|

시장보고서

상품코드

1750519

비포장 폼 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Nonpackaging Foam Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

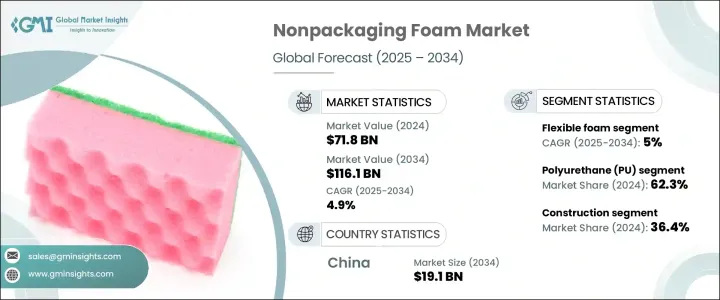

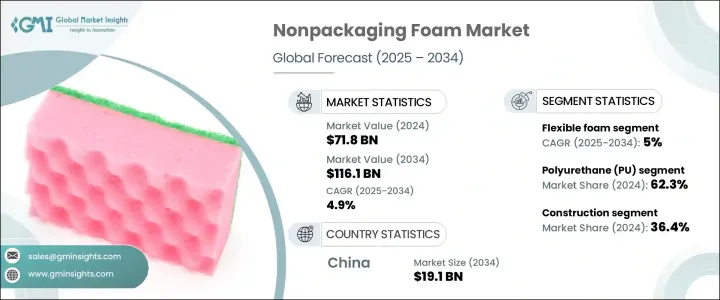

세계의 비포장 폼 시장 규모는 2024년 718억 달러로 평가되었고, 건설, 자동차, 가구, 일렉트로닉스, 헬스케어 등 분야에서 경량이고 내구성 있는 단열재에 대한 수요 증가를 배경으로 CAGR 4.9%로 성장할 전망이며, 2034년에는 1,161억 달러에 달할 전망입니다.

산업이 계속 확대되고 있는 가운데 비포장 폼은 그 범용성, 성능, 다양한 용도의 특정한 요구를 충족시키는 능력에 의해 필수적이 되고 있습니다. 북미, 유럽, 아시아태평양의 신흥 시장에서는 환경 문제에 대응하고 엄격한 규제를 충족시키기 위해 바이오 기반, 재활용 가능, 생분해성 등 지속 가능한 발포체 솔루션 개척에 점점 더 힘을 쏟고 있습니다.

지속가능성에 대한 노력은 비포장 폼 시장의 형성에 중요한 역할을 하고 있습니다. 기업은, 석유화학 원료에 대한 의존을 줄이고, 순환형 경제에 대한 대처를 지원하는 클로즈드 루프 리사이클 시스템에 투자하고 있습니다. 이 동향은 정부가 환경 정책을 강화하고 친환경 제품 개발을 장려하고 있는 북미와 유럽에서 특히 두드러집니다. 아시아태평양에서는 특히 중국 등 건설업과 자동차 산업이 주요 촉진 요인이 되고 있는 국가들에서 인프라와 제조업이 확대되면서 비포장 폼 수요가 빠르게 늘고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 718억 달러 |

| 예측 금액 | 1,161억 달러 |

| CAGR | 4.9% |

시장은 제품 유형별로 구분되며, 연질 폼과 경질 폼이 주요한 카테고리입니다. 연질 폼은 가구, 침구, 자동차 내장, 방음재 등 폭넓은 용도가 있기 때문에 2024년에는 477억 달러를 창출하였으며, 2034년에는 CAGR 5%로 성장할 전망이고, 778억 달러에 이를 것으로 예측됩니다. 인체공학에 기초한 매트리스나 경량의 자동차 부품 등, 쾌적성을 중시한 제품에 대한 수요의 고조가, 연질 폼의 확대를 뒷받침하고 있습니다. 게다가 지속 가능한 저VOC 처방으로의 시프트 증가나 전자상거래 대두가, 연질 폼의 수요를 한층 더 끌어올리고 있습니다.

비포장 폼 시장의 폴리우레탄(PU) 폼 분야는 2024년에 62.3%의 점유율을 차지했는데, 이는 단열재, 자동차 내장재, 가구용 쿠션재 등의 용도에 있어서 뛰어난 범용성에 기인합니다. PU 폼은 가볍고 내열성이 뛰어나 에너지 효율과 쾌적성을 중시하는 산업에 이상적인 소재입니다. PU 폼은 다양한 분야의 요구에 맞게 쉽게 커스터마이징 할 수 있기 때문에 그 수요는 더욱 높아지고 있습니다. 폭넓은 밀도와 형상으로 성형할 수 있기 때문에 경질과 연질 모두의 용도로 사용할 수 있으며, 다양한 시장에서 그 유용성이 확대되고 있습니다.

중국의 비포장 폼 2024년 시장 규모는 117억 달러로 평가되었고, 건설과 자동차 부문 수요 급증에 견인되어 CAGR 5.1%로 성장할 전망이며, 2034년에는 191억 달러에 이를 것으로 예측됩니다. 인프라 정비에 대한 정부 투자 증가는 단열재, 방음재, 구조용 폼 등의 재료에 대한 요구를 부추기고 있습니다. 게다가 전기자동차(EV)의 상승으로, 특히 경량이고 에너지 효율이 높은 재료에 대한 수요가 높아지고 있는 자동차 산업에 있어서, 폼의 새로운 이용 기회가 초래되고 있습니다. 이러한 분야가 계속 확대되고 있는 가운데 비포장 폼, 특히 PU 폼 시장은 중국에서 지속적인 성장을 이루려고 합니다.

세계의 비포장 폼 시장에서 주요 기업은 Huntsman Corporation, BASF, INOAC Corporation, Covestro 등입니다. 이러한 기업들은 생산 능력 확대, 제품 제공 강화, 지속가능성을 위한 노력을 추진하고 있습니다. 폼 제조의 기술적 진보를 활용하고 친환경 솔루션에 주력함으로써 이러한 기업들은 경쟁 시장에서의 입지를 강화하는 것을 목표로 하고 있습니다. 또한 세계의 비포장 폼 수요 증가에 대응하기 위해 전략적 제휴, 인수, 지역 확대에 대한 투자도 실시했습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권의 관세 영향 : 구조화된 개요

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망 및 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계

- 주요 수입국

- 국가 1

- 국가 2

- 국가 3

- 주요 수출국

- 국가 1

- 국가 2

- 국가 3

- 주요 수입국

- 이익률 분석

- 규제 상황

- 영향요인

- 성장 촉진요인

- 에너지 효율이 높은 건축 자재 수요 증가

- 자동차 및 가구 분야에서 경량성 및 쾌적성의 요건

- 신흥 시장의 급속한 산업화 및 인프라 개발

- 업계의 잠재적 위험 및 과제

- 발포 스티롤 폐기물 및 VOC 배출에 관한 환경 우려와 규제

- 원재료 가격 변동

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 밸류체인 분석

- 원재료 공급자

- 폼 제조업체

- 가공업자 및 컨버터

- 판매자 및 소매업체

- 최종 이용 산업

- 밸류체인 최적화 전략

- 비용 구조 분석

- 가격 분석

- 환경규제 및 컴플라이언스 요건

- 제품 규격 및 인증

- 수출입 규제

- 규제에 의한 시장 성장에 대한 영향

- 미래의 규제 동향

- 지속가능성 및 환경에 미치는 영향

- 소재 유형별 가격 평가

- 비포장 폼의 환경 실적

- 지속 가능한 폼 솔루션

- 바이오 폼

- 재활용 가능한 폼

- 생분해성 폼

- 재활용 및 폐기물 관리

- 순환형 경제의 대처

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 연질 폼

- 경질 폼

제6장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 폴리우레탄(PU)

- 폴리스티렌(PS)

- 폴리에틸렌(PE)

- 폴리프로필렌(PP)

- 고무 폼

- 기타

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 공사

- 자동차

- 가구 및 침구

- 일렉트로닉스

- 헬스케어

- 기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- BASF

- Armacell International

- Covestro

- Dow

- FXI Holdings

- Huntsman Corporation

- INOAC Corporation

- JSP Corporation

- Recticel

- Saint-Gobain

- Sheela Foam

- UFP Technologies

- Wanhua Chemical Group

- Woodbridge Group

- Zotefoams

The Global Nonpackaging Foam Market was valued at USD 71.8 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 116.1 billion by 2034, driven by the increasing demand for lightweight, durable insulating materials in sectors such as construction, automotive, furniture, electronics, and healthcare. As industries continue to expand, nonpackaging foam has become essential due to its versatility, performance, and ability to meet the specific needs of various applications. Manufacturers are increasingly focusing on developing sustainable foam solutions, such as bio-based, recyclable, and biodegradable options, to address environmental concerns and meet stringent regulations in North America, Europe, and emerging markets in Asia-Pacific.

Sustainability efforts are playing a significant role in shaping the nonpackaging foam market. Companies are investing in closed-loop recycling systems, which reduce the reliance on petrochemical feedstocks and support circular economy initiatives. This trend is particularly prominent in North America and Europe, where governments are tightening environmental policies and encouraging the development of eco-friendly products. In Asia-Pacific, the demand for nonpackaging foam is growing rapidly, driven by the expansion of infrastructure and manufacturing sectors, especially in countries such as China, where construction and automotive industries are key growth drivers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $71.8 Billion |

| Forecast Value | $116.1 Billion |

| CAGR | 4.9% |

The market is segmented by product type, with flexible and rigid foam being the two main categories. Flexible foam generated USD 47.7 billion in 2024 and is projected to reach USD 77.8 billion by 2034, growing at a 5% CAGR due to its broad range of applications, including furniture, bedding, automotive interiors, and acoustic insulation. The growing demand for comfort-focused products, such as ergonomic mattresses and lightweight vehicle components, is driving the expansion of flexible foam. Additionally, the increasing shift toward sustainable, low-VOC formulations and the rise of e-commerce have further boosted the demand for flexible foam.

Polyurethane (PU) foam segment in the nonpackaging foam market held 62.3% share in 2024, attributed to its exceptional versatility in applications such as thermal insulation, automotive interiors, and cushioning for furniture. The material's lightweight nature and excellent thermal resistance make it an ideal choice for industries that prioritize energy efficiency and comfort. PU foam is easily customizable to meet the specific needs of different sectors, which further drives its demand. Its capacity to be molded into a wide range of densities and forms enables it to serve both rigid and flexible purposes, expanding its utility across various markets.

China Nonpackaging Foam Market generated USD 11.7 billion in 2024 and is expected to grow at a CAGR of 5.1%, reaching USD 19.1 billion by 2034, driven by the surging demand in the construction and automotive sectors. Increased government investment in infrastructure development is fueling the need for materials like insulation, soundproofing, and structural foam. Additionally, the rise of electric vehicles (EVs) has introduced new opportunities for foam usage, particularly in the automotive industry, where demand for lightweight, energy-efficient materials is on the rise. As these sectors continue to expand, the market for nonpackaging foam, especially PU foam, is poised for sustained growth in China.

Leading players in the Global Nonpackaging Foam Market include Huntsman Corporation, BASF, INOAC Corporation, and Covestro. These companies are focusing on expanding their production capacities, enhancing product offerings, and advancing sustainability initiatives. By leveraging technological advancements in foam production and focusing on eco-friendly solutions, these players aim to strengthen their position in the competitive market. Moreover, they are investing in strategic partnerships, acquisitions, and regional expansions to meet the growing demand for nonpackaging foam globally.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade Statistics

- 3.3.1 Major importing countries

- 3.3.1.1 Country 1

- 3.3.1.2 Country 2

- 3.3.1.3 Country 3

- 3.3.2 Major exporting countries

- 3.3.2.1 Country 1

- 3.3.2.2 Country 2

- 3.3.2.3 Country 3

- 3.3.1 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for energy-efficient building materials

- 3.6.1.2 Lightweight and comfort requirements in automotive and furniture sectors

- 3.6.1.3 Rapid industrialization and infrastructure development in emerging markets

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Environmental concerns and regulations on foam waste and VOC emissions

- 3.6.2.2 Volatility in raw material prices

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

- 3.10.1 Raw material suppliers

- 3.10.2 Foam manufacturers

- 3.10.3 Fabricators and converters

- 3.10.4 Distributors and retailers

- 3.10.5 End-use industries

- 3.10.6 Value chain optimization strategies

- 3.10.7 Cost structure analysis

- 3.11 Pricing Analysis

- 3.11.1 North America

- 3.11.2 Europe

- 3.11.3 Asia Pacific

- 3.11.4 Latin America

- 3.11.5 Middle East and Africa

- 3.12 Environmental regulations and compliance requirements

- 3.12.1 Product standards and certifications

- 3.12.2 Import/export regulations

- 3.12.3 Regulatory impact on market growth

- 3.12.4 Future regulatory trends

- 3.13 Sustainability and environmental impact

- 3.13.1 Price point assessment by material type

- 3.13.2 Environmental footprint of nonpackaging foam

- 3.13.3 Sustainable foam solutions

- 3.13.4 Bio-based foams

- 3.13.5 Recyclable foams

- 3.13.6 Biodegradable foams

- 3.13.7 Recycling and waste management

- 3.13.8 Circular economy initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Flexible foam

- 5.3 Rigid foam

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Polyurethane (PU)

- 6.3 Polystyrene (PS)

- 6.4 Polyethylene (PE)

- 6.5 Polypropylene (PP)

- 6.6 Rubber foam

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Automotive

- 7.4 Furniture & bedding

- 7.5 Electronics

- 7.6 Healthcare

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 BASF

- 9.2 Armacell International

- 9.3 Covestro

- 9.4 Dow

- 9.5 FXI Holdings

- 9.6 Huntsman Corporation

- 9.7 INOAC Corporation

- 9.8 JSP Corporation

- 9.9 Recticel

- 9.10 Saint-Gobain

- 9.11 Sheela Foam

- 9.12 UFP Technologies

- 9.13 Wanhua Chemical Group

- 9.14 Woodbridge Group

- 9.15 Zotefoams