|

시장보고서

상품코드

1740909

복합 골판지 튜브 포장 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Composite Cardboard Tube Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

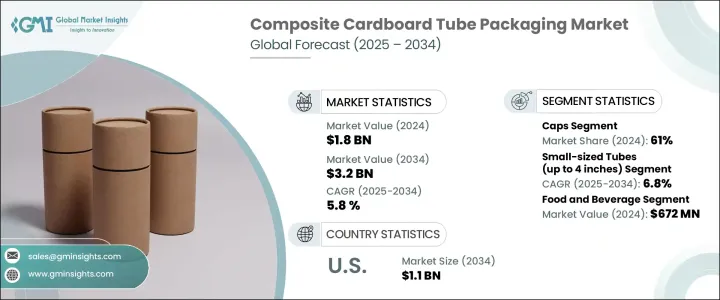

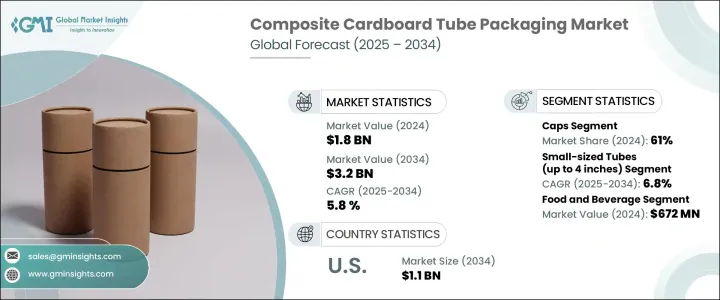

세계의 복합 골판지 튜브 포장 시장은 2024년 18억 달러로 평가되었으며, 친환경 포장에 대한 수요 증가와 전자상거래 활성화로 CAGR 5.8%을 나타내 2034년에는 32억 달러에 이를 것으로 추정됩니다.

각 업계의 기업은 지속 가능한 솔루션으로의 의식적인 변화를 진행하고 있으며, 복합 골판지 튜브는 내구성, 재활용성, 제품의 프레젠테이션을 향상시키는 매력적인 비주얼 어필 등 모든 조건을 충족하기 때문에 강한 지지를 모으고 있습니다. 브랜드는 기능성뿐 아니라 차별화를 위해 튜브 포장에 눈을 돌리고 있습니다. 위의 순환형 경제모델과의 제휴에 주력해 시장은 보다 큰 혁신을 눈에 띄게 될 것으로 예측됩니다. 부는 선반 진열에서 어필을 높이는 동시에 환경에 좋은 영향을 남기고 싶은 브랜드에 있어서 실용적이고 세련된 솔루션이 됩니다.

그러나 시장은 여전히 무시할 수 없는 장애물에 직면하고 있습니다. 비용 증가를 흡수하거나 소비자를위한 가격을 인상하거나 높은 수입 관세를 피하기 위해 지역 공급업체로 발을 옮기는 등 이러한 전환으로 공급망 최적화, 국산 또는 대체 원재료의 조달 목적을 찾고 공급업체와의 파트너십 재평가에 주목이 증가하고 있습니다. 민첩한 재고 시스템에 대한 투자를 늘리고 조달 방법을 다양화하고 있습니다. 재료 조달, 자동화 및 비즈니스 효율성의 혁신은 불안정한 시장 상황에서 경쟁을 이기고 금리를 유지하는 중요한 차별화 요인으로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 18억 달러 |

| 예측 금액 | 32억 달러 |

| CAGR | 5.8% |

제품 유형별로는 캡 부문이 2024년 세계의 복합 골판지 튜브 포장 시장을 61%의 압도적 점유율로 견인했습니다. 또, 경량 캡은 비용 효율적인 운송을 서포트해, 재료의 사용량을 최소한으로 억제하는 것으로 지속가능성의 목표에도 합치하고 있습니다. 또한 브랜드는 이 형식을 활용하고 촉감이 좋은 마무리, 엠보싱 로고, QR 코드, 스마트 라벨링 기술을 통해 고객 경험을 향상시키고 있습니다.

최대 4인치의 소형 튜브는 가장 급성장하는 부문으로 견인력을 늘리고 있으며, 2034년까지의 CAGR은 6.8%를 나타낼 것으로 예측되고 있습니다. 이 튜브는 운반에 편리하고 사용하기 쉽고, 내구성과 브랜드 체험을 높이는 고급 스러움도 갖추고 있습니다.

미국의 복합 골판지 튜브 포장 시장은 지속가능한 포장에 대한 의식의 고조와 견고한 전자상거래 생태계에 의해 2034년까지 11억 달러에 이를 것으로 예상되고 있습니다. 이 새로운 디자인은 브랜드가 무게와 부피를 최적화하여 운송 배출을 줄이고 보다 우수한 구조 설계로 제품의 안전성을 높이는 데 도움이 되고 있습니다.

Sonoco, Smurfit Kappa Group, Paper Tubes &Sales, Visican Ltd, Marshall Paper Tube Co. Inc.와 같은 대기업은 시장에서 발자국을 강화하는 전략을 적극적으로 펼치고 있습니다. 리사이클율을 높이는 것 등이 그 예입니다. 또, 브랜드와 최종 사용자의 쌍방에 공감해 받을 수 있는 디자인, 지속가능성, 성능을 융합시킨 단일의 포장 솔루션을 제공하는 혁신에도 힘을 쏟고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속 가능하고 재활용 가능한 포장 솔루션에 대한 소비자의 선호도 증가

- 전자상거래 보급률의 상승에 의한 보호 수송 튜브 수요 증가

- 독자적인 브랜드 차별화를 요구하는 프리미엄 브랜드의 맞춤형 요구의 고조

- 화장품, 의약품, 특수 식품 분야에서의 용도 확대

- 지속 가능한 포장에 대한 주목의 고조

- 업계의 잠재적 위험 및 과제

- 원재료 가격의 변동에 의한 제조 마진에 대한 영향

- 대체 포장 솔루션과의 경쟁

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 클로저 유형별(2021-2034년)

- 주요 동향

- 캡

- 뚜껑

제6장 시장 추계·예측 : 사이즈별(2021-2034년)

- 주요 동향

- 소형 튜브(최대 4인치)

- 중형 튜브(4-10인치)

- 대형 튜브(10인치 이상)

제7장 시장 추계·예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 식품 및 음료

- 의약품

- 화장품 및 퍼스널케어

- 화학

- 기타

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 호주

- 한국

- 일본

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제9장 기업 프로파일

- Ace Paper Tube Corp

- CBT Packaging

- Chicago Mailing Tube Co.

- Darpac P/L

- Hansen Packaging

- Heartland Products Group

- Marshall Paper Tube Co. Inc.

- Paper Tubes &Sales

- Smurfit Kappa Group

- Sonoco

- Valk Industries

- Visican Ltd

The Global Composite Cardboard Tube Packaging Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 3.2 billion by 2034, driven by the growing demand for eco-friendly packaging and the rise in e-commerce activity. Businesses across industries are making conscious shifts toward sustainable solutions, and composite cardboard tubes are gaining strong traction as they check off all the right boxes-durability, recyclability, and an attractive visual appeal that enhances product presentation. From beauty and personal care to food and industrial goods, brands are turning to tube packaging not just for function but for differentiation. The market's evolution is also being fueled by changing consumer behaviors that favor minimal waste, reusable packaging, and a better unboxing experience. As demand for environmentally responsible solutions climbs, the market is expected to witness greater innovation, with manufacturers focusing on customizing designs, improving material strength, and aligning with circular economy models. The growth of D2C (direct-to-consumer) retail, rising subscription box services, and the widespread popularity of gifting products in cylindrical packaging formats are collectively shaping the momentum. Composite cardboard tubes serve as a practical and stylish solution for brands looking to leave a positive environmental impact while boosting shelf appeal. As companies double down on ESG commitments and sustainability metrics, this packaging format is fast becoming a preferred option across global supply chains.

That said, the market still faces hurdles that can't be ignored. Tariffs on imported raw materials and components, originally introduced under earlier U.S. trade policies, have led to a noticeable spike in production costs. Manufacturers are at a crossroads-either absorb the added costs, increase prices for consumers, or pivot to local suppliers to avoid high import duties. This shift has intensified the focus on optimizing supply chains, finding domestic or alternative raw material sources, and reevaluating supplier partnerships. On top of that, ongoing disruptions in international trade and logistics continue to test the resilience of inventory strategies. Companies are increasingly investing in agile inventory systems and diversifying sourcing methods to ensure stability. Innovation in material sourcing, automation, and operational efficiency has emerged as a critical differentiator in staying ahead of the competition and maintaining margins in a volatile market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 5.8% |

In terms of product type, the caps segment led the global composite cardboard tube packaging market with a dominant 61% share in 2024. Their popularity is largely due to secure closure features that ensure product safety during shipping while maintaining ease of use for consumers. Lightweight caps also support cost-effective transportation and align well with sustainability goals by minimizing material usage. Additionally, brands are leveraging this format to enhance customer experience through tactile finishes, embossed logos, QR codes, and smart labeling technologies. The ability to blend functional security with high-end design elements gives caps an edge across multiple verticals-particularly in food, cosmetics, and personal care-where both protection and branding are equally critical.

Small-sized tubes measuring up to 4 inches are gaining traction as the fastest-growing segment, projected to expand at a CAGR of 6.8% through 2034. What is fueling this demand is the consumer shift toward compact, travel-friendly packaging options, especially in skincare, beauty, and on-the-go food products. These tubes are not only portable and user-friendly but also provide durability and a premium touch that elevates brand experience. As consumers seek packaging that combines minimalism with eco-conscious appeal, small tubes are delivering on both fronts-functionality and form.

The United States Composite Cardboard Tube Packaging Market is expected to reach USD 1.1 billion by 2034, driven by heightened awareness of sustainable packaging and a robust e-commerce ecosystem. Domestic manufacturers are stepping up by investing in recyclable, biodegradable tube innovations that meet regulatory benchmarks while enhancing shelf visibility. These new designs are helping brands cut down on transportation emissions by optimizing weight and volume and are boosting product safety with better structural design. As regulations around plastic usage become more stringent, businesses are gravitating toward cardboard tubes as a reliable, compliant, and brand-friendly solution.

Leading players such as Sonoco, Smurfit Kappa Group, Paper Tubes & Sales, Visican Ltd, and Marshall Paper Tube Co., Inc. are actively deploying strategies to strengthen their footprint in the market. These include embracing automated production lines to ramp up output and cut labor costs, partnering for secure raw material access, expanding product customization to serve niche markets, and integrating higher percentages of recycled content. To stay relevant and ahead, they are banking heavily on innovation-blending design, sustainability, and performance into a single packaging solution that resonates with both brands and end users.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analyisis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.4 Supply-side impact (raw materials)

- 3.2.1.4.1.1 Price volatility in key materials

- 3.2.1.4.1.2 Supply chain restructuring

- 3.2.1.4.1.3 Production cost implications

- 3.2.1.5 Demand-side impact (selling price)

- 3.2.1.5.1.1 Price transmission to end markets

- 3.2.1.5.1.2 Market share dynamics

- 3.2.1.5.1.3 Consumer response patterns

- 3.2.1.6 Key companies impacted

- 3.2.1.7 Strategic industry responses

- 3.2.1.7.1.1 Supply chain reconfiguration

- 3.2.1.7.1.2 Pricing and product strategies

- 3.2.1.7.1.3 Policy engagement

- 3.2.1.8 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growing consumer preference for sustainable and recyclable packaging solutions

- 3.3.1.2 Rising e-commerce penetration driving demand for protective shipping tubes

- 3.3.1.3 Increasing customization needs for premium brands seeking unique brand differentiation

- 3.3.1.4 Expanding applications in cosmetics, pharmaceuticals and specialty food sectors

- 3.3.1.5 Increasing focus on sustainable packaging

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Volatility in raw material prices impacting manufacturing margins

- 3.3.2.2 Competition from alternative packaging solutions

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Closure Type, 2021 - 2034 ($ Mn & Units)

- 5.1 Key trends

- 5.2 Caps

- 5.3 Lids

Chapter 6 Market Estimates and Forecast, By Size, 2021 - 2034 ($ Mn & Units)

- 6.1 Key trends

- 6.2 Small-sized tubes (up to 4 inches)

- 6.3 Medium-sized tubes (4 to 10 inches)

- 6.4 Large-sized tubes (over 10 inches)

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 ($ Mn & Units)

- 7.1 Key trends

- 7.2 Food and Beverage

- 7.3 Pharmaceuticals

- 7.4 Cosmetics and Personal Care

- 7.5 Chemicals

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Australia

- 8.4.4 South Korea

- 8.4.5 Japan

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 U.A.E.

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Ace Paper Tube Corp

- 9.2 CBT Packaging

- 9.3 Chicago Mailing Tube Co.

- 9.4 Darpac P/L

- 9.5 Hansen Packaging

- 9.6 Heartland Products Group

- 9.7 Marshall Paper Tube Co., Inc.

- 9.8 Paper Tubes & Sales

- 9.9 Smurfit Kappa Group

- 9.10 Sonoco

- 9.11 Valk Industries

- 9.12 Visican Ltd