|

시장보고서

상품코드

1740940

세라코트(세라믹 기반 코팅) 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Cerakote (Ceramic-Based Coating) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

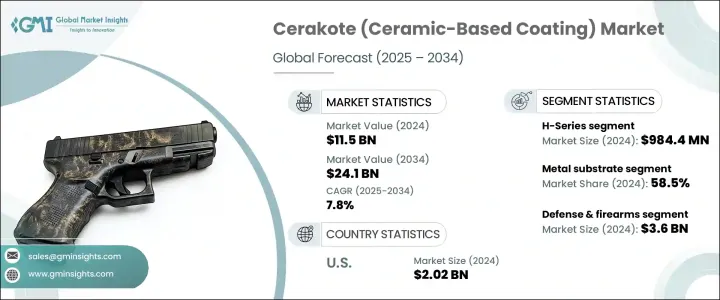

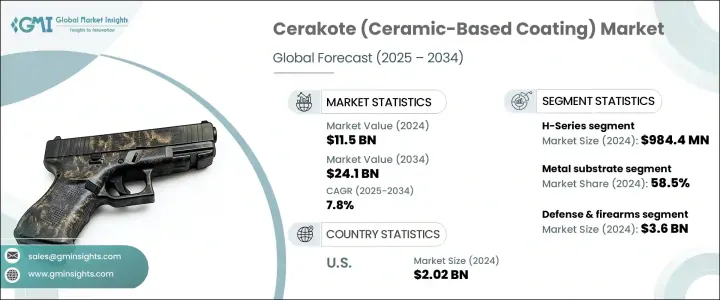

세계의 세라코트(세라믹 기반 코팅) 시장은 2024년 115억 달러로 평가되었으며, 2034년 241억 달러에 이를 것으로 추정되며, CAGR 7.8%로 성장했할 전망입니다.

이 시장은 기술 표준을 충족할 뿐만 아니라 다양한 산업 분야에서 맞춤형 기능을 제공하는 코팅에 대한 수요 증가로 인해 강력한 성장을 경험하고 있습니다. 이러한 급증은 주로 내구성, 내식성 및 미적 매력을 제공하는 고성능 코팅에 대한 수요가 증가함에 따라 주도되고 있습니다. 제조 공정이 더욱 전문화됨에 따라 산업별 요구 사항과 환경 복원력에 부합하는 세라믹 기반 코팅의 채택이 증가하고 있습니다. 기능성과 시각적 세련미를 결합하는 세라코트는 다양한 최종 사용 분야에서 선호되는 소재입니다. 그 중에서도 전자제품은 소비자층이 확대되고 기기 및 액세서리에 내열성, 내마모성, 고급스러운 마감을 제공하는 내구성 있는 코팅에 대한 수요가 증가함에 따라 주목할 만한 성장세를 보이고 있습니다. 이러한 특성 덕분에 세라코트는 까다로운 조건에 노출된 기판 코팅을 위한 최고 수준의 솔루션으로 자리매김했습니다.

H-시리즈는 제품 부문을 주도하며 2024년 9억 8,440만 달러의 가치를 인정받았습니다. 이 시리즈는 2025년에서 2034년 사이에 8.4%의 연평균 성장률을 보일 것으로 예상됩니다. 내화학성, 부식 방지 및 마모 내구성의 강력한 조합으로 인해 가장 상업적으로 성공적인 제품 라인으로 남아 있습니다. 성능과 외관이 모두 중요한 수많은 산업 분야에서 그 효과가 입증되었습니다. 이 시장은 다양한 용도의 요구 사항에 따라 특정 성능 벤치마크를 충족하도록 개발된 C-시리즈, 엘리트 시리즈, 글래시어 시리즈, 클리어 코트 등의 다른 제품 라인으로도 구성됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 115억 달러 |

| 예측 금액 | 241억 달러 |

| CAGR | 7.8% |

세라코트 코팅은 기질 호환성에 따라 분류되며, 금속, 폴리머 및 플라스틱, 복합재, 목재가 주요 재료 카테고리로 사용됩니다. 2024년에는 금속이 전 세계 시장 점유율의 58.5%를 차지하며 이 부문을 지배했습니다. 이러한 우위는 환경 노출, 내마모성, 수명이 필수적인 산업에서 금속 부품이 광범위하게 사용되는 데서 비롯된 것입니다. 철 및 비철 금속 모두에 대한 코팅의 우수한 접착력은 스트레스가 많은 환경에서 그 매력을 더합니다. 세라코트의 분자 결합 능력은 제조 및 고강도 응용 분야에 사용되는 금속을 강화하는 데 중요한 역할을 합니다.

폴리머와 플라스틱은 일반적으로 기본 재료의 구조적 무결성을 유지하기 위해 상온에서 경화되는 C-시리즈 제형으로 코팅됩니다. 반면 목재 기판은 코팅의 내습성 및 스크래치 방지 기능으로 특히 표면 디자인이 중요한 미관 중심 용도에서 이점을 누릴 수 있습니다. 이러한 코팅은 단순한 보호 기능을 넘어 소재의 내구성을 희생하지 않으면서도 창의적인 커스터마이징을 가능하게 합니다.

최종 이용 산업별로는 방위 및 총기 부문은 2024년 36억 달러의 시장 가치와 2034년까지 6.7%의 연평균 성장률을 기록하며 가장 큰 기여를 한 분야로 부상했습니다. 이 부문은 극한 조건에서 안정적으로 작동하는 코팅에 대한 수요 증가에 힘입어 전체 시장의 31%를 차지했습니다. 세라코트는 열 안정성과 내마모성이 뛰어나 성능과 표면 무결성이 중요한 전술 장비 및 무기에 특히 적합합니다.

세라코트 시장의 적용 방법은 크게 스프레이 코팅, 열 경화, 공기 건조로 세분화됩니다. 스프레이 코팅은 균일하고 얇은 층을 생성하는 데 효율적이기 때문에 시각적 매력과 매끄러운 마감이 필수적인 응용 분야에서 계속 선두를 달리고 있습니다. 열 경화는 주로 최고의 내구성과 내화학성이 요구되는 상황에 적용되며, 공기 건조는 플라스틱, 복합재, 목재 등 열에 민감한 피착재에 더 적합합니다.

2024년에는 미국이 20억 2,000만 달러의 평가액으로 세계 시장에서 큰 점유율을 차지하고 있습니다. 국내 시장은 2025년부터 2034년까지 7.8%의 연평균 성장률을 보일 것으로 예상됩니다. 자동차, 군사, 소비재 등 고성능 산업에서 수요가 증가하면서 성장세를 이어가고 있습니다. 맞춤형 미적 마감과 부품 수명 주기의 연장은 시장 확대의 핵심 동력입니다. 내구성 코팅과 산업 표준에 대한 규제 인식도 세라믹 기반 솔루션의 채택을 늘리는 데 기여했습니다.

주요 제조업체들이 혁신, 전략적 협업, 글로벌 유통망 확장에 막대한 투자를 하면서 경쟁 환경은 더욱 치열해지고 있습니다. 상위권 기업들은 생산 기술을 최적화하고 제품 품질의 일관성을 유지하며 OEM 및 애프터마켓 채널 전반에서 입지를 강화하는 데 주력하고 있습니다. 또한 주요 기업들은 브랜드 신뢰와 고객 충성도를 구축하기 위해 인증, 자체 테스트 역량, 기술 서비스에 우선순위를 두고 있습니다. 고성능의 시각적으로 매력적인 코팅에 대한 수요가 증가함에 따라 제조업체들은 첨단 R&D 및 공정 개발을 통해 기대치를 충족하기 위해 경쟁하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 총기 및 방위 산업에서 고성능 코팅에 대한 수요 증가

- 자동차 커스터마이징 및 애프터마켓 서비스 증가

- 항공우주 분야에서 경량, 고열 부품에 대한 사용 증가

- 산업 장비의 고온 코팅에 대한 수요 급증

- 업계의 잠재적 위험 및 과제

- 기존 코팅에 비해 높은 도포 및 경화 비용

- 제한된 브랜드 가용성

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- H-시리즈

- C-시리즈

- 엘리트 시리즈

- 글래시어 시리즈

- 클리어 코트

제6장 시장 추계 및 예측 : 기재 적합성별(2021-2034년)

- 주요 동향

- 금속

- 강철

- 알루미늄

- 티타늄

- 폴리머와 플라스틱

- 복합재료

- 목재

제7장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 방위 및 총기

- 자동차 및 운송

- 항공우주 및 항공

- 가전

- 의료기기

- 산업기기

- 스포츠 및 아웃도어 용품

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 스프레이 코팅

- 열경화

- 공기 건조

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Arrow Finishing

- Cerakote

- KECO Coatings

- KOTEC Ceramic Coatings

- MSP Manufacturing

- Mueller Coatings

- NIC Industries

- Spectrum Coating

- Sun Coating Company

- Tanury Industries

The Global Cerakote (Ceramic-Based Coating) Market was valued at USD 11.5 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 24.1 billion by 2034. The market is experiencing robust growth due to the increasing demand for coatings that not only fulfill technical standards but also deliver tailored functionality across different industries. This surge is primarily driven by the rising need for high-performance coatings that offer durability, corrosion resistance, and aesthetic appeal. As manufacturing processes become more specialized, there's growing adoption of ceramic-based coatings that align with industry-specific requirements and environmental resilience. Cerakote's ability to combine functionality with visual sophistication makes it a preferred choice across various end-use sectors. Among these, electronics are witnessing notable traction due to the expanding consumer base and the growing demand for durable coatings that offer heat resistance, wear protection, and a premium finish on devices and accessories. These qualities have positioned cerakote as a top-tier solution for coating substrates exposed to demanding conditions.

The H-Series led the product segment and was valued at USD 984.4 million in 2024. This series is anticipated to witness a CAGR of 8.4% between 2025 and 2034. It remains the most commercially successful product line due to its strong combination of chemical resistance, corrosion protection, and wear durability. Its effectiveness has proven reliable across numerous industrial uses where both performance and appearance matter. The market comprises other product lines as well, such as the C-Series, Elite Series, Glacier Series, and Clear Coats, each developed to meet specific performance benchmarks in line with various application needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.5 Billion |

| Forecast Value | $24.1 Billion |

| CAGR | 7.8% |

Cerakote coatings are classified based on substrate compatibility, with metals, polymers & plastics, composites, and wood serving as the primary material categories. Metals dominated the segment in 2024, accounting for 58.5% of the global market share. This dominance stems from the widespread use of metallic components in industries where environmental exposure, wear resistance, and longevity are essential. The coating's superior adhesion to both ferrous and non-ferrous metals adds to its attractiveness in high-stress environments. Cerakote's molecular bonding capability plays a significant role in reinforcing metals used in manufacturing and heavy-duty applications.

Polymers and plastics are typically coated with C-Series formulations, which cure at ambient temperatures to maintain the structural integrity of the base materials. In contrast, wood substrates benefit from the coating's moisture resistance and scratch protection, especially in aesthetic-focused uses where surface design matters. These coatings offer more than just protection; they allow for creative customization without sacrificing material durability.

In terms of end-use industries, the defense and firearms sector emerged as the largest contributor, with a market value of USD 3.6 billion in 2024 and an expected CAGR of 6.7% through 2034. This segment represented 31% of the overall market, driven by growing demand for coatings that perform reliably under extreme conditions. The thermal stability and abrasion resistance of cerakote make it particularly suitable for tactical equipment and weaponry, where performance and surface integrity are critical.

Application methods in the cerakote market are primarily segmented into spray coating, heat curing, and air drying. Spray coating continues to lead due to its efficiency in producing even, thin layers, which is critical for applications where visual appeal and smooth finishes are essential. Heat curing is mainly applied in situations that demand peak durability and chemical resistance, whereas air drying is more appropriate for heat-sensitive substrates, including plastics, composites, and wood.

In 2024, the United States held a significant share of the global market, with a valuation of USD 2.02 billion. The domestic market is forecasted to grow at a 7.8% CAGR between 2025 and 2034. Increased demand from high-performance industries such as automotive, military, and consumer goods continues to boost growth. Customized aesthetic finishes and extended component lifecycles are key drivers for market expansion. Regulatory awareness around durable coatings and industry standards has also led to increased adoption of ceramic-based solutions.

The competitive environment is intensifying as leading manufacturers invest heavily in innovation, strategic collaborations, and expansion of global distribution networks. Top-tier companies are focusing on optimizing production techniques, maintaining consistency in product quality, and strengthening their presence across OEM and aftermarket channels. Key players are also prioritizing certifications, in-house testing capabilities, and technical services to build brand trust and customer loyalty. As demand for high-performance and visually appealing coatings grows, manufacturers are racing to meet expectations through advanced R&D and process development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for high-performance coatings in firearms and defense.

- 3.7.1.2 Increasing automotive customization and aftermarket services.

- 3.7.1.3 Growing use in aerospace for lightweight, high-heat components.

- 3.7.1.4 Surge in demand for high-temperature coatings in industrial equipment

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High application and curing costs compared to traditional coatings.

- 3.7.2.2 Limited brand availability.

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 H-series

- 5.3 C-series

- 5.4 Elite series

- 5.5 Glacier series

- 5.6 Clear coats

Chapter 6 Market Estimates & Forecast, By Substrate Compatibility, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Metals

- 6.2.1 Steel

- 6.2.2 Aluminum

- 6.2.3 Titanium

- 6.3 Polymers & plastics

- 6.4 Composites

- 6.5 Wood

Chapter 7 Market Estimates & Forecast, By Application Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Defense & firearms

- 7.3 Automotive & transportation

- 7.4 Aerospace & aviation

- 7.5 Consumer electronics

- 7.6 Medical devices

- 7.7 Industrial equipment

- 7.8 Sporting & outdoor goods

Chapter 8 Market Estimates & Forecast, By Application Method, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Spray coating

- 8.3 Heat curing

- 8.4 Air drying

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arrow Finishing

- 10.2 Cerakote

- 10.3 KECO Coatings

- 10.4 KOTEC Ceramic Coatings

- 10.5 MSP Manufacturing

- 10.6 Mueller Coatings

- 10.7 NIC Industries

- 10.8 Spectrum Coating

- 10.9 Sun Coating Company

- 10.10 Tanury Industries