|

시장보고서

상품코드

1750292

냉간 마무리 봉강 및 바 사이즈 형상 시장 : 기회, 성장 촉진요인, 산업 동향 분석 예측(2025-2034년)Cold-Finished Iron and Steel Bars and Bar-Size Shapes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

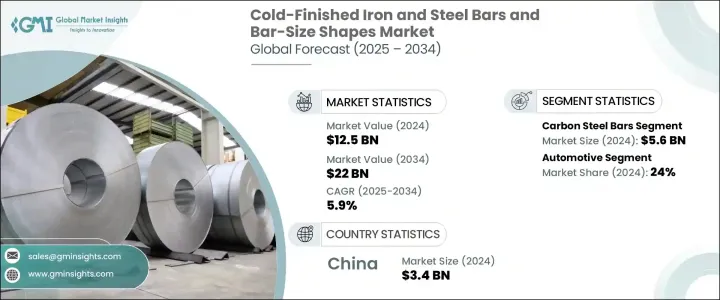

세계의 냉간 마무리 봉강 및 바 사이즈 형상 시장은 2024년 125억 달러로 평가되어 CAGR 5.9%로 성장하고, 2034년까지 220억 달러에 이를 것으로 예측되고 있습니다.

냉간 마무리 봉강은 높은 치수 정밀도, 우수한 표면 마감, 내구성이 평가되며 자동차, 건설, 항공우주, 일반 기계 등의 산업에서 필수적입니다. 정밀 가공된 철강 부품 수요는 특히 신흥 시장에서 현저한 성장을 보이고 있으며 산업 부문은 특수 용도를 위한 고품질 재료에 대한 의존도를 높이고 있습니다. 이 급증은 내구성, 성능, 치수 정밀도를 향상시킨 철강 부품을 필요로 하는 자동차, 항공우주, 건설, 기계 등 산업의 확대로 인한 것이 큽니다.

우수한 표면 마감과 엄격한 치수로 알려진 냉간 마무리 봉강은 이러한 요구를 충족시키는 데 중요한 역할을 합니다. 이러한 봉강을 제조하는 주요 공정 중 하나는 냉간 인발 가공이 있어 고정밀도로 매끄러운 부품을 제조할 수 있기 때문에 선호되고 있습니다. 이 공정은 또한 봉강의 기계적 특성을 향상시키고 강도와 피로 저항이 필수적인 고응력 용도에 적합합니다. 이러한 공정의 진화와 생산기술의 끊임없는 진보로 제조업체 각사는 특정 산업 요구에 맞추어 점점 더 정교한 재료를 생산할 수 있게 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 125억 달러 |

| 예측 금액 | 220억 달러 |

| CAGR | 5.9% |

탄소강 봉강 부문은 2024년 56억 달러를 차지하고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.5%를 보일 것으로 예측됩니다. 탄소강은 기계 가공이나 용접이 용이하기 때문에 건설, 자동차, 기계 등의 분야에서 널리 사용되고 있습니다. 공구강과 특수봉강(SBQ)과 같은 특수강종은 인성과 내피로성이 강화되어 자동차 단조, 광업, 금형 제조업에 필수적입니다.

2024년 62억 달러로 평가된 냉간 인발 봉강 부문은 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 6.5%를 보일 것으로 예측됩니다. 가공의 주요 이점 중 하나는 열간 성형법에 비해 조업 비용이 낮기 때문에 사용하는 에너지가 30-50% 적게 됩니다.

중국 냉간 마무리 봉강 및 바 사이즈 형상 2024년 시장 규모는 34억 달러로, CAGR은 6.1%로 예측되고 있습니다. 세계의 제조 거점인 중국은 주로 견조한 산업기계와 건설 산업에 의해 이러한 제품에 대한 높은 국내 수요를 가지고 있습니다.

Nucor, ArcelorMittal, Timken Steel, JSW Steel, TaeguTec 등의 기업은 시장 점유율을 유지하고 확장하기 위해 몇 가지 중요한 전략을 채택하고 있습니다. 이러한 기업은 특수 고성능 냉간 마무리 봉강 수요 증가에 대응하기 위해 제품 라인업의 확대에 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

참고: 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 자동차 업계에서는 경량이고 고강도의 부품에 대한 수요가 높아져, 사용량이 증가하고 있습니다.

- 세계의 인프라 프로젝트에 의해 내구성이 있는 철강 재료 수요가 높아지고 있습니다.

- 전기자동차의 성장에 의해 정밀하게 가공된 강봉 수요가 높아지고 있습니다.

- 제조업의 진보에 의해 생산 효율과 제품 품질이 향상됩니다.

- 업계의 잠재적 위험 및 과제

- 원재료 가격의 변동은 제조업체에게 있어서 비용의 불확실성을 낳습니다.

- 생산시에 에너지를 대량으로 소비하면, 운용 비용이 대폭 증가합니다.

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 탄소강봉

- 합금강봉

- 스테인리스 강봉

- 공구강봉

- 스페셜 바 품질(SBQ)

제6장 시장 추계 및 예측 : 형상별, 2021-2034년

- 주요 동향

- 둥근 막대

- 육각형 막대

- 각봉

- 플랫바

- 특수 형상

제7장 시장 추계 및 예측 : 제조 공정별, 2021-2034년

- 주요 동향

- 냉간 인발

- 선삭 및 연마

- 연마

- 복합 프로세스

제8장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 자동차

- 기계

- 건설

- 항공우주

- 에너지

- 소비재

- 기타

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Nucor Corporation

- Gerdau SA

- ArcelorMittal

- Steel Dynamics, Inc.

- Tata Steel

- POSCO

- Baowu Steel Group

- Eaton Steel Bar Company

- Ovako AB

- Sanyo Special Steel

- Commercial Metals Company

- Aichi Steel Corporation

- Kobe Steel, Ltd.

- Daido Steel

- Saarstahl AG

- Fushun Special Steel

The Global Cold-Finished Iron and Steel Bars and Bar-Size Shapes Market was valued at USD 12.5 billion in 2024, and is estimated to grow at a CAGR of 5.9% to reach USD 22 billion by 2034, as cold-finished bars are valued for their high dimensional accuracy, superior surface finish, and durability, making them essential in industries such as automotive, construction, aerospace, and general machinery. The demand for precision-engineered steel components is witnessing significant growth, especially in emerging markets where industrial sectors are increasingly relying on high-quality materials for specialized applications. This surge is largely driven by the expansion of industries such as automotive, aerospace, construction, and machinery, which require steel components that offer enhanced durability, performance, and dimensional accuracy.

Cold-finished iron and steel bars, known for their superior surface finish and exacting dimensions, play a crucial role in meeting these needs. One of the primary processes for producing these bars is cold drawing, which is favored for its ability to create highly accurate and smooth components. This process also improves the mechanical properties of the bars, making them suitable for high-stress applications where strength and fatigue resistance are essential. The evolution of these processes, combined with continuous advancements in production techniques, is allowing manufacturers to produce increasingly sophisticated materials tailored for specific industrial needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.5 billion |

| Forecast Value | $22 billion |

| CAGR | 5.9% |

The carbon steel bars segment accounted for USD 5.6 billion in 2024 and is expected to grow at a CAGR of 5.5% from 2025 to 2034. Carbon steel is widely used in sectors like construction, automotive, and machinery due to its ease of machining and welding. It's also integral to manufacturing custom components for structural and mechanical frameworks. Specialized types, like tool steel and Special Bar Quality (SBQ) bars, offer enhanced toughness and fatigue resistance, making them vital for automotive forging, mining, and die-making industries. These properties help ensure high performance in demanding environments.

Cold-drawn bars segment, valued at USD 6.2 billion in 2024, is expected to grow at a CAGR of 6.5% during 2025-2034. The cold-drawing process is especially popular for its accuracy, superior surface finish, and mechanical properties. This method is widely used in the automotive and aerospace sectors, as well as in industrial machining. One of the key advantages of cold drawing is its lower operational costs compared to hot forming methods, using 30-50% less energy. This makes it an attractive option for companies looking to optimize production efficiency.

China Cold-Finished Iron and Steel Bars and Bar-Size Shapes Market was valued at USD 3.4 billion in 2024, with a projected CAGR of 6.1%. As a global manufacturing hub, China has a high domestic demand for these products, driven primarily by its robust industrial machinery and construction industries. The demand for cold-finished steel bars in China continues to rise, reinforcing the country's position as a critical player in the global market.

Companies like Nucor, ArcelorMittal, Timken Steel, JSW Steel, and TaeguTec are adopting several key strategies to maintain and grow their market share. These strategies include continuous investments in advanced manufacturing technologies to improve efficiency, product quality, and innovation. Additionally, these companies are focusing on expanding their product offerings to meet the increasing demand for specialized and high-performance cold-finished bars. By optimizing production processes and investing in R&D, these players are positioning themselves to capture a larger share of the growing market while maintaining a competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Market highlights and key findings

- 2.3 Current market valuation and growth projections

- 2.4 Key market trends and developments

- 2.5 Competitive landscape overview

- 2.6 Strategic recommendations for stakeholders

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Automotive industry's demand for lightweight, high-strength components boosts usage.

- 3.7.1.2 Infrastructure projects worldwide increase need for durable steel materials.

- 3.7.1.3 Electric vehicle growth drives demand for precision-engineered steel bars.

- 3.7.1.4 Advancements in manufacturing enhance production efficiency and product quality.

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Fluctuating raw material prices create cost uncertainties for manufacturers.

- 3.7.2.2 High energy consumption in production raises operational expenses significantly.

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Carbon steel bars

- 5.3 Alloy steel bars

- 5.4 Stainless steel bars

- 5.5 Tool steel bars

- 5.6 Special bar quality (SBQ)

Chapter 6 Market Estimates & Forecast, By Shape, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Round bars

- 6.3 Hexagonal bars

- 6.4 Square bars

- 6.5 Flat bars

- 6.6 Special shapes

Chapter 7 Market Estimates & Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Cold-drawn

- 7.3 Turned and polished

- 7.4 Ground and polished

- 7.5 Combined processes

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Machinery

- 8.4 Construction

- 8.5 Aerospace

- 8.6 Energy

- 8.7 Consumer goods

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Nucor Corporation

- 10.2 Gerdau S.A.

- 10.3 ArcelorMittal

- 10.4 Steel Dynamics, Inc.

- 10.5 Tata Steel

- 10.6 POSCO

- 10.7 Baowu Steel Group

- 10.8 Eaton Steel Bar Company

- 10.9 Ovako AB

- 10.10 Sanyo Special Steel

- 10.11 Commercial Metals Company

- 10.12 Aichi Steel Corporation

- 10.13 Kobe Steel, Ltd.

- 10.14 Daido Steel

- 10.15 Saarstahl AG

- 10.16 Fushun Special Steel