|

시장보고서

상품코드

1740996

성형 펄프 포장 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Molded Pulp Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

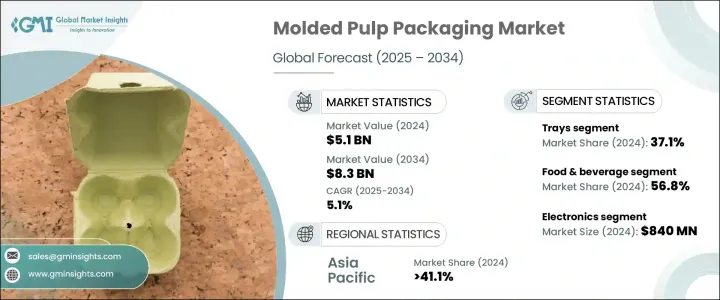

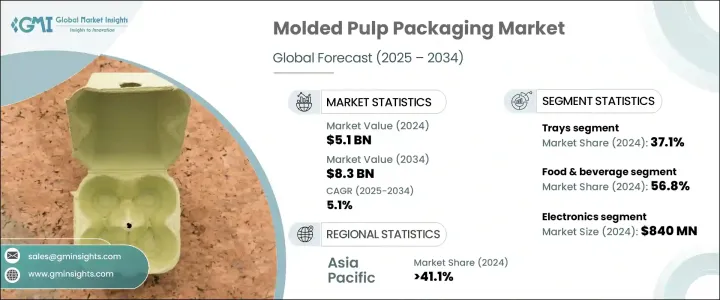

세계의 성형 펄프 포장 시장은 2024년 51억 달러로 평가되었고, CAGR 5.1%로 성장할 전망이며, 2034년에는 83억 달러에 이를 것으로 예측됩니다.

이 성장의 원동력이 되고 있는 것은 환경 폐기물을 삭감하는 세계의 대처와 함께, 지속 가능한 패키징 솔루션에 대한 시프트가 진행되고 있는 것입니다. 일회용 플라스틱에 대한 규제가 강화되고, 소비자의 환경 의식이 높아짐에 따라, 생분해성으로 재활용 가능한 대체품에 대한 수요가 계속 증가하고 있습니다. 재생 가능한 섬유 기반 소재로 만든 성형 펄프 포장은 기존의 플라스틱 포장을 대체하는 지속 가능한 대체품을 제공하고 다양한 업계에서 지지를 모으고 있습니다. 퇴비화나 재활용이 가능한 이 소재는, 환경 목표를 달성해, 환경 친화적인 이미지의 향상을 목표로 하는 브랜드에 있어서, 바람직한 선택 사항이 되고 있습니다.

성형 펄프 포장 시장은 특히 전자상거래 및 소매 분야에서 플라스틱 사용 규제가 높아짐에 따라 큰 열기를 보이고 있습니다. 이러한 규제는, 기업을 환경 친화적인 포장 솔루션으로 끌어올리고 있습니다. 미국의 수입 관세와 같은 무역 정책은 펄프의 국내 조달을 장려함으로써 지역 공급망을 강화하는 데 도움이 되고 있습니다. 이 동향은 해외 공급업체에 대한 의존을 줄이고, 특히 수입 비용 상승이 지속될 경우에는 지역 펄프 업체에 이익을 가져다 줄 가능성이 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 51억 달러 |

| 예측 금액 | 83억 달러 |

| CAGR | 5.1% |

제품 유형 중에서는 성형 펄프 트레이가 지배적인 부문이 되어 2024년에는 19억 달러를 창출했습니다. 이 분야는 트레이의 보호 특성과 환경 배려의 매력으로 인해 CAGR 5.2%의 성장이 전망되고 있습니다. 산업계가 보다 지속 가능한 사업으로 이행함에 따라 성형 펄프 트레이의 수요는 증가하여 동 분야의 성장에 박차를 가할 것으로 예상됩니다.

2024년에 29억 달러로 평가되는 식음료 산업도 시장 확대의 주요 요인입니다. 2034년까지 CAGR 4.9%로 성장할 것으로 예측되는 이 업계에서는 규제를 준수하고 환경 의식이 높은 소비자에게 대응하기 위해 성형 펄프 포장의 채택이 진행되고 있습니다. 기업이 지속 가능성을 우선시함으로써 소비자의 로열티가 향상되고 식품 관련 용도에서의 성형 펄프 포장의 지속적인 채택이 촉진됩니다.

2024년 시장의 41.1% 점유율을 차지한 아시아태평양은 CAGR 5.6%를 보일 것으로 예측됩니다. 급속한 공업화, 활황을 보이는 전자상거래 부문, 중국, 인도, 일본, 동남아시아 등 주요 시장에서 지속 가능한 패키징에 대한 의식이 높아지면서 플라스틱을 대체하는 펄프 성형품 수요를 촉진하고 있습니다. 이 지역의 경쟁력은 원재료의 입수 가능성, 낮은 생산 비용, 대규모 생산 능력에 의해 더욱 강화되고 있습니다.

Huhtamaki, Eco Pulp Packaging, Dart Container Corporation, Henry Molded Products Inc., Pactiv Evergreen Inc., UFP Technologies Inc.와 같은 시장 선도 기업들은 제품 라인 확대 및 자동화 투자에 주력하여 수요 증가에 대응하고 있습니다. 소매업체 및 FMCG 브랜드와의 전략적 파트너십은 유통망을 강화하고, 지속 가능한 혁신 및 생분해성 소재에 대한 투자는 시장에서의 입지 굳히기에 도움이 되고 있습니다. 게다가 이들 기업은 새로운 지역 시장에 참가해 장기적인 브랜드 가치를 키우기 위해 순환 경제 이니셔티브와 제휴하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망 및 향후 검토 사항

- 무역에 미치는 영향

- 벤더 매트릭스

- 이익률 분석

- 기술 및 혁신의 상황

- 특허 분석

- 주요 뉴스 및 대처

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전자상거래에서 지속가능한 포장 채용 증가

- 헬스케어 포장 분야에서 채용 증가

- 친환경 포장을 촉진하는 규제 강화

- 환경에 미치는 영향에 대한 소비자 의식 증가

- 신흥 시장에서의 지속 가능한 관행의 출현

- 업계의 잠재적 위험 및 과제

- 긴 생산 사이클

- 바이오플라스틱과의 경쟁

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 장래 시장 동향

- 규제 상황

제4장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 트레이

- 클램쉘

- 컵과 그릇

- 플레이트

- 기타

제5장 시장 추계 및 예측 : 성형 기술별(2021-2034년)

- 주요 동향

- 두꺼운 성형

- 트랜스퍼 성형

- 열성형 펄프

- 가공 펄프

제6장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 식품 및 음료

- 일렉트로닉스

- 헬스케어

- 자동차

- 화장품 및 퍼스널케어

- 기타

제7장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 일본

- 중국

- 인도

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 기타 중동 및 아프리카

제8장 기업 프로파일

- Best Plus Pulp Factory

- buhl-paperform GmbH

- CKF Inc.

- Dart Container Corporation

- Eco Pulp Packaging

- EnviroPAK

- Green Pack.

- Hartmann Packaging

- Henry Molded Products Inc.

- Huhtamaki

- HZ Green Pulp Sdn Bhd

- Keiding, Inc.

- Pacific Pulp Molding, Inc

- Pactiv Evergreen Inc.

- Primapack

- Sabert Corporation

- UFP Technologies, Inc.

- Western Pulp Products Company

The Global Molded Pulp Packaging Market was valued at USD 5.1 billion in 2024 and is projected to grow at a CAGR of 5.1% to reach USD 8.3 billion by 2034. This growth is being driven by the increasing shift toward sustainable packaging solutions alongside a global effort to reduce environmental waste. As stricter regulations on single-use plastics take hold and consumers become more environmentally conscious, the demand for biodegradable and recyclable alternatives continues to rise. Molded pulp packaging, made from renewable fiber-based materials, is gaining traction across various industries, offering a sustainable alternative to traditional plastic packaging. This material's compostability and recyclability make it the preferred choice for brands aiming to meet their environmental goals and bolster their eco-friendly image.

The molded pulp packaging market is also experiencing substantial momentum due to growing restrictions on plastic use, particularly in the e-commerce and retail sectors. These restrictions are pushing companies toward eco-friendly packaging solutions. National and international policies favoring green alternatives are further accelerating the market's adoption, with trade policies, like import tariffs in the U.S., helping to strengthen local supply chains by encouraging domestic sourcing of pulp. This trend could reduce reliance on foreign suppliers, benefiting regional pulp producers, especially if import costs continue to rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 5.1% |

Among product types, molded pulp trays have become a dominant segment, generating USD 1.9 billion in 2024. This segment is expected to grow at a CAGR of 5.2%, driven by the trays' protective properties and eco-conscious appeal. As industries move toward more sustainable operations, demand for molded pulp trays is expected to increase, fueling segment growth.

The food and beverage industry, valued at USD 2.9 billion in 2024, is also a major driver of market expansion. Projected to grow at a CAGR of 4.9% through 2034, the sector is increasingly adopting molded pulp packaging to comply with regulatory mandates and cater to environmentally aware consumers. As companies prioritize sustainability, they enhance consumer loyalty and encourage the continued adoption of molded pulp packaging in food-related applications.

The Asia Pacific region, which held a 41.1% share of the market in 2024, is forecasted to grow at a CAGR of 5.6%. Rapid industrialization, a booming e-commerce sector, and heightened awareness of sustainable packaging in key markets such as China, India, Japan, and Southeast Asia are driving demand for molded pulp alternatives to plastic. The region's competitive edge is further strengthened by the availability of raw materials, lower production costs, and large-scale manufacturing capabilities.

Leading market players such as Huhtamaki, Eco Pulp Packaging, Dart Container Corporation, Henry Molded Products Inc., Pactiv Evergreen Inc., and UFP Technologies, Inc. are focusing on expanding their product lines and investing in automation to meet growing demand. Strategic partnerships with retailers and FMCG brands are enhancing their distribution networks, while investments in sustainable innovations and biodegradable materials are helping them solidify their market position. Additionally, these companies are entering new regional markets and aligning with circular economy initiatives to foster long-term brand value.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Vendor matrix

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news and initiatives

- 3.8 Industry impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing adoption of sustainable packaging in e-commerce

- 3.8.1.2 Increased adoption by healthcare packaging sectors

- 3.8.1.3 Rising regulations promoting eco-friendly packaging

- 3.8.1.4 Rising consumer awareness of environmental impacts

- 3.8.1.5 Emergence of sustainable practices in emerging markets

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Lengthy production cycles

- 3.8.2.2 Competition from bioplastics

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Future market trends

- 3.13 Regulatory landscape

Chapter 4 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Bn & Kilo Tons)

- 4.1 Key trends

- 4.2 Trays

- 4.3 Clamshells

- 4.4 Cups and bowls

- 4.5 Plates

- 4.6 Others

Chapter 5 Market Estimates and Forecast, By Molding Technology, 2021 - 2034 (USD Bn & Kilo Tons)

- 5.1 Key trends

- 5.2 Thick-Wall molding

- 5.3 Transfer molding

- 5.4 Thermoformed pulp

- 5.5 Processed pulp

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Bn & Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.3 Electronics

- 6.4 Healthcare

- 6.5 Automotive

- 6.6 Cosmetics & personal care

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Bn & Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 ANZ

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 UAE

- 7.6.3 Saudi Arabia

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Best Plus Pulp Factory

- 8.2 buhl-paperform GmbH

- 8.3 CKF Inc.

- 8.4 Dart Container Corporation

- 8.5 Eco Pulp Packaging

- 8.6 EnviroPAK

- 8.7 Green Pack.

- 8.8 Hartmann Packaging

- 8.9 Henry Molded Products Inc.

- 8.10 Huhtamaki

- 8.11 HZ Green Pulp Sdn Bhd

- 8.12 Keiding, Inc.

- 8.13 Pacific Pulp Molding, Inc

- 8.14 Pactiv Evergreen Inc.

- 8.15 Primapack

- 8.16 Sabert Corporation

- 8.17 UFP Technologies, Inc.

- 8.18 Western Pulp Products Company