements in wireless cardiac monitoring technologies

- 3.2.1.3 Rising emphasis on preventive healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability in rural and underdeveloped areas

- 3.2.2.2 Stringent regulatory requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Implantable cardiac monitors (ICM)

- 5.3 Mobile cardiac telemetry systems

- 5.3.1 Lead-based

- 5.3.2 Patch-based

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Coronary artery disease

- 6.3 Angina pectoris

- 6.4 Atherosclerosis

- 6.5 Heart failure

- 6.6 Stroke

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Specialty clinics

- 7.4 Diagnostic centers

- 7.5 Home care settings

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AliveCor

- 9.3 Baxter International

- 9.4 Biotronik

- 9.5 Boston Scientific

- 9.6 InfoBionic

- 9.7 iRhythm Technologies

- 9.8 Koninklijke Philips N.V.

- 9.9 Medtronic

- 9.10 Nihon Kohden

- 9.11 SmartCardia

- 9.12 Vital Connect