|

시장보고서

상품코드

1750337

니티놀 기반 의료기기 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Nitinol-based Medical Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

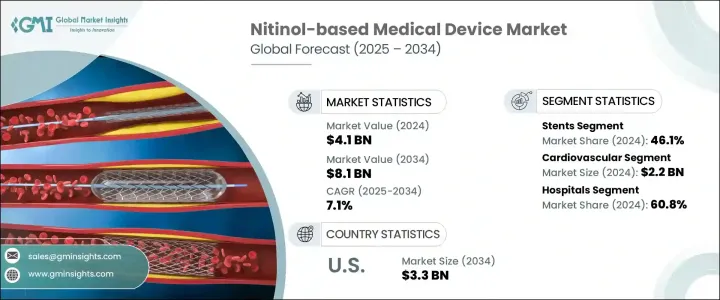

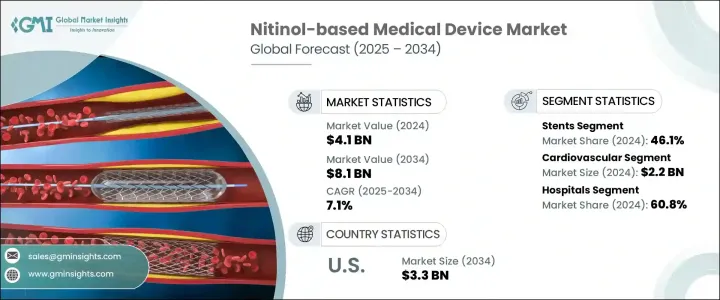

세계의 니티놀 기반 의료기기 시장은 2024년에는 41억 달러로 평가되었고, 고도로 저침습적인 의료 개입이 필요한 심혈관질환, 말초동맥질환, 신경질환 등 만성질환의 유병률 증가에 견인되어 CAGR 7.1%로 성장할 전망이며, 2034년에는 81억 달러에 달할 것으로 예측됩니다.

니티놀은 초탄성과 형상 기억이라는 독특한 특성으로 알려진 니켈 티타늄 합금으로, 환자의 예후를 개선하기 위해 의료기기에 대한 이용이 증가하고 있습니다.

니티놀은 변형 후 소정의 형상으로 돌아가는 능력과 기계적 응력에 대한 내성에 의해 다양한 의료 용도에 이상적입니다. 이러한 특성은 유연성과 내구성이 중요한 스텐트, 가이드 와이어, 정형외과용 임플란트 등의 기기에서 특히 유용합니다. 이 재료의 생체적합성 및 내식성은 장기적인 이식에 대한 적성을 더욱 높여줍니다. 이러한 특성에 의해 니티놀제 기구는 장기간에 걸쳐 인체 내에서 기능성과 구조적 무결성을 유지하고, 거부반응이나 열화의 위험을 줄입니다. 이 신뢰성으로 니티놀은 심장혈관, 신경혈관, 정형외과 치료에 사용되는 영구 임플란트로 선호되는 선택지가 되고 있습니다. 저침습 처치 수요가 높아짐에 따라 니티놀 기반 기기의 채택이 증가하여 시장 확대에 기여할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 41억 달러 |

| 예측 금액 | 81억 달러 |

| CAGR | 7.1% |

2024년 병원 부문의 점유율은 60.8%로, 수술 시간 단축, 환자 외상 최소화, 회복 결과 개선을 목적으로 하는 선진 의료기기의 도입이 증가하고 있는 것이 배경에 있습니다. 스텐트, 가이드 와이어, 필터, 정형외과용 임플란트 등 니티놀을 기반으로 하는 기기는 형상 기억이나 초탄성 등의 독자적인 특성으로 인해 병원에 필수적인 것이 되고 있습니다. 특히 심장혈관이나 신경혈관의 손기술에서 복잡한 해부학적 구조를 탐색하는 스텐트의 뛰어난 성능은 손기술의 성공률 향상과 입원기간 단축으로 이어집니다.

2024년에는 혈관장애의 유병률 상승 및 니티놀 스텐트가 제공하는 임상적 이점에 힘입어 스텐트 부문은 46.1%의 점유율로 최고 자리를 유지했습니다. 이 스텐트들은 특히 말초동맥질환 및 관상동맥폐색 환자에서 자기확장성과 복잡한 혈관경로에 심리스에 적합한 능력을 평가받고 있습니다. 특히 말초동맥질환이나 관상동맥폐색 환자에서 이러한 스텐트는 복잡한 혈관 경로에 원활하게 적합한 능력을 평가받고 있습니다. 헬스케어 공급자가 동맥 질환 관리를 위해 저침습성으로 효과가 높은 치료 옵션을 우선시하고 있기 때문에 수요는 계속 증가하고 있습니다.

북미의 니티놀 기반 의료기기 2024년 시장 점유율은 40%를 차지했는데, 이는 이 지역의 견고한 헬스케어 인프라, 확립된 상환 제도, 선진 의료 기술의 조기 도입에 기인하고 있습니다. 선도적인 제조업체의 존재와 병원 및 전문 클리닉에서 니티놀 기반 기기의 광범위한 임상 통합은 급속하게 진화하는이 의료기기 분야에서 북미의 아성을 더욱 견고하게 만듭니다.

세계의 니티놀 기반 의료기기 업계의 주요 기업은 Boston Scientific Corporation, Medtronic plc, Abbott Laboratories, Terumo Corporation, B. Braun Melsungen AG 등이 있습니다. 이 회사는 니티놀 기반 기기의 혁신 및 성능을 향상시키기 위한 연구개발에 주력하고 있습니다. 전략적 제휴, 합병, 인수는, 각사가 제품 포트폴리오와 시장 범위의 확대를 목표로 하는 가운데 일반적으로 행해지고 있습니다. 시장 포지션을 강화하기 위해 니티놀 기반 의료기기 업계의 기업들은 몇 가지 중요한 전략을 채택하고 있습니다. 여기에는 니티놀을 기반으로 한 기기의 혁신 및 성능 향상을 위한 연구 개발에 대한 투자가 포함됩니다. 전략적 제휴, 합병, 인수는 기업이 제품 포트폴리오와 시장 리치를 확대하는 것을 목적으로 하고 있기 때문에 일반적입니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 저침습 수술 수요 증가

- 심혈관 질환 및 정형외과 질환 유병률의 상승

- 의료기기 제조에서 기술의 진보

- 세계적으로 고령화 진행

- 업계의 잠재적 위험 및 과제

- 니티놀 기반 기기의 고비용

- 엄격한 규제 승인 프로세스

- 성장 촉진요인

- 성장 가능성 분석

- 트럼프 정권의 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망 및 향후의 검토 사항 트럼프 정권의 관세

- 무역에 미치는 영향

- 기술의 상황

- 장래 시장 동향

- 규제 상황

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 경쟁 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 스텐트

- 가이드와이어

- 카테터

- 기타 제품

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 심혈관계

- 정형외과

- 치과

- 신경학적

- 비뇨기과

- 기타 용도

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 연구 및 학술기관

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 일본

- 중국

- 인도

- 호주

- 한국

- 라틴아메리카

- 멕시코

- 브라질

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott Laboratories

- Acandis

- Admedes Schuessler

- Arthrex

- B Braun

- Becton, Dickinson and Company

- Biotronik

- Boston Scientific

- Cook Medical

- Endosmart

- Jotec

- Medtronic

- MicroPort

- Stryker

- Terumo

The Global Nitinol-based Medical Device Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 8.1 billion by 2034 driven by the increasing prevalence of chronic diseases such as cardiovascular conditions, peripheral artery disease, and neurological disorders, which necessitate advanced, minimally invasive medical interventions. Nitinol, a nickel-titanium alloy known for its unique properties of superelasticity and shape memory, is increasingly utilized in medical devices to improve patient outcomes.

Nitinol's ability to return to a predetermined shape after deformation and its resistance to mechanical stress make it ideal for various medical applications. These properties are particularly beneficial in devices like stents, guidewires, and orthopedic implants, where flexibility and durability are crucial. The material's biocompatibility and corrosion resistance further enhance its suitability for long-term implantation. These properties ensure that nitinol devices maintain their functionality and structural integrity within the human body over extended periods, reducing the risk of rejection or degradation. This reliability makes nitinol a preferred choice for permanent implants used in cardiovascular, neurovascular, and orthopedic treatments. As the demand for minimally invasive procedures grows, the adoption of nitinol-based devices is expected to rise, contributing to the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $8.1 Billion |

| CAGR | 7.1% |

The hospital segment held a 60.8% share in 2024, driven by the increasing incorporation of advanced medical devices aimed at reducing operative time, minimizing patient trauma, and improving recovery outcomes. Nitinol-based devices-such as stents, guidewires, filters, and orthopedic implants-have become integral to hospitals due to their unique properties like shape memory and super-elasticity, which are critical in minimally invasive interventions. Their superior performance in navigating complex anatomies, particularly during cardiovascular and neurovascular procedures, translates into higher procedural success rates and reduced length of hospital stays.

In 2024, the stents segment maintained its leading position with a 46.1% share, fueled by the rising prevalence of vascular disorders and the clinical advantages provided by nitinol stents. These stents are valued for their self-expanding properties and ability to conform seamlessly to complex vascular pathways, especially in patients with peripheral artery disease or coronary blockages. The demand continues to rise as healthcare providers prioritize less invasive, highly effective treatment options for managing arterial conditions.

North America Nitinol-based Medical Device Market held 40% share in 2024, attributed to the region's robust healthcare infrastructure, well-established reimbursement systems, and early adoption of advanced medical technologies. The presence of leading manufacturers and widespread clinical integration of nitinol-based tools in hospitals and specialty clinics has further reinforced North America's stronghold in this rapidly evolving medical device space.

Key players in the Global Nitinol-Based Medical Device Industry include Boston Scientific Corporation, Medtronic plc, Abbott Laboratories, Terumo Corporation, and B. Braun Melsungen AG. These companies are focusing on research and development to innovate and enhance the performance of nitinol-based devices. Strategic collaborations, mergers, and acquisitions are common as companies aim to expand their product portfolios and market reach. To strengthen their market position, companies in the nitinol-based medical device industry are adopting several key strategies. These include investing in research and development to innovate and improve the performance of nitinol-based devices. Strategic collaborations, mergers, and acquisitions are common as companies aim to expand their product portfolios and market reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for minimally invasive surgeries

- 3.2.1.2 Rising prevalence of cardiovascular and orthopedic disorders

- 3.2.1.3 Technological advancements in medical device manufacturing

- 3.2.1.4 Growing geriatric population globally

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of nitinol-based devices

- 3.2.2.2 Stringent regulatory approval processes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerationsTrump administration tariffs

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Stents

- 5.3 Guidewires

- 5.4 Catheters

- 5.5 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiovascular

- 6.3 Orthopedic

- 6.4 Dental

- 6.5 Neurological

- 6.6 Urology

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Research and academic institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Acandis

- 9.3 Admedes Schuessler

- 9.4 Arthrex

- 9.5 B Braun

- 9.6 Becton, Dickinson and Company

- 9.7 Biotronik

- 9.8 Boston Scientific

- 9.9 Cook Medical

- 9.10 Endosmart

- 9.11 Jotec

- 9.12 Medtronic

- 9.13 MicroPort

- 9.14 Stryker

- 9.15 Terumo