|

시장보고서

상품코드

1750306

첨단 광학 재료 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Advanced Optics Material Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

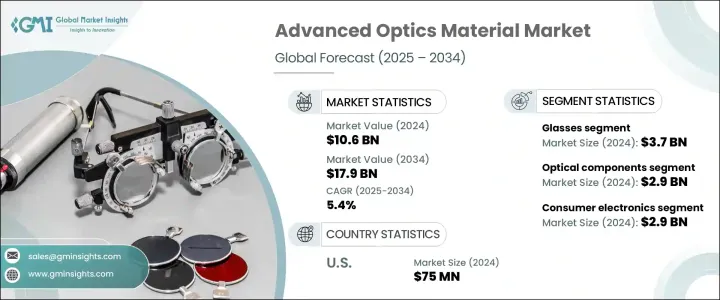

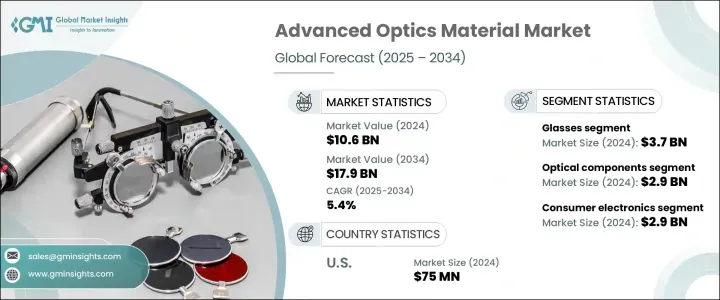

세계의 첨단 광학 재료 시장은 2024년 106억 달러로 평가되었고, CAGR 5.4%로 성장해 2034년까지 179억 달러에 이를 것으로 예측됩니다.

AR, VR, LiDAR, 디지털 기술의 급속한 채용이 자동차 시스템, 스마트 가전, 방위용도에서 첨단 광학 부품의 중요성을 높이고 있습니다.

제조의 진보, 특히 AI 구동형 적층 조형 및 레이저 지원 프로세스에 의해 커스텀 광학 부품의 실현성과 확장성이 높아지고 있습니다. 이는 항공우주, 방위, 생물의학 이미징 등의 분야에서 특히 가치가 있습니다. 보다 컴팩트하고 가볍고 효율적인 광학 솔루션의 진화를 뒷받침하고 있습니다. 증강현실, 양자 컴퓨팅, 포토닉 칩의 혁명적인 발전에 대한 길을 열어 이러한 기술 혁신에 의해 새로운 성능 벤치마크가 설정되어 첨단 광학의 프론티어가 확산되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 106억 달러 |

| 예측 금액 | 179억 달러 |

| CAGR | 5.4% |

재료별로는 유리가 2024년 시장 점유율 35.3%를 차지하고, 평가액은 37억 달러였습니다. 제품과 의료기기에 사용되고 있습니다. 내자외선성과 굴절 성능을 강화한 새로운 폴리머 조성은 그 유용성을 확대하고 있습니다.

가전기기 부문은 2024년에 29억 달러를 차지해 2034년까지 CAGR 5.9%로 예측되고 있습니다. 헬스케어 분야에서는 진단 툴, 수술 장치, 생체 적합 기구에 광학계를 통합하여 정확도와 환자의 안전성을 높이고 있습니다.

미국의 첨단 광학 재료 시장은 7,500만 달러에 이르고, CAGR 6.9%를 보일 것으로 예측되고 있습니다.

이 업계의 주요 기업은 Hoya Corporation, Edmund Optics, CoorsTek, Heraeus Holding, Corning Incorporated 등이 있습니다. 이들 기업은 연구 개발 투자의 확대, 이업종 협업의 형성, 제조 능력의 강화에 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급 체인 구조

- 생산 비용에 미치는 영향

- 공급측의 영향(원재료)

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS 코드) 참고: 위의 무역 통계는 주요 국가에 대해서만 제공됩니다

- 주요 수출국, 2021-2024년

- 주요 수입국, 2021-2024년

- 공급자의 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 고성능 광학 부품 수요 증가

- 포토닉스와 양자 광학의 진보

- 통신에 있어서의 용도 증가

- 헬스케어 및 의료기기 채용 증가

- 업계의 잠재적 리스크 및 과제

- 높은 생산 비용

- 원재료 공급

- 규제상의 과제

- 성장 촉진요인

- 시장 기회

- 증강현실과 가상현실에 있어서의 새로운 응용

- 고도 감지 기술에 대한 수요 증가

- 자율주행 시스템 확대

- 생체 모방 광학 재료의 개발

- 성장 가능성 분석

- 규제 틀 분석

- REACH 및 ROHS 규정

- 수출관리규제

- 환경 컴플라이언스 요건

- 취급 및 처리에 관한 안전기준

- 기술의 정세

- 현재의 기술 동향

- 신흥기술

- 연구개발 이니셔티브와 혁신 파이프라인

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 시장 점유율 분석

- 제조업체별 세계 시장 점유율

- 제조업체별 지역 시장 점유율

- 경쟁 벤치마킹

- 제품 포트폴리오 비교

- 기술력의 비교

- R&D 투자 비교

- 제조능력 비교

- 전략적 노력과 개발

- 합병과 인수

- 파트너십 및 협업

- 제품 출시와 혁신

- 확장 계획

- 경쟁 포지셔닝 매트릭스

- 전략적 대시보드

제5장 시장 추계 및 예측 : 재료별, 2021-2034년

- 주요 동향

- 유리 재료

- 광학 유리

- 용융 실리카

- 붕규산 유리

- 특수 유리

- 기타

- 고분자 재료

- 폴리메틸메타크릴레이트(PMMA)

- 폴리카보네이트(PC)

- 환상 올레핀 폴리머(COP)

- 환상 올레핀 공중합체(COC)

- 기타

- 결정 재료

- 사파이어

- 실리콘

- 게르마늄

- 셀레늄화 아연

- 불화칼슘

- 기타

- 세라믹 재료

- 투명 세라믹

- 알루미늄 옥시나이트 라이드(ALON)

- 마그네슘 알루미네이트 스피넬

- 이트륨 알루미늄 가닛(YAG)

- 기타

- 금속재료

- 알루미늄

- 은

- 금

- 기타

- 첨단 복합재료

- 포토닉 결정

- 메타물질

- 나노 재료

- 기타

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 광학 부품

- 렌즈

- 미러

- 프리즘

- 창

- 필터

- 회절 격자

- 기타

- 광전자 디바이스

- LED

- 레이저 다이오드

- 광검출기

- 태양전지

- 광 변조기

- 기타

- 이미지 시스템

- 카메라

- 현미경

- 망원경

- 열화상

- 기타

- 광통신

- 광섬유

- 도파관

- 광 증폭기

- 광 스위치

- 기타

- 센싱과 계측

- 광학 센서

- 분광법

- 간섭법

- 기타

- 디스플레이 기술

- LCD 디스플레이

- OLED 디스플레이

- AR/VR 디스플레이

- 기타

- 기타

제7장 시장 추계 및 예측 : 최종 이용 산업별, 2021-2034년

- 주요 동향

- 가전

- 스마트폰

- 카메라

- 웨어러블 디바이스

- 기타

- 헬스케어 및 의료

- 진단 기기

- 외과용 기기

- 치료 시스템

- 의료 이미지

- 기타

- 방위 및 안전 보장

- 암시장치

- 조준 시스템

- 감시

- 기타

- 통신

- 광 네트워크

- 데이터센터

- 5G 인프라

- 기타

- 자동차

- 조명 시스템

- 헤드업 디스플레이

- Lidar 시스템

- 운전 지원 시스템

- 기타

- 항공우주

- 항공전자기기

- 네비게이션 시스템

- 위성 부품

- 기타

- 산업

- 머신 비전

- 레이저 가공

- 품질관리

- 기타

- 에너지

- 태양에너지

- 태양광 발전

- 기타

- 연구개발

- 기타

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- CoorsTek

- Corning Incorporated

- Edmund Optics

- Heraeus Holding

- Hoya Corporation

- II-VI Incorporated

- Materion Corporation

- Newport Corporation

- Nikon Corporation

- Ohara Corporation

- SCHOTT

- Sumitomo Electric Industries

- Surmet Corporation

- Thorlabs

- ZEISS Group

The Global Advanced Optics Material Market was valued at USD 10.6 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 17.9 billion by 2034, driven by the increasing demand for precise, high-performance optical components across multiple industries. Rapid adoption of AR, VR, LiDAR, and digital technologies elevates the importance of advanced optics in automotive systems, smart consumer electronics, and defense applications. Similarly, the growing reliance on minimally invasive diagnostics and real-time health monitoring is boosting the adoption of precision optics in the healthcare sector.

Advancements in manufacturing, particularly through AI-driven additive and laser-assisted processes, are making custom optical parts more feasible and scalable. These technologies are reducing production time, minimizing waste, and enabling the precision required for intricate optical geometries, which is especially valuable in fields like aerospace, defense, and biomedical imaging. In parallel, ongoing research in nanostructured and meta-optical materials drives the evolution of more compact, lightweight, and efficient optical solutions across diverse applications. These next-generation materials offer unprecedented control over light behavior, such as bending, filtering, or focusing at nanoscale levels, paving the way for revolutionary developments in augmented reality, quantum computing, and photonic chips. Together, these innovations are setting new performance benchmarks and expanding the frontier of advanced optics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.6 Billion |

| Forecast Value | $17.9 Billion |

| CAGR | 5.4% |

In terms of material, glass held 35.3% market share in 2024 with a valuation of USD 3.7 billion. Glass is favored for its superior clarity and heat stability in high-performance lenses and precision optics. However, polymer-based alternatives gain ground in consumer electronics and medical instruments due to their cost-effectiveness and lightweight properties. Newer polymer compositions with enhanced UV resistance and refractive performance expand their utility. Additionally, specialty materials such as sapphire and lithium niobate are gaining prominence in high-frequency and laser-based systems due to their thermal durability and birefringence characteristics.

The consumer electronics segment accounted for USD 2.9 billion in 2024, with a projected CAGR of 5.9% through 2034. Advancements in smart glasses, foldable displays, and compact, high-resolution cameras fuel demand for multifunctional and space-efficient optical materials. The healthcare sector integrates optics into diagnostic tools, surgical devices, and biocompatible instruments, enhancing precision and patient safety. In defense and industrial security, rugged optics that can withstand extreme temperatures and deliver high-resolution surveillance and targeting are seeing rising demand.

United States Advanced Optics Material Market reached USD 75 million and is expected to grow at a 6.9% CAGR, underpinned by a concentration of aerospace, defense, and tech development activities across the region. Substantial government and private investment in photonics, integrated optics, and quantum technologies is further propelling the use of novel materials like silicon nitride and lithium niobate in next-gen communication and sensing applications.

Leading companies in this industry include Hoya Corporation, Edmund Optics, CoorsTek, Heraeus Holding, and Corning Incorporated. These players focus on expanding R&D investments, forming cross-industry collaborations, and strengthening their manufacturing capabilities. By innovating in material science and aligning with emerging tech trends, these companies aim to maintain their global leadership and meet evolving customer needs in traditional and disruptive application areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain structure

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries, 2021-2024 (kilo tons)

- 3.3.2 Major importing countries, 2021-2024 (kilo tons)

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing demand for high-performance optical components

- 3.8.1.2 Advancements in photonics and quantum optics

- 3.8.1.3 Increasing applications in telecommunication

- 3.8.1.4 Rising adoption in healthcare and medical devices

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High production costs

- 3.8.2.2 Raw material supply

- 3.8.2.3 Regulatory challenges

- 3.8.1 Growth drivers

- 3.9 Market opportunities

- 3.9.1 Emerging applications in augmented and virtual reality

- 3.9.2 Growing demand for advanced sensing technologies

- 3.9.3 Expansion in autonomous vehicle systems

- 3.9.4 Development of biomimetic optical materials

- 3.10 Growth potential analysis

- 3.11 Regulatory framework analysis

- 3.11.1 Reach and ROHS regulations

- 3.11.2 Export control regulations

- 3.11.3 Environmental compliance requirements

- 3.11.4 Safety standards for handling and processing

- 3.12 Technology landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

- 3.12.3 R&D initiatives and innovation pipeline

- 3.12.4 Patent analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Market share analysis

- 4.2.1 Global market share by manufacturer

- 4.2.2 Regional market share by manufacturer

- 4.3 Competitive benchmarking

- 4.3.1 Product portfolio comparison

- 4.3.2 Technological capabilities comparison

- 4.3.3 R&D investment comparison

- 4.3.4 Manufacturing capacity comparison

- 4.4 Strategic initiatives & developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 Product launches & innovations

- 4.4.4 Expansion plans

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

Chapter 5 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Glass materials

- 5.2.1 Optical glass

- 5.2.2 Fused silica

- 5.2.3 Borosilicate glass

- 5.2.4 Specialty glass

- 5.2.5 Others

- 5.3 Polymeric materials

- 5.3.1 Polymethyl methacrylate (PMMA)

- 5.3.2 Polycarbonate (PC)

- 5.3.3 Cyclic olefin polymer (COP)

- 5.3.4 Cyclic olefin copolymer (COC)

- 5.3.5 Others

- 5.4 Crystalline materials

- 5.4.1 Sapphire

- 5.4.2 Silicon

- 5.4.3 Germanium

- 5.4.4 Zinc selenide

- 5.4.5 Calcium fluoride

- 5.4.6 Others

- 5.5 Ceramic materials

- 5.5.1 Transparent ceramics

- 5.5.2 Aluminum oxynitride (ALON)

- 5.5.3 Magnesium aluminate spinel

- 5.5.4 Yttrium aluminum garnet (YAG)

- 5.5.5 Others

- 5.6 Metallic materials

- 5.6.1 Aluminum

- 5.6.2 Silver

- 5.6.3 Gold

- 5.6.4 Others

- 5.7 Advanced composite materials

- 5.8 Photonic crystals

- 5.9 Metamaterials

- 5.10 Nanomaterials

- 5.11 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Optical components

- 6.2.1 Lenses

- 6.2.2 Mirrors

- 6.2.3 Prisms

- 6.2.4 Windows

- 6.2.5 Filters

- 6.2.6 Diffraction gratings

- 6.2.7 Others

- 6.3 Optoelectronic devices

- 6.3.1 Light emitting diodes (LEDs)

- 6.3.2 Laser diodes

- 6.3.3 Photodetectors

- 6.3.4 Solar cells

- 6.3.5 Optical modulators

- 6.3.6 Others

- 6.4 Imaging systems

- 6.4.1 Cameras

- 6.4.2 Microscopes

- 6.4.3 Telescopes

- 6.4.4 Thermal imaging

- 6.4.5 Others

- 6.5 Optical communication

- 6.5.1 Optical fibers

- 6.5.2 Waveguides

- 6.5.3 Optical amplifiers

- 6.5.4 Optical switches

- 6.5.5 Others

- 6.6 Sensing and measurement

- 6.6.1 Optical sensors

- 6.6.2 Spectroscopy

- 6.6.3 Interferometry

- 6.6.4 Others

- 6.7 Display technologies

- 6.7.1 LCD displays

- 6.7.2 OLED displays

- 6.7.3 AR/VR displays

- 6.7.4 Others

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Consumer electronics

- 7.2.1 Smartphones

- 7.2.2 Cameras

- 7.2.3 Wearable devices

- 7.2.4 Others

- 7.3 Healthcare and medical

- 7.3.1 Diagnostic equipment

- 7.3.2 Surgical devices

- 7.3.3 Therapeutic systems

- 7.3.4 Medical imaging

- 7.3.5 Others

- 7.4 Defense and security

- 7.4.1 Night vision

- 7.4.2 Targeting systems

- 7.4.3 Surveillance

- 7.4.4 Others

- 7.5 Telecommunications

- 7.5.1 Optical networks

- 7.5.2 Data centers

- 7.5.3 5g infrastructure

- 7.5.4 Others

- 7.6 Automotive

- 7.6.1 Lighting systems

- 7.6.2 Heads-up displays

- 7.6.3 Lidar systems

- 7.6.4 Driver assistance systems

- 7.6.5 Others

- 7.7 Aerospace

- 7.7.1 Avionics

- 7.7.2 Navigation systems

- 7.7.3 Satellite components

- 7.7.4 Others

- 7.8 Industrial

- 7.8.1 Machine vision

- 7.8.2 Laser processing

- 7.8.3 Quality control

- 7.8.4 Others

- 7.9 Energy

- 7.9.1 Solar energy

- 7.9.2 Photovoltaics

- 7.9.3 Others

- 7.10 Research and development

- 7.11 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 CoorsTek

- 9.2 Corning Incorporated

- 9.3 Edmund Optics

- 9.4 Heraeus Holding

- 9.5 Hoya Corporation

- 9.6 II-VI Incorporated

- 9.7 Materion Corporation

- 9.8 Newport Corporation

- 9.9 Nikon Corporation

- 9.10 Ohara Corporation

- 9.11 SCHOTT

- 9.12 Sumitomo Electric Industries

- 9.13 Surmet Corporation

- 9.14 Thorlabs

- 9.15 ZEISS Group