|

시장보고서

상품코드

1740813

유기 건조 주정박 사료 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Organic Dried Distiller´s Grain Feed Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

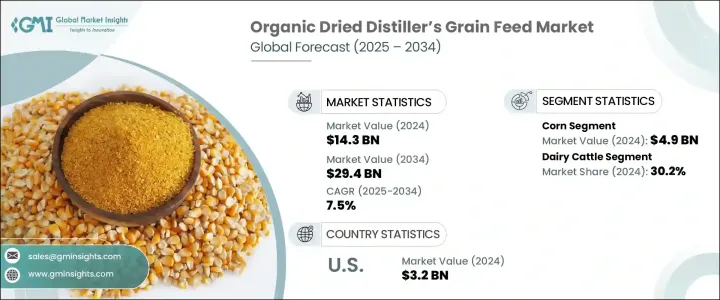

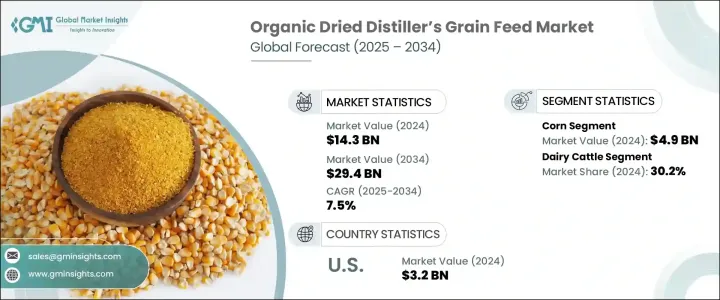

세계의 유기 건조 주정박 사료 시장은 2024년 143억 달러로 평가되어, 유기농 축산물에 대한 수요 증가와 지속 가능하고 환경에 배려한 농업 관행에 대하 업계 전체의 뒷받침으로, CAGR 7.5%로 성장하여 2034년에는 294억 달러에 달할 것으로 추정됩니다.

소비자의 선호도가 더 깨끗하고 윤리적인 식품으로 빠르게 이동하는 동안 축산 부문은 유기적이고 재생 가능한 사료 시스템과의 협조를 강력히 요구하고 있습니다. 그리고 점점 대두되고 있습니다. 또한 세계 무역의 혼란은 탄력 있고 추적 가능한 공급망의 중요성을 높이고 있으며, 유기 DDG를 기존 사료를 대체하는 실행 가능한 옵션으로 더욱 자리 매김하고 있습니다. 동물복지와 지속가능성을 둘러싼 인식이 깊어짐에 따라, 생산자는 규제의 기대와 소비자의 신뢰를 모두 충족하기 때문에 유기 사료 투입을 급속히 채용하고 있습니다. 양 프로그램에서 중요한 원료가 되고 있으며, 성능의 신뢰성과 유기 인증과의 무결성을 모두 제공합니다.

지난 몇 년간 에탄올 생산자가 유기 곡물 투입으로 이동하여 생산 시설의 인증을 요구하게 되었기 때문에 유기 인증 DDG 공급량이 크게 증가하고 있습니다. 생산자와 사료 제조업체는 지속가능성 목표와 시장 수요 양쪽에 합치하는 유기 솔루션의 채용에 과거 없을 정도로 열심히 노력하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 143억 달러 |

| 예측 금액 | 294억 달러 |

| CAGR | 7.5% |

옥수수를 주원료로 하는 건조 주정박은 2024년에 49억 달러의 수익을 올렸으며 2034년까지 연평균 복합 성장률(CAGR) 7%를 보일 것으로 예측되며 여전히 지배적인 원료입니다. 옥수수는 널리 입수 가능하며 전분 함량이 높고 에탄올 발효 효율이 높기 때문에 유기 DDG 생산에 적합한 작물입니다. 이 일관성은 엄격한 유기 인증 기준을 충족하기 위해 고품질 사료 투입에 의존하는 생산자에게 필수적입니다.

동물에 대한 응용 분야에서 젖소는 가장 큰 소비자 부문입니다. 7.8%를 보일 것으로 예측되는 이 부문은 유기 DDG가 낙농의 식이요구를 지원하는데 중요한 역할을 하고 있음을 반영하고 있습니다. 이는 우유 생산량을 유지하는 데 도움이 될 뿐만 아니라, 소 전체의 건강과 활력을 서포트합니다.

미국의 유기 건조 디스티러스 그레인 사료 시장은 2024년 32억 달러를 창출해 CAGR 7.3%를 보일 것으로 예측됩니다. 이 성장의 원동력이되는 것은 재생 농업에 대한 관심 증가와 지속 가능하고 투명성이 높은 축산물을 선호하는 소비자의 동향입니다. 유기 에탄올 생산의 제품별을 재이용하는 순환형 농업에 있어서의 유기 DDG의 역할을 생각하면, 생산성과 지속가능성의 양쪽 모두를 높이고 싶은 미국의 생산자에게 있어서, 유기 DDG는 매력적인 선택지가 되고 있습니다.

Flint Hills Resources, Archer Daniels Midland Company(ADM), Green Plains Inc., POET LLC, Valero Energy Corporation과 같은 주요 기업은 확장 및 인증 취득에 적극적으로 투자하고 있습니다. 전략적 파트너십과 추적성과 투명성의 중요성 증가는 진화하는 유기 사료의 전망에서 장기적인 성장을 목표로하는 이러한 기업 시장 전략을 계속 정의하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 미래의 전망

- 제조업자

- 리셀러

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 공급측의 영향(원재료)

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국, 2021-2024년

- 주요 수입국, 2021-2024년

- 공급자의 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 유기농 동물 제품에 대한 소비자 수요 증가

- 유기 축산 및 양계 확대

- 정부의 지원과 유기인증 정책

- 지속가능하고 순환적인 농업 관행의 중시

- 업계의 잠재적 위험 및 과제

- 인증된 유기 원료의 입수가 한정

- 기존의 사료에 비해 높은 생산 및 가공 비용

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 원료별, 2021-2034년

- 주요 동향

- 옥수수

- 밀

- 쌀

- 보리

- 수수

- 귀리

- 호밀

- 기장

- 기타

제6장 시장 추계 및 예측 : 동물 유형별, 2021-2034년

- 주요 동향

- 젖소

- 육우

- 돼지

- 가금

- 아쿠아

- 기타 동물의 유형

제7장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 동물사료

- 바이오에너지 생산

- 비료 및 토양 개량제

- 기타

제8장 시장 추계 및 예측 : 유통 채널별, 2021-2034년

- 주요 동향

- 온라인

- 오프라인

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Bayer Animal Health

- ADM

- Agrifeeds

- Alcogroup SA

- Chimique India

- COFCO Biochemical(Anhui) Co. Ltd.

- Feedpedia

- Furst-McNess Company

- Greenfield Global Inc.

- Gulshan Polyols Ltd.

- Kemin Industries, Inc.

- Midas Overseas

- Nutrigo Feeds Pvt Ltd

- Poet LLC

- Valero Energy Corporation

The Global Organic Dried Distiller's Grain Feed Market was valued at USD 14.3 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 29.4 billion by 2034, driven by the rising demand for organic livestock products and an industry-wide push toward sustainable, eco-conscious farming practices. With consumer preferences rapidly shifting toward cleaner, ethically sourced food, the livestock sector is under mounting pressure to align with organic and regenerative feed systems. Organic DDGs are increasingly emerging as a key solution, bridging the gap between nutritional needs and organic compliance. Global trade disruptions have also heightened the importance of resilient, traceable supply chains-further positioning organic DDGs as a viable alternative to conventional feed. As organic certification standards tighten and awareness surrounding animal welfare and sustainability deepens, producers are rapidly adopting organic feed inputs to meet both regulatory expectations and consumer trust. Across the livestock industry, from poultry to dairy and beef cattle, organic DDGs are now a crucial ingredient in nutrition programs, offering both performance reliability and alignment with organic certifications. This growth trajectory is supported by continued investments, evolving regulatory frameworks, and infrastructure developments across established and emerging markets.

Over the past few years, the supply of certified organic DDGs has grown considerably, as ethanol producers shift toward organic grain inputs and seek certification for their production facilities. These developments come at a time when the demand for sustainable and transparent agricultural supply chains is reaching new heights. Producers and feed manufacturers are more eager than ever to embrace organic solutions that align with both sustainability goals and market demand. North America continues to lead in market adoption due to its well-established organic agriculture ecosystem. However, the Asia-Pacific region is quickly catching up, as countries invest in organic production models and enhance their certification and distribution infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.3 Billion |

| Forecast Value | $29.4 Billion |

| CAGR | 7.5% |

Corn-based dried distiller's grain remains the dominant feedstock, generating USD 4.9 billion in revenue in 2024 and projected to grow at a 7% CAGR through 2034. Corn's widespread availability, high starch content, and efficiency in ethanol fermentation make it a preferred crop for organic DDG production. The nutritional density of corn-derived DDGs, rich in protein and energy, also makes it especially well-suited for organic livestock systems. This consistency is vital for producers who rely on quality feed inputs to meet stringent organic certification standards. As livestock producers continue to prioritize nutrition and compliance, corn-based DDG is expected to retain its leadership in the organic feed segment.

In terms of animal application, dairy cattle represent the largest consumer segment. Valued at USD 4.3 billion in 2024 and forecasted to grow at a CAGR of 7.8%, this segment reflects the critical role that organic DDG plays in supporting the dietary needs of dairy operations. Organic dairy farms, which restrict the use of synthetic additives and antibiotics, increasingly rely on organic DDGs to deliver protein and fiber naturally. This not only helps maintain milk production levels but also supports overall herd health and vitality. As demand for organic dairy products grows globally, the importance of nutrient-rich, organically compliant feed will only become more central to the sector.

The United States Organic Dried Distiller's Grain Feed Market generated USD 3.2 billion in 2024 and is expected to grow at a 7.3% CAGR. This growth is fueled by increased interest in regenerative agriculture and consumer trends favoring sustainable, transparently sourced animal products. US feed manufacturers are adapting swiftly by integrating organic DDGs into nutrition plans that support both performance and environmental goals. Given their role in circular agriculture-repurposing by-products of organic ethanol production-organic DDGs are becoming an attractive choice for American producers looking to boost both productivity and sustainability.

Leading companies such as Flint Hills Resources, Archer Daniels Midland Company (ADM), Green Plains Inc., POET LLC, and Valero Energy Corporation are actively investing in expansion and certification. These key players are upgrading facilities to meet organic standards, collaborating with organic grain suppliers, and tailoring their product lines to cater to specific livestock nutrition requirements. Strategic partnerships and a growing emphasis on traceability and transparency continue to define the market strategies of these firms as they position themselves for long-term growth in the evolving organic feed landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-Side Impact (Raw Materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-Side Impact (Raw Materials)

- 3.2.3 Demand-Side Impact (Selling Price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing consumer demand for organic animal products

- 3.8.1.2 Expansion of organic livestock and poultry farming

- 3.8.1.3 Government support and organic certification policies

- 3.8.1.4 Emphasis on sustainable and circular agricultural practices

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Limited availability of certified organic raw materials

- 3.8.2.2 High production and processing costs compared to conventional feed

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Corn

- 5.3 Wheat

- 5.4 Rice

- 5.5 Barley

- 5.6 Sorghum

- 5.7 Oats

- 5.8 Rye

- 5.9 Millet

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Animal Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dairy cattle

- 6.3 Beef cattle

- 6.4 Swine

- 6.5 Poultry

- 6.6 Aqua

- 6.7 Other animal types

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Animal feed

- 7.3 Bioenergy production

- 7.4 Fertilizers & Soil amendments

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Online

- 8.3 Offline

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bayer Animal Health

- 10.2 ADM

- 10.3 Agrifeeds

- 10.4 Alcogroup SA

- 10.5 Chimique India

- 10.6 COFCO Biochemical (Anhui) Co. Ltd.

- 10.7 Feedpedia

- 10.8 Furst-McNess Company

- 10.9 Greenfield Global Inc.

- 10.10 Gulshan Polyols Ltd.

- 10.11 Kemin Industries, Inc.

- 10.12 Midas Overseas

- 10.13 Nutrigo Feeds Pvt Ltd

- 10.14 Poet LLC

- 10.15 Valero Energy Corporation