|

시장보고서

상품코드

1750577

연료전지 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Fuel Cell Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

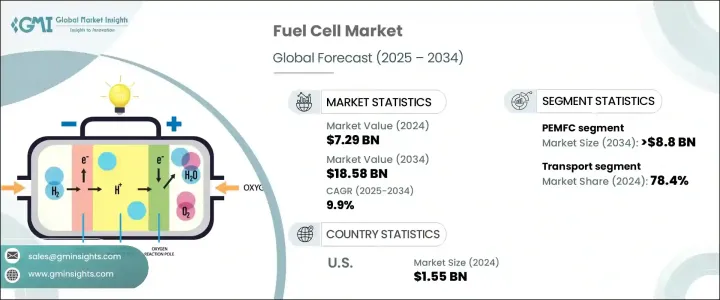

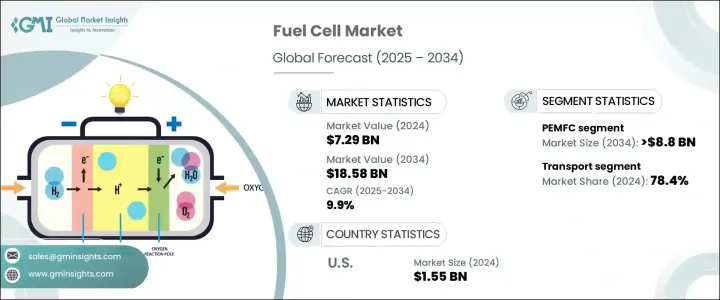

2024년 세계의 연료전지 시장 규모는 72억 9,000만 달러로 평가되었고, 깨끗하고 신뢰성 있고 효율적인 전원에 대한 요구가 계속 증가하고 있기 때문에 CAGR 9.9%를 나타내 2034년에는 185억 8,000만 달러에 이를 것으로 추정되고 있습니다.

이 성장의 원동력이 되는 것은 원격지 및 비전화 지역에서의 전력 수요 증가와 배출량 감축을 목적으로 한 환경 규제의 강화입니다. 산업계가 지속가능성과 비용 효율적인 전력 솔루션에 초점을 맞추는 동안 연료전지는 유망한 대안으로 부상하고 있습니다. 이러한 시스템은 높은 운전 효율, 환경에 미치는 영향, 기존 기술에 비해 경쟁력 있는 가격 설정으로 인해 특히 매력적입니다.

연료전지는 무정전 전원 공급 및 저배출 솔루션이 중요한 제조 부문에서 널리 채택되었습니다. 공해를 최소화하면서 전력을 생산할 수 있는 연료전지는 정부와 민간 기업의 주목을 받고 있습니다. 이산화탄소 배출량 감축과 에너지 효율 개선에 초점을 맞춘 정책을 전개하는 국가가 늘어나는 가운데, 다양한 용도에서의 연료전지의 이용은 꾸준히 확대되고 있습니다. 금융기관과 정부기관은 이 분야의 기술진보를 추진하기 위해 연구개발에 많은 투자를 하고 있습니다. 기술 혁신이 진행됨에 따라, 연료전지는 상업용 및 주택용 에너지 시스템 모두에서 점점 실용적이 될 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 72억 9,000만 달러 |

| 예측 금액 | 185억 8,000만 달러 |

| CAGR | 9.9% |

관민 양부문으로부터의 투자도 시장의 성장에 기여하고 있습니다. 세계의 조직이, 연료전지의 성능, 효율, 가격을 향상시키는 선진 기술의 개발에의 대처를 강화하고 있습니다.

다양한 유형의 연료전지 중에서도 고체 고분자형 연료전지(PEMFC) 분야는 2034년까지 88억 달러 이상에 달할 것으로 예상되고 있습니다. 솔루션부터 휴대용 에너지 시스템, 자동차에 이르기까지 다양한 용도에 이상적입니다.

응용 분야의 관점에서 시장은 고정형, 휴대용 및 운송 분야로 분류됩니다. 배출가스 감축과 환경친화적인 기술로의 전환에 점점 더 많은 관심을 받고 있으며, 수소연료전지 시스템의 통합을 뒷받침하고 있습니다.

미국이 주도하는 북미 연료전지 시장도 꾸준한 성장을 이루고 있습니다. 통합된 메탄 개질 기술을 이용한 현장 수소 생성 스테이션의 개발은 연료 공급 인프라에 비용 효율적인 솔루션을 제공하고, 지역적인 보급을 뒷받침하고 있습니다.

세계의 연료전지 시장은 현재 혁신과 협업을 통해 시장에서의 지위 강화에 지속적으로 임하고 있는 여러 주요 기업의 존재에 의해 형성되고 있습니다. Power-collectively의 주요 5개사는 합계로 세계 시장 점유율의 약 40%를 차지하고 있습니다.이러한 기업의 전략에는 에너지 기업, 자동차 제조업체, 연구 기관과 제휴를 맺어, 제품 라인업을 충실시키고, 기술 개발을 가속시키는 것이 포함됩니다.

전략적 파트너십, 합작투자, 정부 및 민간 단체로부터의 자금 제공 증가로 연구개발의 페이스가 가속화되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 에코시스템

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율

- 전략적 노력

- 전략적 대시보드

- 기업 벤치마킹

- 혁신과 기술 상황

제5장 연료전지 시장 : 제품별(2021-2034년)

- 주요 동향

- PEMFC

- DMFC

- SOFC

- PAFC 및 AFC

- MCFC

제6장 연료전지 시장 : 용도별(2021-2034년)

- 주요 동향

- 고정형

- 200kW 미만

- 200kW-1MW

- 1MW 이상

- 휴대용

- 운송

- 선박

- 철도

- FCEV

- 기타

제7장 연료전지 시장 : 연료별(2021-2034년)

- 주요 동향

- 수소

- 암모니아

- 메탄올

- 탄화수소

제8장 연료전지 시장 : 사이즈별(2021-2034년)

- 주요 동향

- 소

- 대

제9장 연료전지 시장 : 최종 용도별(2021-2034년)

- 주요 동향

- 주택

- 상업 및 산업

- 데이터센터

- 군사 및 방위

- 유틸리티 및 정부

- 운송

제10장 연료전지 시장 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 오스트리아

- 아시아태평양

- 일본

- 한국

- 중국

- 인도

- 필리핀

- 베트남

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 라틴아메리카

- 브라질

- 페루

- 멕시코

제11장 기업 프로파일

- Cummins

- Ballard Power Systems

- Plug Power

- Nuvera Fuel Cells

- Nedstack Fuel Cell Technology

- Bloom Energy

- Panasonic Corporation

- Doosan Fuel Cell

- Aisin Corporation

- Ceres

- SFC Energy

- Toshiba Corporation

- Robert Bosch

- TW Horizon Fuel Cell Technologies

- AFC Energy

- FuelCell Energy

- Fuji Electric

- Hyundai Motor Company

The Global Fuel Cell Market was valued at USD 7.29 billion in 2024 and is estimated to grow at a CAGR of 9.9% to reach USD 18.58 billion by 2034 as the need for clean, reliable, and efficient power sources continues to grow. This growth is being driven by an increasing demand for power in remote and off-grid locations, as well as by tightening environmental regulations aimed at reducing emissions. As industries shift their focus toward sustainability and cost-effective power solutions, fuel cells are emerging as a promising alternative. These systems are particularly attractive due to their high operational efficiency, lower environmental impact, and competitive pricing compared to conventional technologies.

Fuel cells are being widely adopted in the manufacturing sector, where uninterrupted power supply and low-emission solutions are critical. Their capability to produce electricity with minimal pollution has drawn the attention of governments and private players alike. With a growing number of countries rolling out policies focused on reducing carbon footprints and improving energy efficiency, the use of fuel cells across a range of applications is expanding steadily. Financial institutions and government bodies are pouring significant investments into research and development to drive technological advancements in this space. As innovation progresses, fuel cells are expected to become increasingly viable for both commercial and residential energy systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.29 Billion |

| Forecast Value | $18.58 Billion |

| CAGR | 9.9% |

Investments from both public and private sectors are also contributing to the growth of the market. Organizations across the globe are stepping up efforts to develop advanced technologies that improve the performance, efficiency, and affordability of fuel cells. These initiatives are encouraging companies across multiple industries to adopt fuel cell systems as part of their energy transition strategies. In response to these developments, the demand for next-generation fuel cell systems is growing rapidly.

Among the various types of fuel cells, the Proton Exchange Membrane Fuel Cell (PEMFC) segment is expected to surpass USD 8.8 billion by 2034. These fuel cells are known for their low operating temperature and quick startup times, making them ideal for a variety of applications, from backup power solutions to portable energy systems and automotive uses. As these technologies evolve and become more reliable, their use in sectors such as data centers, residential buildings, and mobile infrastructure is anticipated to increase significantly.

In terms of application, the market is categorized into stationary, portable, and transport sectors. The transport segment dominated the market in 2024, accounting for more than 78.4% of the total share. This segment is witnessing accelerated adoption of fuel cell systems in electric bikes, unmanned aerial vehicles, and commercial fleets. The transportation sector's increasing focus on reducing emissions and transitioning to greener technologies is propelling the integration of hydrogen fuel cell systems. As infrastructure for hydrogen production and distribution improves, the deployment of these systems across various transport applications, including maritime logistics and commercial shipping, is expected to expand.

The North American fuel cell market, led by the United States, is also witnessing steady progress. The US market alone recorded a value of over USD 1.52 billion in 2022, USD 1.53 billion in 2023, and reached USD 1.55 billion in 2024. Across the continent, the market is forecasted to grow at a CAGR of over 6% through 2034. The development of on-site hydrogen generation stations using integrated methane reforming technologies has provided cost-effective solutions for fueling infrastructure, thus boosting regional adoption. These advancements are creating a more favorable environment for the widespread deployment of fuel cells in both public and private sectors.

The global fuel cell market is currently shaped by the presence of several key players who are continuously working to strengthen their market position through innovation and collaboration. The top five companies-Cummins, Ballard Power Systems, Fuji Electric, Toshiba Corporation, and Plug Power-collectively account for around 40% of the global market share. Their strategies include forming alliances with energy companies, automotive manufacturers, and research institutions to enhance product offerings and accelerate technology development. These collaborative efforts are expanding the reach of fuel cell technology and opening new avenues for commercialization.

Strategic partnerships, joint ventures, and increased funding from both government and private entities are accelerating the pace of research and development. These efforts are not only driving innovation but also improving the scalability and market readiness of fuel cell solutions. As a result, the industry is moving closer to achieving large-scale deployment, with significant implications for the global energy landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic initiatives

- 4.4 Strategic dashboard

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Fuel Cell Market, By Product, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 PEMFC

- 5.3 DMFC

- 5.4 SOFC

- 5.5 PAFC & AFC

- 5.6 MCFC

Chapter 6 Fuel Cell Market, By Application, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Stationary

- 6.2.1 < 200 kW

- 6.2.2 200 kW - 1 MW

- 6.2.3 ≥ 1 MW

- 6.3 Portable

- 6.4 Transport

- 6.4.1 Marine

- 6.4.2 Railways

- 6.4.3 FCEVs

- 6.4.4 Others

Chapter 7 Fuel Cell Market, By Fuel, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Hydrogen

- 7.3 Ammonia

- 7.4 Methanol

- 7.5 Hydrocarbons

Chapter 8 Fuel Cell Market, By Size, 2021 - 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 Small scale

- 8.3 Large scale

Chapter 9 Fuel Cell Market, By End Use, 2021 - 2034 (USD Million & MW)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial & industrial

- 9.4 Data centers

- 9.5 Military and defense

- 9.6 Utilities & government

- 9.7 Transportation

Chapter 10 Fuel Cell Market, By Region, 2021 - 2034 (USD Million & MW)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Austria

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 South Korea

- 10.4.3 China

- 10.4.4 India

- 10.4.5 Philippines

- 10.4.6 Vietnam

- 10.5 Middle East & Africa

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Peru

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 Cummins

- 11.2 Ballard Power Systems

- 11.3 Plug Power

- 11.4 Nuvera Fuel Cells

- 11.5 Nedstack Fuel Cell Technology

- 11.6 Bloom Energy

- 11.7 Panasonic Corporation

- 11.8 Doosan Fuel Cell

- 11.9 Aisin Corporation

- 11.10 Ceres

- 11.11 SFC Energy

- 11.12 Toshiba Corporation

- 11.13 Robert Bosch

- 11.14 TW Horizon Fuel Cell Technologies

- 11.15 AFC Energy

- 11.16 FuelCell Energy

- 11.17 Fuji Electric

- 11.18 Hyundai Motor Company