|

시장보고서

상품코드

1740920

생가죽 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Raw Hides and Skins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

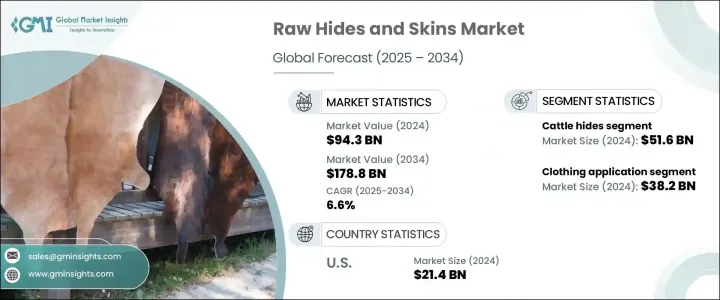

세계의 생가죽 시장 규모는 2024년에 943억 달러로 평가되었고, CAGR 6.6%를 나타내 2034년에는 1,788억 달러에 이를 것으로 추정되고 있습니다.

이는 의류, 가정용 가구, 고급 액세서리 등 다양한 산업에서 가죽을 사용한 상품 수요가 높아지고 있는 것에 기인하고 있습니다. 따라서 생가죽 시장은 이러한 변화의 혜택을 받고 있습니다. 고급 가죽 제품의 매력은 특히 패션과 인테리어 용도에서 미적 감각, 장수명, 쾌적성이 구매 행동에 중요한 역할을 하는 소비 패턴의 상승으로 이어지고 있습니다. 시장은 원료의 안정 공급에 크게 의존하는 가죽 산업의 세계 확대에 깊이 영향을 받고 있습니다. 2023년 세계의 생가죽 생산량은 약 2,100만 톤으로, 그 대부분은 소에서 유래했습니다.

생가죽 시장에서는 소피가 수량·수익의 양면에서 우위를 유지하고 있습니다. 2024년 소가죽 부문은 516억 달러로 평가되었으며 예측 기간 동안 6.5%의 연평균 성장률(CAGR)을 나타낼 것으로 예상됩니다. 이 가죽은 뛰어난 강도, 두께, 전반적인 품질에 의해 선호되며 신발, 가구의 장지, 고급 패션 아이템 등의 견고한 가죽 제품의 제조에 이상적입니다. 그 결과, 이 분야는 시장 내에서 가장 경제적 영향력이 있는 카테고리로서의 지위를 유지하고 있습니다. 대조적으로, 다른 유형의 가죽은 일부 지역 시장에서 인기가 높아지고 있는 것, 소피의 생산 레벨이나 세계 수요에는 아직 미치지 않습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 943억 달러 |

| 예측 금액 | 1,788억 달러 |

| CAGR | 6.6% |

용도별로 의류 분야가 시장 역학 형성에 중요한 역할을 하고 있습니다. 2024년 382억 달러의 가치를 지닌 이 부문은 2034년까지 7%의 연평균 성장률을 나타내 40.7%의 상당한 시장 점유율을 차지할 것으로 예상됩니다. 더 많은 가죽을 도입함에 따라 의류 섹터의 생가죽 수요는 증가세를 유지할 것으로 예측됩니다. 고품질의 가죽 사용과 같은 지속 가능한 패션 선택으로의 전환도 볼 수 있습니다. 이러한 소비자 행동의 변화는 특히 신흥 경제 국가와 부유 한 도시 지역에서 가죽 의류 분야의 성장을 지원합니다.

미국만으로도 2024년 시장 규모는 214억 달러였고 2025년부터 2034년에 걸쳐 CAGR 6.4%를 나타낼 것으로 예측되고 있습니다. 자동차 내장, 가구, 패션 등 여러 산업에 있어서 수요는 계속 견조하고, 고성능으로 지속 가능한 재료에 대한 주목이 높아지고 있습니다.

업계 각사는 제품 품질의 향상, 가격 전략의 합리화, 명확한 가치 제안의 개발로 적극적으로 경쟁하고 있습니다. 한 이니셔티브 외에도 공급망 최적화와 전략적 파트너십은 기업이 세계적인 도달범위를 넓히고 시장 수요에 보다 효율적으로 대응하는 데 도움이 되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴적 혁신

- 향후 전망

- 제조업자

- 리셀러

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 공급측의 영향(원재료)

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국(2021-2024년)

- 주요 수입국(2021-2024년)

- 공급자의 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 패션 업계 및 자동차 업계의 가죽 제품 수요 증가

- 특히 신흥 경제국의 세계 신발 시장 성장

- 럭셔리하고 지속 가능한 가죽 제품에 대한 수요 증가

- 자동차 산업 확대와 가죽 가구의 필요성

- 업계의 잠재적 위험 및 과제

- 가죽 생산과 핥기 공정에 관한 환경 문제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정·예측 : 제품별(2021-2034년)

- 주요 동향

- 소가죽

- 풀 그레인 가죽

- 톱 그레인 가죽

- 정품 가죽

- 스플릿 가죽

- 버팔로 가죽

- 풀 그레인 가죽

- 톱 그레인 가죽

- 스플릿 가죽

- 말 가죽

- 말 가죽(크롬 태닝)

- 말 가죽(야채 태닝)

- 말 가죽 스웨이드

- 기타

제6장 시장 추정·예측 : 유형별(2021-2034년)

- 주요 동향

- 천연

- 합성

제7장 시장 추정·예측 : 기술별(2021-2034년)

- 주요 동향

- 기계

- 수동

제8장 시장 추정·예측 : 용도별(2021-2034년)

- 주요 동향

- 의류

- 신발

- 실내 장식품

- 기타

제9장 시장 추정·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- AJHollander Enterprises Inc.

- Allanasons Pvt Ltd

- AI Bravo Leather Industries

- BAHIRDAR Tannery

- Merpiel

- Norilia Nordic AS

- Naugra

- Rose International

- Sanimax Corporation

- Stan India

- Texpac Hide &Skin Ltd.

- J &E Sedgwick &Co. Ltd.

The Global Raw Hides and Skins Market was valued at USD 94.3 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 178.8 billion by 2034, attributed to the rising demand for leather-based goods across multiple industries, including apparel, home furnishings, and luxury accessories. As consumer preferences continue to lean toward premium, durable materials, the market for raw hides and skins is benefitting from this shift. The appeal of high-end leather products has led to a rise in consumption patterns, particularly in fashion and interior applications, where aesthetics, longevity, and comfort play significant roles in purchasing behavior. The market is deeply influenced by the global expansion of the leather industry, which relies heavily on a consistent supply of raw materials. A notable factor driving growth is the steady output of hides worldwide. In 2023, the global production of raw hides was approximately 21 million metric tons, with a major portion derived from cattle. This trend is closely linked to regions that have a strong presence in livestock farming, providing a stable foundation for market expansion.

Cattle hides continue to dominate the raw hides and skins market in terms of both volume and revenue. In 2024, the cattle hides segment was valued at USD 51.6 billion and is anticipated to expand at a CAGR of 6.5% over the forecast period. These hides are favored due to their superior strength, thickness, and overall quality, making them ideal for manufacturing robust leather goods such as footwear, furniture upholstery, and luxury fashion items. Their availability remains consistent due to large-scale cattle farming operations in regions with well-established livestock industries. As a result, the segment retains its position as the most economically influential category within the market. In contrast, other types of hides, though increasingly popular in certain local markets, have yet to match the production levels or global demand for cattle hides. Nonetheless, they present a potential growth area as niche consumer bases emerge.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $94.3 billion |

| Forecast Value | $178.8 billion |

| CAGR | 6.6% |

In terms of application, the clothing segment plays a vital role in shaping market dynamics. Valued at USD 38.2 billion in 2024, this segment is set to grow at a CAGR of 7% through 2034, claiming a substantial market share of 40.7%. The growing popularity of leather garments-including jackets, skirts, pants, and accessories-reflects changing fashion trends and rising disposable income among middle and upper-income consumers. Leather continues to be seen as a stylish, long-lasting material that fits into modern and luxury fashion aesthetics. As global fashion brands integrate more leather into their collections, demand for raw hides in the clothing sector is expected to maintain upward momentum. There is also a shift toward sustainable fashion choices, which include eco-conscious processing and the use of high-quality leather that supports long-term use rather than disposable consumption. This change in consumer behavior supports growth in the leather clothing segment, particularly in developing economies and affluent urban centers.

The market in the United States alone was valued at USD 21.4 billion in 2024 and is expected to grow at a CAGR of 6.4% between 2025 and 2034. The country continues to be a key player in global leather production, largely due to its access to premium-quality hides and advanced processing infrastructure. Demand across multiple industries-such as automotive interiors, furniture, and fashion-remains strong, with an increasing focus on high-performance and sustainable materials. Innovations in tanning and treatment technologies have also contributed to product quality and consistency, enhancing the competitiveness of the U.S. market.

Companies operating in the industry are actively competing by improving product quality, streamlining pricing strategies, and developing distinct value propositions. Environmental concerns are prompting businesses to adopt responsible sourcing practices and cleaner production methods, which are becoming central to maintaining brand reputation and meeting regulatory expectations. In addition to these efforts, supply chain optimization and strategic partnerships are helping firms broaden their global reach and respond more efficiently to market demands. This evolving landscape highlights the need for constant innovation and cost efficiency to remain relevant in an increasingly competitive environment.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (hs code)

- 3.3.1 Major exporting countries, 2021-2024 (kilo tons)

- 3.3.2 Major importing countries, 2021-2024 (kilo tons)

Note: the above trade statistics will be provided for key countries only.

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing demand for leather products in fashion and automotive industries.

- 3.8.1.2 Growth of the global footwear market, particularly in emerging economies.

- 3.8.1.3 Rising demand for premium and sustainable leather products.

- 3.8.1.4 Expansion of the automotive industry and the need for leather upholstery.

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Environmental concerns regarding leather production and tanning processes.

- 3.8.2.2 Fluctuating raw hide supply due to animal farming and climate-related factors.

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cattle hides

- 5.2.1 Full grain leather

- 5.2.2 Top grain leather

- 5.2.3 Genuine leather

- 5.2.4 Split leather

- 5.3 Buffalo hides

- 5.3.1 Full grain leather

- 5.3.2 Top grain leather

- 5.3.3 Split leather

- 5.4 Horse hides

- 5.4.1 Horse leather (chrome-tanned)

- 5.4.2 Horse leather (vegetable tanned)

- 5.4.3 Horse hides suede

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Natural

- 6.3 Synthetic

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Machine pulled

- 7.3 Hand-flayed

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Clothing

- 8.3 Footwear

- 8.4 Upholstery

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AJHollander Enterprises Inc.

- 10.2 Allanasons Pvt Ltd

- 10.3 AI Bravo Leather Industries

- 10.4 BAHIRDAR Tannery

- 10.5 Merpiel

- 10.6 Norilia Nordic AS

- 10.7 Naugra

- 10.8 Rose International

- 10.9 Sanimax Corporation

- 10.10 Stan India

- 10.11 Texpac Hide & Skin Ltd.

- 10.12 J & E Sedgwick & Co. Ltd.