|

시장보고서

상품코드

1750490

금속 마개 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Metal Closures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

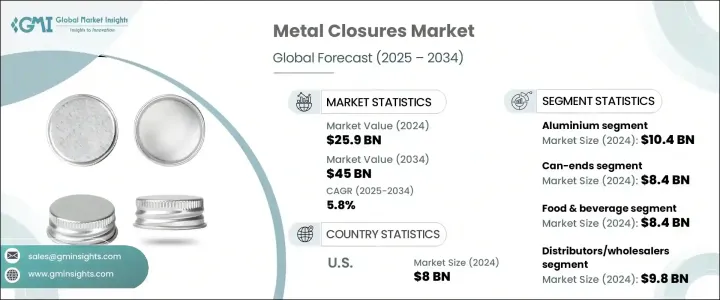

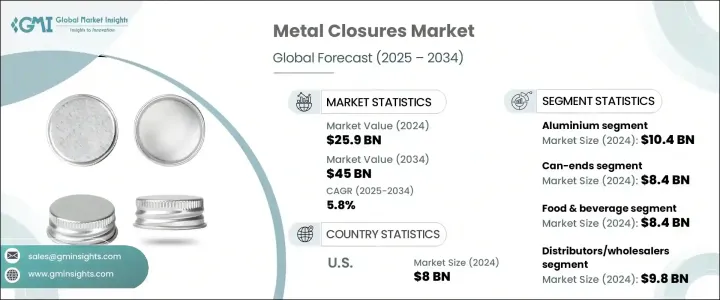

세계의 금속 마개 시장 규모는 2024년에 259억 달러로 평가되었고, CAGR 5.8%를 나타내, 2034년까지는 450억 달러에 이를 것으로 추정됩니다. 신흥 경제국가 모두에서 알코올 음료의 소비가 증가하고 있는 것 외에도 식품 및 음료에 대한 수요가 증가하고 있는 것입니다. 변조되지 않은 포장 솔루션에 대한 요구가 크게 증가하고 금속 마개 채택에 박차를 가하고 있습니다. 포장 노력을 지원하는 능력을 가지고 있기 때문에 지지되고 있습니다. 최근, 시장 관계자는 환경 친화적인 기능을 도입해, 재활용 가능한 재료를 우선하는 것으로, 진화하는 규제와 소비자의 기대에 부응하고 있습니다.

트럼프 정권 하에서 수입 알루미늄과 철강에 관세가 부과된 것은 업계에 큰 영향을 미쳤습니다. 일부 지역 금속 제조업체는 일시적인 가격 이점을 얻었지만 업계 전반에 걸쳐 변동성 증가와 운영 비용 상승을 해결했습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 259억 달러 |

| 예측 금액 | 450억 달러 |

| CAGR | 5.8% |

재료별로는 알루미늄, 스틸, 주석 등으로 구분됩니다. 이 재료는 내부식성과 산성 제품에의 적합성으로 특히 선호되고 있습니다.

제품 유형별로 크라운, 캔 엔드, 스크류, 트위스트 및 기타 마개가 있습니다. 이러한 마개는 뛰어난 밀봉 성능을 발휘하므로 신선도 유지와 오염 방지에 이상적입니다.

금속 마개 시장은 최종 용도에 근거해, 퍼스널케어 및 화장품, 식품 및 음료, 소비재, 의약품, 기타로 나눌 수 있습니다. 식품 및 음료 분야는 2024년에 84억 달러의 평가액으로 시장을 리드했습니다. 가공 식품에 있어서의 밀폐 용기의 보급 등이, 수요를 촉진하는 데 중요한 역할을 하고 있습니다. 금속 마개는 내용물을 습기나 산소로부터 보호하는 배리어 특성을 제공해, 특히 탄산 음료나 발효 음료의 보존 기간의 연장과 품질 유지에 공헌하고 있습니다.

유통 채널에 관해서는 시장은 직접 판매, 유통업체·도매업체, 소매업체로 구분됩니다. 따라서 대량 구매가 신뢰할 수 있는 공급망의 연속성을 보장하고 있기 때문에 이러한 판매자는 종종 유연한 주문 크기와 맞춤형 옵션으로 중견 기업을 수용할 수 있으며 틈새 시장 및 특수 포장 요구 사항을 충족할 수 있습니다.

미국은 2024년에 80억 달러로 최대의 지역 점유율을 차지했습니다. 컴플라이언스와 소비자의 안전을 위해 점점 더 중요해지고 있습니다.

금속 마개 산업의 경쟁은 치열하며 세계 제조업체와 지역 제조업체도 존재합니다. 상위 3개 회사인 Silgan Holdings Inc. Crown Holdings Inc. Guala Closures Group은 2024년에 합쳐 12.8% 이상 시장 점유율을 차지했습니다. 대기업은 연구개발에 계속 투자해 경량재료, 재활용성 향상, 혁신적인 밀봉기구에 초점을 맞춘 차세대 제품을 발표하고 있습니다. QR 코드나 NFC 칩을 탑재한 스마트 마개 등의 기능은 기업이 소비자의 관여, 추적 가능성, 제품의 안전성을 높이려고 하고 있기 때문에 기세를 늘리고 있습니다. 게다가, 건강 지향과 추적성을 중시하는 포장의 중요성이 높아지고 있기 때문에 제조업체는 BPA-NI 라이닝이나 하이 배리어 기술 등의 기능을 갖춘 마개의 개발을 촉구하고 있습니다. 또, 온라인 소매, 소비자 직접 판매 브랜드, 공예품 제조의 인기가 각 업계에서 높아지고 있는 것도, 기능성과 미적 매력을 겸비한 커스터마이즈 가능한 소롯트 대응의 마개의 필요성을 높여지고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 포장 식품 및 음료 수요 증가

- 활황을 나타내는 제약 업계

- 알코올 음료의 소비량 증가

- 긴 보존 기간과 밀폐성

- 지속가능성과 재활용성의 매력

- 업계의 잠재적 리스크 및 과제

- 원재료 가격 변동

- 경량 연포장에 대한 대체

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 재료별(2021-2034년)

- 주요 동향

- 알루미늄

- 강철

- 주석

- 기타

제6장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 크라운

- 캔 엔드

- 나사

- 트위스트

- 기타

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 식품 및 음료

- 의약품

- 소비재

- 퍼스널케어 및 화장품

- 기타

제8장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 판매자/도매업체

- 소매업체

- 전자상거래

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Amcor

- AptarGroup

- Berry Global

- CL Smith

- Closure Systems International

- Crown Holdings

- Finn-Korkki

- Guala Closures

- MJS Packaging

- Metal Closures

- Nippon Closures

- O. Berk

- Pelliconi

- Silgan Holdings

- Sonoco Products

- Tecnocap

The Global Metal Closures Market was valued at USD 25.9 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 45 billion by 2034. This growth is primarily driven by the increasing demand for packaged food and beverages, along with rising consumption of alcoholic drinks across both developed and emerging economies. As consumer lifestyles become more fast-paced and urbanized, the need for convenient, durable, and tamper-proof packaging solutions has grown substantially, fueling the adoption of metal closures. These closures are favored due to their ability to preserve product integrity, offer extended shelf life, and support sustainable packaging efforts. In recent years, market players have responded to evolving regulations and consumer expectations by incorporating environmentally friendly features and prioritizing recyclable materials.

The imposition of tariffs on imported aluminum and steel under the Trump administration significantly impacted the industry. These measures led to raw material cost surges-up to 25%-causing widespread disruptions for manufacturers reliant on imports. Domestic players faced tightened margins and had to pass on higher costs to customers. While some local metal producers benefited from the temporary pricing advantage, the broader industry dealt with heightened volatility and rising operational expenses. These challenges also encouraged firms to re-evaluate sourcing strategies, with many shifting towards automation and exploring alternative materials to stabilize production costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.9 Billion |

| Forecast Value | $45 Billion |

| CAGR | 5.8% |

By material, the market is segmented into aluminum, steel, tin, and others. The aluminum segment dominated in 2024, generating over USD 10.4 billion. Aluminum closures are widely chosen for their lightweight nature, which reduces logistics expenses, and their durability, which provides reliable sealing solutions. This material is especially favored for its resistance to corrosion and compatibility with acidic products. Its alignment with circular economy initiatives and rising corporate commitments toward sustainability are boosting its adoption across various industries.

In terms of product type, the market includes crown, can-ends, screw, twist, and other closures. The can-ends category emerged as the leading segment, surpassing USD 8.4 billion in 2024. Their increasing use in the packaging of food and beverages has significantly accelerated demand. These closures provide excellent sealing performance, making them ideal for maintaining freshness and preventing contamination. The popularity of convenient packaging solutions has also contributed to the rapid growth of this segment, especially in sectors where longevity and user-friendliness are essential.

Based on end-use, the metal closures market is divided into personal care and cosmetics, food and beverage, consumer goods, pharmaceuticals, and others. The food and beverage sector led the market in 2024 with a valuation of USD 8.4 billion. Changing consumption habits, increased preference for ready-to-eat meals, and the widespread use of airtight containers in processed food have all played a vital role in driving demand. Metal closures offer barrier properties that protect contents from moisture and oxygen, helping extend shelf life and maintain quality, especially for carbonated and fermented beverages.

Regarding distribution channels, the market is segmented into direct sales, distributors/wholesalers, retailers, and e-commerce. Distributors and wholesalers accounted for the highest market share in 2024, reaching USD 9.8 billion. The growth of this segment is attributed to bulk purchasing by manufacturers across various industries, ensuring reliable supply chain continuity. These distributors often cater to mid-sized firms with flexible order sizes and custom options, enabling them to meet the needs of niche markets and specialty packaging requirements.

The United States held the largest regional share in 2024, valued at USD 8 billion. The country's robust pharmaceutical production infrastructure, combined with stringent safety and packaging standards, has driven the adoption of advanced closure systems. Metal closures designed with tamper-evident and child-resistant features have become increasingly important for compliance and consumer safety. Demand is also being fueled by the rising popularity of premium packaged goods, along with increased consumption of alcohol-based beverages, all of which require secure and efficient sealing technologies.

Competition in the metal closures industry is intense, with the presence of both global and regional manufacturers. The top three companies- Silgan Holdings Inc., Crown Holdings Inc., and Guala Closures Group-together held a market share of over 12.8% in 2024. Leading firms continue to invest in research and development to introduce next-generation products focusing on lightweight materials, enhanced recyclability, and innovative sealing mechanisms. Features such as smart closures equipped with QR codes and NFC chips are gaining momentum as companies look to boost consumer engagement, traceability, and product safety. Additionally, the rising importance of health-conscious and traceable packaging is prompting manufacturers to develop closures with features like BPA-NI linings and high-barrier technologies. The growing popularity of online retail, direct-to-consumer brands, and craft production across industries is also amplifying the need for customizable, short-run closures that combine functionality with aesthetic appeal.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising demand for packaged food & beverages

- 3.3.1.2 Booming pharmaceutical industry

- 3.3.1.3 Increasing alcoholic beverage consumption

- 3.3.1.4 Long shelf life and hermetic sealing

- 3.3.1.5 Sustainability & recyclability appeal

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Volatility in raw material prices

- 3.3.2.2 Substitution by lightweight flexible packaging

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Million and Billion Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

- 5.4 Tin

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million and Billion Units)

- 6.1 Key trends

- 6.2 Crown

- 6.3 Can-ends

- 6.4 Screw

- 6.5 Twist

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million and Billion Units)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Pharmaceuticals

- 7.4 Consumer goods

- 7.5 Personal care & cosmetics

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million and Billion Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Distributors / wholesalers

- 8.4 Retailer

- 8.5 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million and Billion Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amcor

- 10.2 AptarGroup

- 10.3 Berry Global

- 10.4 CL Smith

- 10.5 Closure Systems International

- 10.6 Crown Holdings

- 10.7 Finn-Korkki

- 10.8 Guala Closures

- 10.9 MJS Packaging

- 10.10 Metal Closures

- 10.11 Nippon Closures

- 10.12 O. Berk

- 10.13 Pelliconi

- 10.14 Silgan Holdings

- 10.15 Sonoco Products

- 10.16 Tecnocap