|

시장보고서

상품코드

1750496

자동차 시트 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automotive Seating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

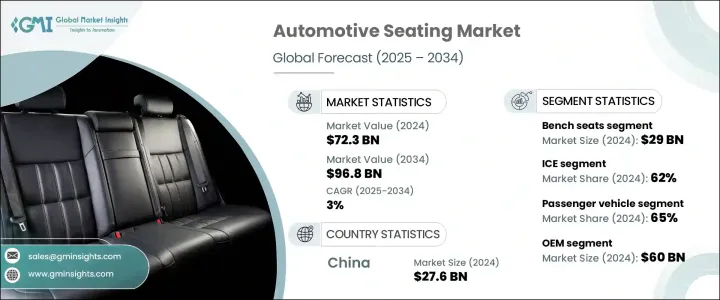

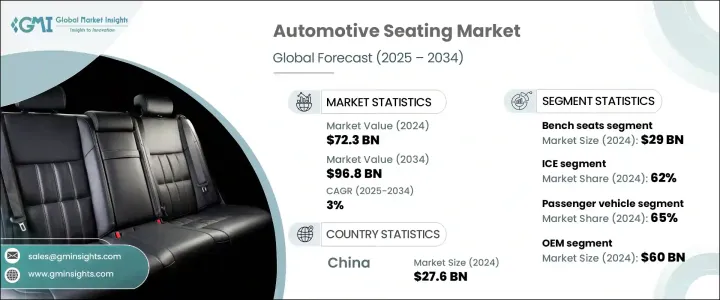

세계의 자동차 시트 시장은 2024년에는 723억 달러로 자동차 생산 증가, 안전 규제 강화, 쾌적성과 편의성에 대한 소비자의 기대 증가를 배경으로 2034년까지는 968억 달러에 달할 것으로 예측되며, CAGR3%로 성장할 전망입니다.

자동차 제조사들은 미적 디자인과 승객 경험을 향상시키는 것뿐 아니라 진화하는 기준과 소비자 선호도에 부합하는 스마트 기술과 지속 가능한 소재를 통합하기 위해 시트 시스템을 재검토하고 있습니다.

자동차 시트 산업에서 눈에 띄는 변화는 인체 공학 및 건강에 민감한 디자인이 점점 더 중요해지고 있다는 점입니다. 자동차 제조업체들은 맞춤형 요추 지지대, 압력 감지 시스템, 자세 교정 메커니즘, 스마트 시트 모니터링 솔루션 등 첨단 시트 기술에 대한 투자를 확대하고 있습니다. 이러한 기능은 운전 편의성을 높일 뿐 아니라 장시간 여행 중 피로를 줄이고 척추 정렬을 개선하여 장기적인 건강을 지원하기 위해 설계되었습니다. 경량 복합 재료는 구조적 강도와 차량 무게 감소를 균형 있게 조화시켜 연료 및 에너지 효율성을 높이는 데 기여하고 있습니다. 이처럼 지능형 인체공학 시트 시스템에 대한 집중은 차량 내부를 사용자 중심 환경으로 변모시켜 제조사가 변화하는 소비자 기대에 부응하도록 돕습니다. 중급 차량에서도 프리미엄 경험에 대한 수요가 증가함에 따라 시트는 브랜드 차별화와 구매 결정의 핵심 요소로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025년-2034년 |

| 시작금액 | 723억 달러 |

| 예측 금액 | 968억 달러 |

| CAGR | 3% |

내연 기관(ICE) 차량 부문은 2024년에 62%의 점유율을 차지하며, 전 세계 자동차 라인업에서 폭넓게 사용되고 있어 계속해서 우위를 차지할 것으로 보입니다. 그러나 전기자동차(EV) 부문은 모멘텀을 얻고 있으며, 예측 기간 동안 약 4%의 CAGR로 성장할 것으로 예상됩니다. ICE 모델은 다양성과 접근성으로 인해 여전히 인기가 있지만, EV 제조업체들은 기술에 정통하고 편안함을 중시하는 소비자를 유치하기 위해 요추 조절, 통풍, 마사지 기능 등 정교한 좌석 기능을 통합하고 있습니다.

2024년에는 벤치 시트 부문이 290억 달러의 매출을 올릴 것으로 예상됩니다. 벤치 시트의 인기는 승객 공간을 최대한 확보해야 하는 SUV, 밴, 다목적 차량에서 실용성이 높기 때문입니다. 이러한 구성은 좌석 수를 늘리고 다양한 레이아웃을 가능하게 하여 가족용 및 차량용 차량 부문 모두에 적합합니다. 간결한 구조와 저렴한 가격 덕분에 벤치 시트는 개발 도상국과 성숙한 시장 모두에서 신뢰할 수 있는 선택으로 계속 자리매김하고 있습니다.

중국의 자동차 시트 시장은 차량 제조 생태계, 첨단 인테리어 기능에 대한 선호도 증가, 맞춤화, 연결성 및 고급스러움을 우선으로 하는 시트 시스템에 대한 새로운 수요에 힘입어 2024년에 276억 달러의 매출을 달성했습니다. 전기자동차와 고급 모델이 인기를 끌면서 통풍 시트, 전자식 조절 기능, 메모리 기능과 같은 기능이 표준으로 기대되고 있습니다. 중국 자동차 제조사들은 빠른 혁신과 현지 생산 강화로 대응하며, 이는 해당 국가의 지역 시트 산업 지배력을 더욱 공고히 하고 있습니다.

이 시장을 형성하는 주요 기업인 GRAMMER, RECARO Holding, Toyota Boshoku, Lear, MG Seating Systems, Adient, Magna International, Brose Sitech, Faurecia, Fisher and Company등입니다. 경쟁 우위를 유지하기 위해 주요 자동차 시트 제조업체들은 지속 가능하고 인체공학적인 소재에 대한 연구개발 투자, OEM과의 협력, 지역 생산 확대 등 전략적 조치를 집중하고 있습니다. 많은 기업들은 디지털 기술과 AI 기반 시트 시스템을 통합해 승객 경험 향상, 브랜드 정체성 강화, 주요 자동차 제조사와의 장기 계약 확보를 목표로 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 재료 제공업체

- 부품 공급업체

- 제조업자

- 리셀러

- OEM

- 기술 인테그레이터

- 최종 용도

- 이익률 분석

- 공급자의 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 전략적인 업계 대응

- 공급망 재구성

- 무역에 미치는 영향

- 가격 설정 및 제품 전략

- 기술과 혁신의 상황

- 현재의 기술 동향

- 스마트 시트 기술

- 차량 시스템과의 통합

- 경량화 기술

- 쾌적성 향상 기술

- 신흥기술

- AI와 머신러닝의 용도

- 좌석 시스템에 IoT 통합

- 생체 인증 감지 및 모니터링

- 첨단 재료 과학

- 현재의 기술 동향

- 특허 분석

- 주요 뉴스와 대처

- 소비자의 선호와 행동

- 편안함의 기대

- 좌석 취향에 대한 인구통계학적 영향

- 좌석의 쾌적함에 관한 소비자의 인식

- 가격 동향

- 시트

- 지역

- 코스트 내역 분석

- 규제 상황

- 영향요인

- 성장 촉진요인

- 스마트 및 커넥티드 시트 기술의 통합

- 경량 및 지속 가능한 소재의 발전

- 전기 및 자율주행 차량의 인테리어 재구성 증가

- 센서 및 에어백 통합을 통한 안전 기능 강화

- 업계의 잠재적 리스크 및 과제

- 폴리우레탄 폼 및 복합 재료의 재활용 복잡성

- 고급 시트 메커니즘 개발 비용 증가

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 시트별(2021-2034년)

- 주요 동향

- 접이식 시트

- 버킷 시트

- 벤치 시트

- 분할 시트

- 기타

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 표준

- 전동

- 통풍

- 에어컨 설비

- 마사지 기능

- 기타

제7장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 천연 가죽

- 합성 가죽

- 패브릭

- 지속 가능

- 재활용

- 바이오 기반

- 식물 기반

제8장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제9장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 프레임

- 폼 패딩

- 시트 조절기

- 헤드레스트

- 기타

제10장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 내연기관(ICE)

- 전기자동차(EV)

- 하이브리드 자동차

제11장 시장 추계 및 예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제12장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제13장 기업 프로파일

- Adient

- Brose Sitech

- Camaco-Amvian

- Dura Automotive Systems

- Faurecia

- Fisher and Company

- Freedman Seating

- GRAMMER

- Guelph Manufacturing

- Lear

- Magna International

- MG Seating Systems

- NHK Spring

- RECARO

- TACHI-S

- TM Systems

- Toyota Boshoku

- True Assistive Tech

- TS Tech

- Woodbridge

The Global Automotive Seating Market was valued at USD 72.3 billion in 2024 and is estimated to grow at a CAGR of 3% to reach USD 96.8 billion by 2034, fueled by increasing automobile production, tightening safety regulations, and rising consumer expectations for comfort and convenience. Automakers are rethinking seating systems not only to enhance aesthetics and passenger experience but to integrate smart technologies and sustainable materials that meet evolving standards and buyer preferences.

A noticeable shift in the automotive seating industry is the growing prioritization of ergonomics and health-conscious design. Automakers are ramping up investments in advanced seat technologies such as customizable lumbar support, pressure-sensing systems, posture correction mechanisms, and smart in-seat monitoring solutions. These features are designed not only to elevate driving comfort but also to support long-term health by reducing fatigue and enhancing spinal alignment during extended travel. Lightweight composite materials are increasingly used to balance structural strength with reduced vehicle weight, contributing to greater fuel and energy efficiency. This focus on intelligent, ergonomic seating systems transforms vehicle interiors into more user-centric environments, helping manufacturers meet evolving consumer expectations. As demand rises for premium experiences even in mid-range vehicles, seating has become a defining element of brand distinction and buyer decision-making.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $72.3 Billion |

| Forecast Value | $96.8 Billion |

| CAGR | 3% |

The internal combustion engine (ICE) vehicles segment held a 62% share in 2024, continuing to dominate due to their extensive presence across global automotive lineups. However, the electric vehicle (EV) segment is gaining momentum, projected to grow at approximately 4% CAGR through the forecast period. While ICE models remain popular for their variety and accessibility, EV manufacturers incorporate sophisticated seat functionalities, like lumbar adjustments, ventilation, and massage features, to attract tech-savvy, comfort-driven consumers.

In 2024, the bench seats segment will generate USD 29 billion. Their popularity stems from their practicality in SUVs, vans, and multipurpose vehicles, where maximizing passenger space is essential. These configurations allow for increased seating capacity and versatile layouts, making them well-suited for both family and fleet-oriented vehicle segments. Their streamlined construction and affordability continue to make bench seats a reliable choice in both developing and mature markets.

China Automotive Seating Market generated USD 27.6 billion in 2024, driven by the vehicle manufacturing ecosystem, a rising preference for high-tech interior features, and the new demand for seating systems prioritizing customization, connectivity, and premium feel. As electric vehicles and luxury models gain traction, features like ventilated seating, electronic adjustability, and memory functions are becoming standard expectations. China's automakers are responding with rapid innovation and enhanced local production, further reinforcing the country's dominance in the regional seating industry.

Key players shaping this market include GRAMMER, RECARO Holding, Toyota Boshoku, Lear, MG Seating Systems, Adient, Magna International, Brose Sitech, Faurecia, and Fisher and Company. To maintain a competitive edge, leading automotive seating manufacturers focus on strategic moves such as R&D investments in sustainable and ergonomic materials, collaborations with OEMs, and regional manufacturing expansion. Many integrate digital technology and AI-enabled seating systems to elevate passenger experience, strengthen brand identity, and secure long-term contracts with top automakers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Distributors

- 3.1.1.5 OEMs

- 3.1.1.6 Technology integrators

- 3.1.1.7 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.1 Impact on trade

- 3.3 Pricing and product strategies

- 3.4 Technology & innovation landscape

- 3.4.1 Current technological trends

- 3.4.1.1 Smart seating technologies

- 3.4.1.2 Integration with vehicle systems

- 3.4.1.3 Weight reduction technologies

- 3.4.1.4 Comfort enhancement technologies

- 3.4.2 Emerging Technologies

- 3.4.2.1 AI and Machine Learning Applications

- 3.4.2.2 IoT integration in seating systems

- 3.4.2.3 Biometric sensing and monitoring

- 3.4.2.4 Advanced material sciences

- 3.4.1 Current technological trends

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Consumer preferences and behavior

- 3.7.1 Comfort expectations

- 3.7.2 Demographic influences on seating preferences

- 3.7.3 Consumer perception of seating comfort

- 3.8 Price trend

- 3.8.1 Seat

- 3.8.2 Region

- 3.9 Cost breakdown analysis

- 3.10 Regulatory landscape

- 3.11 Impacting forces

- 3.11.1 Growth drivers

- 3.11.1.1 Integration of smart and connected seating technologies

- 3.11.1.2 Advancements in lightweight and sustainable materials

- 3.11.1.3 Growth in electric and autonomous vehicle interior reconfigurations

- 3.11.1.4 Enhanced safety features with sensor and airbag integrations

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 Complexity in recycling polyurethane foams and composites

- 3.11.2.2 High development costs for advanced seat mechanisms

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Seat, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Folding seat

- 5.3 Bucket seat

- 5.4 Bench seat

- 5.5 Split seat

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Standard

- 6.3 Powered

- 6.4 Ventilated

- 6.5 Climate-Controlled

- 6.6 Massage

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Genuine leather

- 7.3 Synthetic leather

- 7.4 Fabric

- 7.5 Sustainable

- 7.5.1 Recycled

- 7.5.2 Bio-based

- 7.5.3 Plant-derived

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Hatchback

- 8.2.2 Sedan

- 8.2.3 SUVs

- 8.3 Commercial vehicles

- 8.3.1 Light commercial vehicles (LCVs)

- 8.3.2 Medium commercial vehicles (MCV)

- 8.3.3 Heavy commercial vehicles (HCVs)

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Frames

- 9.3 Foam padding

- 9.4 Seat adjuster

- 9.5 Headrests

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Internal combustion engine (ICE)

- 10.3 Electric vehicles (EVs)

- 10.4 Hybrid vehicles

Chapter 11 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 Original equipment manufacturers (OEMs)

- 11.3 Aftermarket

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 12.1 Key Trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Southeast Asia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 Saudi Arabia

- 12.6.3 South Africa

Chapter 13 Company Profiles

- 13.1 Adient

- 13.2 Brose Sitech

- 13.3 Camaco-Amvian

- 13.4 Dura Automotive Systems

- 13.5 Faurecia

- 13.6 Fisher and Company

- 13.7 Freedman Seating

- 13.8 GRAMMER

- 13.9 Guelph Manufacturing

- 13.10 Lear

- 13.11 Magna International

- 13.12 MG Seating Systems

- 13.13 NHK Spring

- 13.14 RECARO

- 13.15 TACHI-S

- 13.16 TM Systems

- 13.17 Toyota Boshoku

- 13.18 True Assistive Tech

- 13.19 TS Tech

- 13.20 Woodbridge