|

시장보고서

상품코드

1750471

HVAC 밸브 시장 기회와 촉진요인, 업계 동향 분석 및 예측(2025-2034년)HVAC Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

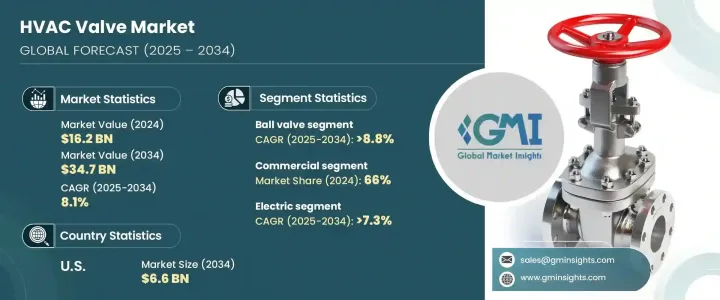

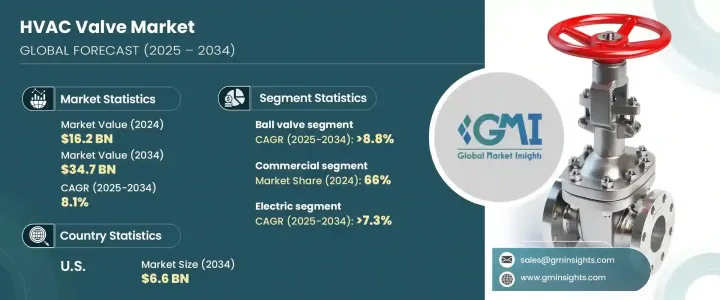

세계의 HVAC 밸브 시장은 2024년에 162억 달러로 평가되었고 전 세계적으로 건설 활동이 급증하면서 주거, 상업 및 산업 부문에서 난방, 환기 및 공조(HVAC) 시스템에 대한 수요가 증가함에 따라 2034년에는 347억 달러에 이를 것으로 예측되며, CAGR 8.1%로 성장할 전망입니다.

밸브는 유체 흐름, 압력 및 온도를 조절하여 최적의 성능과 에너지 효율을 보장함으로써 이러한 시스템에서 중요한 역할을 합니다.

에너지 효율이 높고 스마트한 건물에 대한 동향이 HVAC 밸브 시장을 견인하고 있습니다. 새로운 건축물에는 실시간 모니터링 및 제어를 위한 센서, 연결성 및 분석 기능을 갖춘 지능형 밸브가 장착된 첨단 HVAC 시스템이 통합되어 있습니다. 이러한 스마트 밸브를 통해 시설 관리자는 에너지 소비를 최적화하고, 오류를 조기에 감지하고, 예측 유지보수를 수행하여 운영 비용을 절감하고 장비 수명을 연장할 수 있습니다. IoT 기술을 HVAC 시스템에 통합하는 것은 자동화 및 지능형 밸브 솔루션에 대한 수요를 가속화하고 있습니다. 이러한 스마트 밸브는 실시간 모니터링, 원격 액세스, 고급 제어 기능을 제공하여 시설 관리자가 에너지 사용을 최적화하고 시스템 응답성을 개선할 수 있도록 합니다. 상업용 및 산업용 건물이 스마트 빌딩 프레임워크를 점점 더 채택함에 따라 빌딩 관리 시스템(BMS)과 원활하게 통신할 수 있는 밸브에 대한 수요가 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 162억 달러 |

| 예측 금액 | 347억 달러 |

| CAGR | 8.1% |

2024년 기준 볼 밸브는 HVAC 밸브 시장에서 4.3%의 상당한 점유율을 차지했습니다. 이들의 인기는 단순한 구조, 밀폐 성능, HVAC 시스템의 공기 및 유체 흐름 관리에 적합한 특성에서 비롯됩니다. 볼 밸브는 낮은 토크 작동, 밀폐성, 높은 내구성을 갖추어 난방 및 냉각 응용 분야의 효율성과 무균성을 향상시키기 때문에 신규 설치 및 리모델링 프로젝트에서 널리 사용됩니다. 또한 볼 밸브는 자동화 기술과 호환되어 스마트 HVAC 시스템과 호환됩니다.

2024년 HVAC 밸브 시장에서는 상업 부문이 66%의 점유율을 차지하며 주도했습니다. 사무실, 쇼핑몰, 병원, 호텔, 데이터 센터 및 학교와 같은 상업용 건물에는 유체 및 공기 흐름을 정확하게 조절하기 위해 복잡한 HVAC 시스템이 필요합니다. 이러한 건물에 스마트하고 에너지 효율적인 HVAC 시스템이 채택되는 것은 정부 표준을 준수하고, 비용을 절감하며, LEED와 같은 친환경 인증을 획득해야 하는 필요성에 의해 촉진되고 있습니다. 이러한 동향은 정밀한 제어 및 건물 관리 시스템과의 통합을 제공하는 첨단 HVAC 밸브에 대한 수요를 촉진하고 있습니다.

미국의 HVAC 밸브 시장은 2024년에 67%의 점유율을 차지했으며, Energy Star 프로그램 및 캐나다의 에너지 효율 규정과 같은 엄격한 에너지 효율 규정 및 지속 가능성 이니셔티브에 힘입어 2034년에는 66억 달러를 달성할 것으로 예상됩니다. 이러한 규정은 에너지 절약 및 환경 기준 준수를 위해 지능형 및 IoT 기반 밸브를 포함한 효율적인 HVAC 시스템의 채택을 장려하고 있습니다. 지역 내 스마트 빌딩과자율화 기술에 대한 관심은 빌딩 관리 시스템(BMS) 호환형 HVAC 밸브 수요를 더욱 촉진하고 있습니다. 또한, 기존 HVAC 시스템의 개조 작업이 기존 건물에서 진행되면서 고급 밸브 솔루션에 대한 수요가 증가하고 있습니다.

세계의 HVAC 밸브 산업의 주요 기업에는 Honeywell, Johnson Controls, Schneider Electric, Siemens, Belimo, Danfoss, Pentair, AVK, Flowserve, Mueller Industries, Samson, Taco, Bray, Nexus, 및 IDC가 포함됩니다. 이들 기업은 제품 혁신, 전략적 파트너십, 합병 및 인수합병을 통해 시장 지위를 강화하는 데 집중하고 있습니다. 선도적인 제조업체들은 스마트 기능과 향상된 성능을 갖춘 고급 HVAC 밸브 개발을 핵심 전략으로 삼고 있습니다. 또한 기업들은 지속 가능한 HVAC 시스템에 대한 수요 증가를 충족하기 위해 친환경적이고 에너지 효율적인 솔루션 개발을 위해 연구 개발에 투자하고 있습니다.

HVAC 밸브 산업의 기업들은 시장 점유율을 강화하기 위해 여러 핵심 전략을 채택하고 있습니다. 이는 혁신과 기술 발전을 통해 제품 포트폴리오를 확장하는 것을 포함하며, 고객의 변화하는 요구사항을 충족하기 위해 새로운 밸브 디자인과 기능을 도입하는 것이 포함됩니다. IoT 및 자동화와 같은 스마트 기술의 통합은 시장에서 중요한 트렌드로, 제조업체는 실시간 모니터링 및 제어 기능을 갖춘 첨단 솔루션을 제공할 수 있게 되었습니다. 기술 공급업체, HVAC 시스템 제조업체 및 유통업체와의 전략적 파트너십 및 협력을 통해 기업은 제품군을 강화하고 더 광범위한 고객층에 도달할 수 있습니다. 또한, 합병 및 인수는 시장 통합과 새로운 시장 및 기술에 대한 접근을 위한 일반적인 전략입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 제조업자

- 원재료 공급업체

- 유통 채널

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(고객에 대한 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 이익률 분석

- 기술과 혁신의 상황

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 성장하는 건설 업계

- 도시화와 스마트 시티의 대처

- 기후 변화와 이상기상

- 업계의 잠재적 위험 및 과제

- 초기 비용이 높아

- 신흥 시장에서의 인지도가 낮은

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 산업 구조와 집중

- 경쟁 강도 평가

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 제품의 위치 지정

- 가격 성능비 포지셔닝

- 지리적 존재

- 혁신 능력

- 전략적 대시보드

- 경쟁 벤치마킹

- 제조능력

- 제품 포트폴리오의 강도

- 유통 네트워크

- R&D 투자

- 전략적 노력의 평가

- 주요 기업의 SWOT 분석

- 미래 경쟁 전망

제5장 시장 추계 및 예측 : 밸브 유형별(2024-2034년)

- 주요 동향

- 볼 밸브

- 글로브 밸브

- 나비 밸브

- 체크 밸브

- 게이트 밸브

- 압력 릴리프 밸브

- 제어 밸브

- 솔레노이드 밸브

- 기타

제6장 시장 추계 및 예측 : 운영 유형별(2024-2034년)

- 주요 동향

- 매뉴얼

- 공압

- 유압식

- 전기

- 스마트 및 커넥티드

제7장 시장 추계 및 예측 : 용도별(2024-2034년)

- 주요 동향

- 난방 시스템

- 냉각 시스템

- 환기 시스템

- 지역 냉방

- 냉동

제8장 시장 추계 및 예측 : 최종 용도별(2024-2034년)

- 주요 동향

- 주거용

- 상업용

- 오피스 빌딩

- 소매

- 접객업

- 의료

- 교육

- 기타

- 산업

- 석유 및 가스

- 제조업

- 식품 및 음료

- 의약품

- 기타

제9장 시장 추계 및 예측 : 지역별(2024-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- AVK

- Belimo

- Bray

- Danfoss

- Flowserve

- Honeywell

- IDC

- Johnson Controls

- Mueller Industries

- Nexus

- Pentair

- Samson

- Schneider Electric

- Siemens

The Global HVAC Valve Market was valued at USD 16.2 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 34.7 billion by 2034 driven by the surge in construction activities worldwide, leading to increased demand for heating, ventilation, and air conditioning (HVAC) systems across residential, commercial, and industrial sectors. Valves play a crucial role in these systems by regulating fluid flow, pressure, and temperature, ensuring optimal performance and energy efficiency.

The trend toward energy-efficient and smart buildings is propelling the HVAC valve market. New constructions incorporate advanced HVAC systems with intelligent valves featuring sensors, connectivity, and analytics for real-time monitoring and control. These smart valves enable facility managers to optimize energy consumption, detect faults early, and perform predictive maintenance, reducing operational costs and extending equipment lifespan. Integrating Internet of Things (IoT) technology into HVAC systems accelerates the demand for automated and intelligent valve solutions. These smart valves offer real-time monitoring, remote access, and advanced control capabilities, allowing facility managers to optimize energy usage and improve system responsiveness. As commercial and industrial buildings increasingly adopt smart building frameworks, the need for valves that seamlessly communicate with Building Management Systems (BMS) is rising.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.2 Billion |

| Forecast Value | $34.7 Billion |

| CAGR | 8.1% |

In 2024, ball valves held a significant share of the HVAC valve market, accounting for 4.3%. Their popularity is attributed to their simple structure, tight shut-off action, and suitability for airflow and fluid flow management in HVAC systems. Ball valves are widely used in new installations and retrofitting projects due to their low torque operation, close seal, and high durability, which contribute to the efficiency and asepsis of heating and cooling applications. Additionally, ball valves support automation technologies, making them compatible with smart HVAC systems.

The commercial sector dominated the HVAC valve market in 2024, representing a 66% share. Commercial buildings such as offices, shopping malls, hospitals, hotels, data centers, and schools require complex HVAC systems to regulate fluid and air flow accurately. The adoption of smart and energy-efficient HVAC systems in these buildings is driven by the need to comply with government standards, reduce costs, and achieve green certifications like LEED. This trend fuels the demand for advanced HVAC valves that offer precise control and integration with building management systems.

United States HVAC Valve Market held a 67% share in 2024 and is projected to generate USD 6.6 billion by 2034, driven by stringent energy efficiency regulations and sustainability initiatives, such as the Energy Star program and Canada's Energy Efficiency Regulations. These regulations are encouraging the adoption of efficient HVAC systems, including intelligent and IoT-based valves, to conserve energy and comply with environmental standards. The focus on smart buildings and automation in the region further supports the demand for Building Management System (BMS)-compatible HVAC valves. Additionally, the retrofitting of existing HVAC systems in older buildings is contributing to the increased demand for advanced valve solutions.

Key players in the Global HVAC Valve Industry include Honeywell, Johnson Controls, Schneider Electric, Siemens, Belimo, Danfoss, Pentair, AVK, Flowserve, Mueller Industries, Samson, Taco, Bray, Nexus, and IDC. These companies focus on product innovation, strategic partnerships, and mergers and acquisitions to strengthen their market presence. Developing advanced HVAC valves with smart features and enhanced performance is a key focus area for leading manufacturers. Additionally, companies are investing in research and development to develop eco-friendly and energy-efficient solutions to meet the growing demand for sustainable HVAC systems.

To strengthen their market presence, companies in the HVAC valve industry are adopting several key strategies. These include expanding their product portfolios through innovation and technological advancements, such as introducing new valve designs and features to cater to the evolving needs of customers. Integrating smart technologies, such as IoT and automation, is a significant trend in the market, enabling manufacturers to offer advanced solutions with real-time monitoring and control capabilities. Strategic partnerships and collaborations with technology providers, HVAC system manufacturers, and distributors enable companies to enhance their product offerings and reach a broader customer base. Additionally, mergers and acquisitions are common strategies for market consolidation and gaining access to new markets and technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Distribution channel

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact on forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growing construction industry

- 3.8.1.2 Urbanization and smart city initiatives

- 3.8.1.3 Climate change and weather extremes

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial costs

- 3.8.2.2 Limited awareness in emerging markets

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Industry structure and concentration

- 4.2.1 Competitive intensity assessment

- 4.2.2 Company market share analysis

- 4.2.3 Competitive positioning matrix

- 4.3 Product positioning

- 4.3.1 Price-performance positioning

- 4.3.2 Geographic presence

- 4.3.3 Innovation capabilities

- 4.4 Strategic dashboard

- 4.5 Competitive benchmarking

- 4.5.1 Manufacturing capabilities

- 4.5.2 Product portfolio strength

- 4.5.3 Distribution network

- 4.5.4 R&D investments

- 4.6 Strategic initiatives assessment

- 4.7 SWOT analysis of key players

- 4.8 Future competitive outlook

Chapter 5 Market Estimates & Forecast, By Valve Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Ball valves

- 5.3 Globe valves

- 5.4 Butterfly valves

- 5.5 Check valves

- 5.6 Gate valves

- 5.7 Pressure relief valves

- 5.8 Control valves

- 5.9 Solenoid valves

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Operation Type, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manual

- 6.3 Pneumatic

- 6.4 Hydraulic

- 6.5 Electric

- 6.6 Smart/connected

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Heating systems

- 7.3 Cooling systems

- 7.4 Ventilation systems

- 7.5 district cooling

- 7.6 Refrigeration

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Office buildings

- 8.3.2 Retail

- 8.3.3 hospitality

- 8.3.4 Healthcare

- 8.3.5 Educational institute

- 8.3.6 Others

- 8.4 Industrial

- 8.4.1 Oil and gas

- 8.4.2 Manufacturing

- 8.4.3 Food and beverage

- 8.4.4 Pharmaceuticals

- 8.4.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AVK

- 10.2 Belimo

- 10.3 Bray

- 10.4 Danfoss

- 10.5 Flowserve

- 10.6 Honeywell

- 10.7 IDC

- 10.8 Johnson Controls

- 10.9 Mueller Industries

- 10.10 Nexus

- 10.11 Pentair

- 10.12 Samson

- 10.13 Schneider Electric

- 10.14 Siemens