|

시장보고서

상품코드

1750434

바이오 숙신산 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Bio-Succinic Acid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

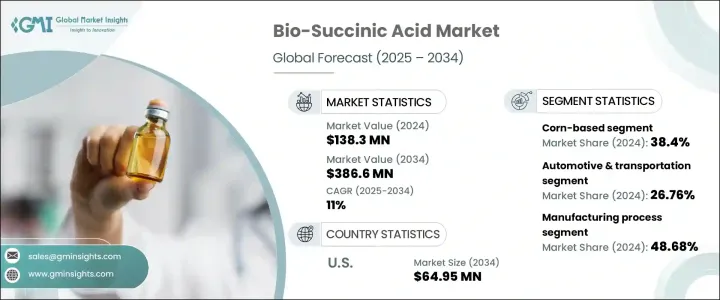

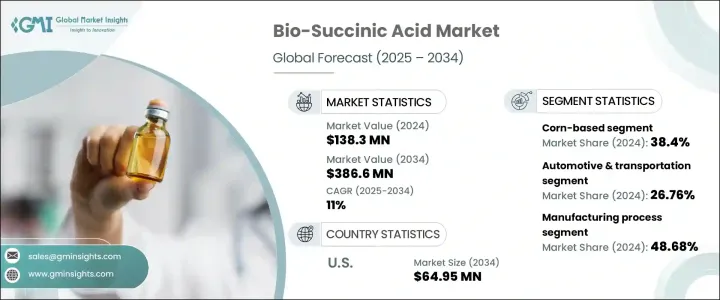

세계의 바이오 숙신산 시장은 2024년에는 1억 3,830만 달러가 되고, 2034년에는 CAGR 11%로 성장해 3억 8,660만 달러에 이를 것으로 추정되고 있습니다.

산업계도 정부도 환경 친화적인 해결책을 중시하는 가운데, 바이오 숙신산은 다양한 용도로 재생 가능하고 생분해성의 선택지를 제공하는 그린 제품으로서 지지를 모으고 있습니다.

바이오 숙신산은 바이오베이스 폴리머를 제조할 때 중요한 구성 요소이기 때문에 다양한 산업에서 지속 가능한 재료로의 이동이 진행되고 있는 것이 바이오 숙신산 수요를 크게 밀어 올리고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1억 3,830만 달러 |

| 예측 금액 | 3억 8,660만 달러 |

| CAGR | 11% |

옥수수 분야의 바이오 숙신산 시장은 2024년 38.4%의 점유율을 차지했습니다. 힘에 의해 대규모 생산에 바람직한 원료가 되고 있습니다. 옥수수를 원료로 하는 바이오 숙신산의 채용이 확대되고 있는 것은 그 확립된 공급 체인과 발효 기술의 확장성에 의한 것입니다.

발효 기반 공정 부문은 비용 효율성과 재생가능한 원료에 대한 의존성으로 인해 49%의 점유율을 차지하고 있습니다. 화학 촉매도 주목받고 있지만, 비용이 높고 환경에 대한 영향도 우려되기 때문에 보급에는 한계가 있습니다.

미국 바이오 숙신산 미국 시장은 2024년에 2,238만 달러를 창출해 2034년에는 6,495만 달러에 이를 것으로 예측되고 있습니다.

바이오 숙신산 세계 시장의 주요 기업은 Corbion N.V., Kawasaki Kasei Chemicals, BASF SE, Mitsui & Co., Ltd., Reverdia 등입니다. Corbion NV와 Reverdia는 수율을 최적화하고 비용을 절감하기 위해 고도의 발효 프로세스를 활용하고 있으며, Mitsui & Co., Ltd.은 생산에 농업 폐기물과 같은 재생 가능 원료의 사용을 모색하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

참고: 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

- 이익률 분석

- 규제 상황

- 영향요인

- 성장 촉진요인

- 바이오의 화학 물질과 지속 가능한 대체품에 대한 수요 증가

- 지속가능하고 환경친화적인 제품에 대한 소비자의 강한 취향

- 환경 친화적인 생분해 성 제품을 촉진하는 정부 규제

- 업계의 잠재적 위험 및 과제

- 석유 유래의 대체품에 비해 생산 비용이 높습니다.

- 원재료의 입수가 한정되어 있어, 확장성에 영향을 주고 있습니다.

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장추계 및 예측 : 원재료별, 2021-2034년

- 주요 동향

- 옥수수 베이스

- 사탕수수 베이스

- 카사바 베이스

- 리그노셀룰로오스계 바이오매스(목재, 농업 폐기물 등)

- 기타(조류, 미생물 발효 등)

제6장 시장 추계 및 예측 : 최종 이용 산업별, 2021-2034년

- 주요 동향

- 자동차 및 운송

- 포장업계

- 섬유산업

- 건설 및 인프라

- 소비재

- 헬스케어 및 의약품

- 농업

- 에너지 부문

제7장 시장 추계 및 예측 : 제조 공정별, 2021-2034년

- 주요 동향

- 발효 기반 생산

- 포도당과 당에서 직접 합성

- 화학촉매

- 하이브리드 공정(발효와 촉매의 조합)

제8장 시장추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- AHB Global

- BASF SE

- Corbion NV

- Kawasaki Kasei Chemicals

- Mitsubishi Chemical Corporation

- Mitsui &Co., Ltd

- Myriant Corporation

- Nippon Shokubai

- Reverdia

- Roquette Freres

The Global Bio-Succinic Acid Market was valued at USD 138.3 million in 2024 and is estimated to grow at a CAGR of 11% to reach USD 386.6 million by 2034, driven by a rising consumer demand for sustainable, bio-based chemical alternatives to traditional petroleum-based products. As industries and governments alike focus on eco-friendly solutions, bio-succinic acid has gained traction as a green product, offering a renewable and biodegradable option in various applications. The increased emphasis on sustainability, coupled with stricter regulations on environmental impact, has made bio-succinic acid a key player in the chemical industry.

The increasing shift towards sustainable materials in various industries has significantly bolstered the demand for bio-succinic acid, as it is a key building block in the production of bio-based polymers. Among these polymers, polybutylene succinate (PBS) stands out due to its biodegradability, versatility, and potential to replace petroleum-based plastics in numerous applications. This surge in demand for PBS is driving the need for bio-succinic acid, as it is used in the production of PBS and other environmentally friendly polymers, further expanding the market for bio-succinic acid.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $138.3 Million |

| Forecast Value | $386.6 Million |

| CAGR | 11% |

The bio-succinic acid market from the corn segment held 38.4% share in 2024. Corn, being a carbohydrate-rich resource, is particularly well-suited for fermentation-based processes that yield bio-succinic acid. Its availability, cost-effectiveness, and ability to provide a consistent and reliable supply make it a preferred feedstock for large-scale production. The growing adoption of corn-based bio-succinic acid is driven by its established supply chain and the scalability of fermentation technologies. As demand for bio-succinic acid grows, alternative feedstocks are also being explored.

The fermentation-based process segment held 49% share due to its cost-effectiveness and reliance on renewable feedstocks. This method allows for scalable production with reduced environmental impact, making it the preferred choice for large-scale manufacturing. However, new approaches, such as direct synthesis from glucose and sugars, are emerging, offering higher yields under controlled conditions. Chemical catalysis is also gaining attention, although its higher costs and environmental concerns limit its widespread application. The hybrid process, combining fermentation and catalysis, is being explored as a solution to improve production efficiency and sustainability while balancing cost.

U.S Bio-Succinic Acid Market generated USD 22.38 million in 2024, with projections to reach USD 64.95 million by 2034, attributed to government incentives supporting bio-based chemicals and the growing industrial demand for renewable resources. The U.S. is a major producer of bio-succinic acid, benefiting from an advanced manufacturing infrastructure and strong governmental support for green technologies.

Key players in the Global Bio-Succinic Acid Market include Corbion N.V., Kawasaki Kasei Chemicals, BASF SE, Mitsui & Co., Ltd., and Reverdia. Companies are focusing on expanding their product portfolios, improving production efficiency, and exploring new raw materials to enhance their market share. For instance, Corbion N.V. and Reverdia have been leveraging advanced fermentation processes to optimize yields and reduce costs, while Mitsui & Co., Ltd. is exploring the use of renewable raw materials like agricultural waste for production. By adopting these strategies, these companies are positioning themselves to capitalize on the growing demand for bio-succinic acid as industries move toward more sustainable solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.3 Supply-side impact (raw materials)

- 3.2.3.1 Price volatility in key materials

- 3.2.3.2 Supply chain restructuring

- 3.2.3.3 Production cost implications

- 3.2.4 Demand-side impact (selling price)

- 3.2.4.1 Price transmission to end markets

- 3.2.4.2 Market share dynamics

- 3.2.4.3 Consumer response patterns

- 3.2.5 Key companies impacted

- 3.2.6 Strategic Industry Responses

- 3.2.6.1 Supply Chain Reconfiguration

- 3.2.6.2 Pricing and Product Strategies

- 3.2.6.3 Policy Engagement

- 3.2.7 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major Exporting Countries

- 3.3.2 Major Importing Countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for bio-based chemicals and sustainable alternatives

- 3.6.1.2 Strong consumer preference for sustainable and green products

- 3.6.1.3 Government regulations promoting eco-friendly and biodegradable products

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs compared to petroleum-based alternatives

- 3.6.2.2 Limited availability of raw materials, affecting scalability

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Raw Material Source, 2021 – 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Corn-based

- 5.3 Sugarcane-based

- 5.4 Cassava-based

- 5.5 Lignocellulosic biomass (wood, agricultural waste, etc.)

- 5.6 Others (algae, microbial fermentation, etc.)

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Automotive & transportation

- 6.3 Packaging industry

- 6.4 Textile industry

- 6.5 Construction & infrastructure

- 6.6 Consumer goods

- 6.7 Healthcare & pharmaceuticals

- 6.8 Agriculture

- 6.9 Energy sector

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 – 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Fermentation-based production

- 7.3 Direct synthesis from glucose & sugars

- 7.4 Chemical catalysis

- 7.5 Hybrid process (combination of fermentation & catalysis)

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AHB Global

- 9.2 BASF SE

- 9.3 Corbion N.V.

- 9.4 Kawasaki Kasei Chemicals

- 9.5 Mitsubishi Chemical Corporation

- 9.6 Mitsui & Co., Ltd

- 9.7 Myriant Corporation

- 9.8 Nippon Shokubai

- 9.9 Reverdia

- 9.10 Roquette Freres