|

시장보고서

상품코드

1750606

금속 유리 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Metallic Glasses Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

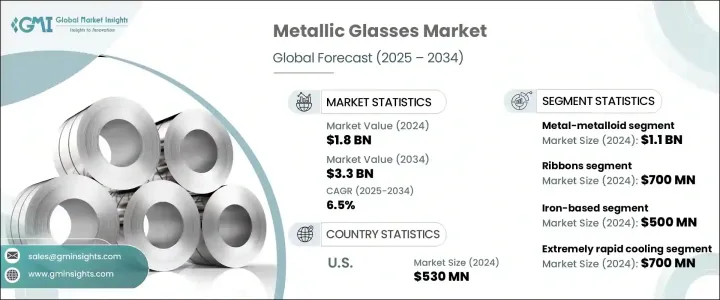

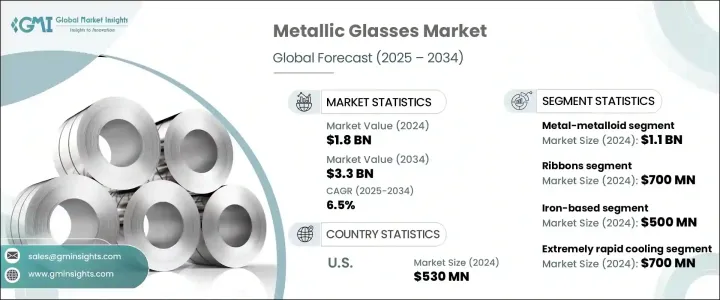

세계의 금속 유리 시장은 2024년에는 18억 달러로 평가되었으며, 2034년까지는 CAGR 6.5%를 나타내 33억 달러에 이를 것으로 추정되고 있습니다. 파스 원자 구조에 의해 엄격한 조건하에서도 매우 뛰어난 성능을 발휘해, 구조 강도와 정밀도에 이상적인 재료가 되고 있습니다. 전기 부품이나 자기 부품 등, 내구성과 내마모성을 필요로 하는 산업에서 유용합니다.

시장은 전자석 및 전자 분야에서 수요 증가로 이익을 얻고 있습니다. 생체 적합성과 기계적 강도가 의료용 임플란트나 수술 기구에 이상적이기 때문에 바이오메디컬 분야도 금속 유리의 중요한 성장 분야입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 18억 달러 |

| 예측 금액 | 33억 달러 |

| CAGR | 6.5% |

2024년 금속 유리 시장의 메탈메탈로이드 분야 시장 규모는 11억 달러로 평가되었고, 특히 소비자 일렉트로닉스, AR/VR(증강현실/가상현실), 의료기기 등 산업에서 경량이고 비용효율이 우수한 재료에 대한 수요가 높아지고 있는 것을 배경으로 2034년까지 연평균 복합 성장률(CAGR) 5.7%를 나타낼 것으로 예측됩니다. 이러한 재료는 강도와 유연성의 완벽한 균형을 제공하기 때문에 급속하게 발전하는 이러한 분야의 소형화 부품에 최적입니다.

2024년에 7억 달러로 평가된 리본 부문은 2034년까지 5.1%의 성장률을 나타낼 것으로 예측됩니다. 수술에 대한 수요가 증가함에 따라 금속 유리 리본은 이러한 용도에서 중요한 역할을 계속할 것으로 예측됩니다.

미국의 금속 유리 시장은 2024년에는 5억 3,000만 달러가 되었고 2025년부터 2034년까지의 CAGR 성장률은 6%를 나타낼 것으로 예측되어 항공우주, 방위 시스템, 일렉트로닉스에 있어서의 금속 유리 수요 증가가 견인하고 있습니다. 방위 계약자 간의 긴밀한 협력은 새로운 금속 유리 솔루션의 개발과 유통을 촉진하고 있습니다.

세계의 금속 유리 시장 주요 기업은 Heraeus Holding GmbH, Liquidmetal Technologies Inc. Materion Corporation, Usha Amorphous Metals Limited, itachi Metals Ltd. 등이 있습니다. 금속 유리 시장의 각 기업은 존재감을 높이기 위해 생산 능력을 확대하고 제조 공정를 개선하여 비용을 절감하는 데 주력하고 있습니다. 콜라보레이션은 기술 혁신과 신소재의 도입을 가속화하는 데 도움이 되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 시장 정의와 진화

- 금속 유리의 정의와 분류

- 금속 유리의 역사적 개발

- 재료의 조성과 특성

- 원자의 구조와 특성

- 기계적 특성

- 자기 특성

- 내식성

- 열특성

- 제조 공정

- 급속 응고 기술

- 멜트 스피닝

- 가스분석

- 흡입 주조

- 적층 조형

- 비교 분석 : 금속 유리 vs. 기존 재료

- 금속 유리 vs. 결정 금속

- 금속 유리 vs. 세라믹

- 금속 유리 vs. 폴리머

- 금속 유리에 있어서의 기술의 진보

- 트럼프 정권의 관세 영향 - 구조화된 개요

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

- 이익률 분석

- 규제 상황과 기준

- 세계의 규제 틀

- 지역 규제 틀

- 북미

- FDA 규제(의료 용도)

- ASTM 규격

- 기타 관련 규제

- 유럽

- EU 의료기기 규제(MDR)

- CE 마킹 요건

- 리치 규제

- 아시아태평양

- 중국의 규제

- 일본의 규제

- 기타 지역규제

- 세계의 기타 지역

- 북미

- 제품 인증 및 규격

- 품질 기준

- 안전기준

- 퍼포먼스 기준

- 컴플라이언스 과제와 전략

- 향후 규제 동향과 그 영향

- 시장 역학

- 시장 성장 촉진요인

- 우수한 재료 특성

- 전자 및 에너지 분야 수요 증가

- 제조 기술의 진보

- 바이오메디컬 분야에서의 응용 확대

- 시장 성장 억제요인

- 높은 생산 비용

- 사이즈와 형상의 제한

- 취성과 연성의 한계

- 기존의 재료와의 경쟁

- 시장 기회

- 항공우주 및 방위에 있어서의 새로운 용도

- 적층 조형의 진보

- 지속 가능한 소재에 대한 수요 증가

- 신흥 경제 국가의 확대

- 시장의 과제

- 생산규모 확대

- 일관된 품질 실현

- 규제 준수

- 시장의 인지도와 수용

- 시장 성장 촉진요인

- Porter's Five Forces 분석

- PESTEL 분석

- 밸류체인 분석

- 원재료 공급자

- 제조업체

- 유통업체

- 최종 사용자

- 환경·사회·거버넌스(ESG) 분석

- 환경 영향 평가

- 탄소 발자국 분석

- 수명 주기 평가(LCA)

- 폐기물 관리와 재활용

- 생산에 있어서의 에너지 소비

- 사회적 영향

- 노동 관행과 노동 조건

- 커뮤니티에 대한 영향과 관여

- 건강과 안전에 관한 고려 사항

- 거버넌스와 윤리적 배려

- 기업 지배 구조의 실천

- 윤리적인 공급망 관리

- 투명성과 보고

- 주요 기업의 ESG 퍼포먼스 벤치마크

- ESG 리스크 평가 및 경감 전략

- 금속 유리 업계의 향후 ESG 동향

- 환경 영향 평가

- 제조·생산 분석

- 제조 공정 개요

- 원재료 조달 및 준비

- 합금의 용해와 균질화

- 급속 응고 기술

- 후처리와 마무리

- 품질 관리 및 테스트

- 생산비용 분석

- 원재료비

- 에너지 비용

- 인건비

- 제조 간접비

- 비용 최적화 전략

- 제조시설 분석

- 주요 제조 거점

- 생산 능력 평가

- 시설 확장 계획

- 공급망의 과제와 해결책

- 제조 공정에서의 지속가능성

- 에너지 효율 대책

- 폐기물 삭감 전략

- 친환경 소재 및 공정

- 제조 공정 개요

- 소비자 행동과 시장 동향의 분석

- 소비자의 기호와 구매 패턴

- 구매결정에 영향을 미치는 요인

- 성능과 품질

- 비용 고려

- 지속가능성요인

- 브랜드의 평판

- 업계 고유의 채용 동향

- 일렉트로닉스 업계의 채용

- 자동차 업계에서의 채용

- 의료 업계에서의 채용

- 항공우주산업의 채용

- 소비자 행동의 지역차

- 디지털 변혁이 소비자 참여에 미치는 영향

- 미래의 소비자 동향과 그 영향

- 기술적 상황과 혁신 분석

- 금속 유리의 현재 기술 동향

- 신흥기술과 그 잠재적인 영향

- 첨단 제조 기술

- 새로운 합금 조성

- 표면 개질 기술

- 복합 금속 유리

- 연구개발활동과 혁신허브

- 용도 전체에 걸친 기술 채용 동향

- 기술 준비 상황 평가

- 향후 기술 로드맵(2025-2034년)

- 가격 분석과 경제적 요인

- 가격 동향 분석

- 역사적 가격 동향

- 현재 가격 시나리오

- 가격 예측

- 가격에 영향을 미치는 요인

- 원재료비

- 생산의 복잡성

- 생산규모

- 시장 경쟁

- 용도별 요건

- 지역별 가격 차이

- 가격과 가치의 관계 분석

- 시장에 영향을 미치는 경제지표

- GDP 성장률과 산업 생산

- 연구개발비

- 금속 상품 가격

- 에너지 비용

- 주요 시장 기업의 가격 전략

- 가격 동향 분석

- 원재료와 공급망 분석

- 주요 원재료의 개요

- 금속 및 메탈로이드

- 희토류 원소

- 기타 중요한 재료

- 원재료 조달 및 조달

- 세계공급원

- 공급 집중과 위험

- 지속 가능한 조달 노력

- 공급 체인의 구조와 역학

- 업스트림 공급망

- 중류 처리

- 하류 유통

- 공급망의 과제

- 원재료의 가용성과 중요성

- 가격 변동

- 지정학적 요인

- 물류와 수송

- 공급망 리스크 경감 전략

- 원재료와 공급 체인의 장래 동향

- 주요 원재료의 개요

제4장 경쟁 구도

- 주요 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 주요 기업이 채용하고 있는 경쟁 전략

- 제품의 혁신과 개발

- 합병 및 인수

- 파트너십 및 협업

- 확대 전략

- 투자분석과 시장의 매력

- 현재 투자 시나리오

- 투자 기회 : 부문별

- 투자 기회 : 지역별

- ROI 분석

- 벤처 캐피탈과 프라이빗 주식의 상황

- M&A 활동 분석

- 미래 투자 전망

- 리스크 평가 및 경감 전략

- 시장 위험

- 기술적 위험

- 규제 위험

- 경쟁위험

- 공급망의 위험

- 환경과 지속가능성의 위험

- 리스크 경감 전략

제5장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 금속-금속 금속 유리

- 금속-메탈로이드 금속 유리

제6장 시장 추계·예측 : 형태별(2021-2034년)

- 주요 동향

- 리본

- 와이어

- 분말

- 시트

- 기타

제7장 시장 추계·예측 : 재료 구성별(2021-2034년)

- 주요 동향

- 철 기반

- 지르코늄 기반

- 티타늄 기반

- 구리 기반

- 팔라듐 기반

- 마그네슘 기반

- 알루미늄 기반

- 기타 구성

제8장 시장 추계·예측 : 제조 공정별(2021-2034년)

- 주요 동향

- 매우 빠른 냉각

- 물리적 기상 증착

- 고체 상태 반응

- 이온 조사

- 기타

제9장 시장 추계·예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 전자 및 전기

- 자동차 및 운송

- 항공우주 및 방위

- 의료 및 헬스케어

- 스포츠 및 레저

- 에너지

- 산업기기

- 기타

제10장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Amorphology Inc.

- Antai Technology Co.Ltd.

- EPSON ATMIX Corporation

- Exmet AB

- Glassimetal Technology

- Heraeus Holding

- Hitachi Metals Ltd.

- Liquidmetal Technologies Inc.

- Materion Corporation

- PrometalTech

- PX Group SA

- Qingdao Yunlu Advanced Materials Technology Co.Ltd.

- RS Alloys

- Usha Amorphous Metals Limited

The Global Metallic Glasses Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 3.3 billion by 2034, driven by the unique properties of metallic glasses, which combine high tensile strength with excellent corrosion resistance and malleability. These materials' amorphous atomic structure allows them to perform exceptionally well under challenging conditions, making them ideal for structural strength and precision. They are useful in industries requiring durability and resistance to wear, such as electrical and magnetic components. As industries continue to demand more advanced and efficient materials, the versatile applications of metallic glasses are gaining traction.

The market benefits from increased demand in the electromagnetic and electronics sectors. Metallic glasses' low power dissipation and high efficiency make them suitable for magnetic cores, sensors, and transformers. Moreover, advancements in manufacturing technologies, such as rapid solidification and physical vapor deposition, are reducing production costs and enabling scalable operations. The biomedical sector is another key growth area for metallic glasses, as their biocompatibility and mechanical strength make them ideal for medical implants and surgical tools. Their resistance to bacteria and wear adds to their appeal for healthcare applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 6.5% |

In 2024, the metal-metalloid segment of the metallic glasses market was valued at USD 1.1 billion and is projected to grow at a CAGR of 5.7% through 2034 fueled by the rising demand for lightweight and cost-effective materials, particularly in industries such as consumer electronics, augmented reality/virtual reality (AR/VR), and medical devices. These materials offer the perfect balance of strength and flexibility, making them ideal for the miniaturized components in these fast-evolving sectors. As technological advancements push for smaller, more efficient products, the adoption of metal-metalloid glasses is expected to accelerate across various applications.

The ribbons segment, valued at USD 700 million in 2024, is also projected to experience a growth rate of 5.1% through 2034, attributed to their exceptional magnetic properties, which make them particularly suitable for use in transformers and magnetic sensors. As the demand for advanced electronic systems, energy-efficient equipment, and more precise sensor technologies increases, ribbons made from metallic glasses will continue to play a crucial role in these applications. Their ability to perform under demanding conditions while maintaining high performance makes them an asset for industries focusing on power generation, energy distribution, and high-tech sensing technologies.

U.S. Metallic Glasses Market was valued at USD 530 million in 2024, with a projected growth rate of 6% CAGR from 2025 to 2034, driven by the growing demand for metallic glasses in aerospace, defense systems, and electronics. Close collaboration between manufacturers and defense contractors is expediting the development and distribution of new metallic glass solutions. Additionally, research institutions in the U.S. are playing a vital role in advancing new alloys and optimizing production processes, which further supports the market's expansion.

Key companies in the Global Metallic Glasses Market include Heraeus Holding GmbH, Liquidmetal Technologies Inc., Materion Corporation, Usha Amorphous Metals Limited, and Hitachi Metals Ltd. To strengthen their presence, companies in the metallic glasses market focus on expanding production capabilities and refining manufacturing processes to reduce costs. Strategic partnerships and collaborations with research institutions and other industry players are helping accelerate innovation and the introduction of new materials. Manufacturers invest in technological advancements, such as additive manufacturing and advanced alloy development, to meet the growing demand for high-performance materials across various industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Market definition and evolution

- 3.1.1 Definition and classification of metallic glasses

- 3.1.2 Historical development of metallic glasses

- 3.1.3 Material composition and properties

- 3.1.3.1 Atomic structure and characteristics

- 3.1.3.2 Mechanical properties

- 3.1.3.3 Magnetic properties

- 3.1.3.4 Corrosion resistance

- 3.1.3.5 Thermal properties

- 3.1.4 Manufacturing processes

- 3.1.4.1 Rapid solidification techniques

- 3.1.4.2 Melt spinning

- 3.1.4.3 Gas atomization

- 3.1.4.4 Suction casting

- 3.1.4.5 Additive manufacturing

- 3.1.5 Comparative analysis: metallic glasses vs. Conventional materials

- 3.1.5.1 Metallic glasses vs. Crystalline metals

- 3.1.5.2 Metallic glasses vs. Ceramics

- 3.1.5.3 Metallic glasses vs. Polymers

- 3.1.6 Technological advancements in metallic glasses

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (hs code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Regulatory landscape and standards

- 3.5.1 Global regulatory framework

- 3.5.2 Regional regulatory frameworks

- 3.5.2.1 North America

- 3.5.2.1.1 Fda regulations (for medical applications)

- 3.5.2.1.2 Astm standards

- 3.5.2.1.3 Other relevant regulations

- 3.5.2.2 Europe

- 3.5.2.2.1 Eu medical device regulation (mdr)

- 3.5.2.2.2 Ce marking requirements

- 3.5.2.2.3 Reach regulations

- 3.5.2.3 Asia-pacific

- 3.5.2.3.1 China's regulations

- 3.5.2.3.2 Japan's regulations

- 3.5.2.3.3 Other regional regulations

- 3.5.2.4 Rest of the world

- 3.5.2.1 North America

- 3.5.3 Product certification and standards

- 3.5.3.1 Quality standards

- 3.5.3.2 Safety standards

- 3.5.3.3 Performance standards

- 3.5.4 Compliance challenges and strategies

- 3.5.5 Future regulatory trends and their implications

- 3.6 Market dynamics

- 3.6.1 Market drivers

- 3.6.1.1 Superior material properties

- 3.6.1.2 Increasing demand in electronics and energy sectors

- 3.6.1.3 Advancements in manufacturing technologies

- 3.6.1.4 Growing applications in biomedical field

- 3.6.2 Market restraints

- 3.6.2.1 High production costs

- 3.6.2.2 Limited size and shape capabilities

- 3.6.2.3 Brittleness and limited ductility

- 3.6.2.4 Competition from conventional materials

- 3.6.3 Market opportunities

- 3.6.3.1 Emerging applications in aerospace and defense

- 3.6.3.2 Advancements in additive manufacturing

- 3.6.3.3 Growing demand for sustainable materials

- 3.6.3.4 Expansion in developing economies

- 3.6.4 Market challenges

- 3.6.4.1 Scaling up production

- 3.6.4.2 Achieving consistent quality

- 3.6.4.3 Regulatory compliance

- 3.6.4.4 Market awareness and acceptance

- 3.6.1 Market drivers

- 3.7 Porter's five forces analysis

- 3.8 Pestle analysis

- 3.9 Value chain analysis

- 3.9.1 Raw material suppliers

- 3.9.2 Manufacturers

- 3.9.3 Distributors

- 3.9.4 End users

- 3.10 Environmental, social, and governance (esg) analysis

- 3.10.1 Environmental impact assessment

- 3.10.1.1 Carbon footprint analysis

- 3.10.1.2 Life cycle assessment (lca)

- 3.10.1.3 Waste management and recycling

- 3.10.1.4 Energy consumption in production

- 3.10.2 Social implications

- 3.10.2.1 Labor practices and working conditions

- 3.10.2.2 Community impact and engagement

- 3.10.2.3 Health and safety considerations

- 3.10.3 Governance and ethical considerations

- 3.10.3.1 Corporate governance practices

- 3.10.3.2 Ethical supply chain management

- 3.10.3.3 Transparency and reporting

- 3.10.4 Esg performance benchmarking of key players

- 3.10.5 Esg risk assessment and mitigation strategies

- 3.10.6 Future esg trends in the metallic glasses industry

- 3.10.1 Environmental impact assessment

- 3.11 Manufacturing and production analysis

- 3.11.1 Manufacturing process overview

- 3.11.1.1 Raw material procurement and preparation

- 3.11.1.2 Alloy melting and homogenization

- 3.11.1.3 Rapid solidification techniques

- 3.11.1.4 Post-processing and finishing

- 3.11.1.5 Quality control and testing

- 3.11.2 Production cost analysis

- 3.11.2.1 Raw material costs

- 3.11.2.2 Energy costs

- 3.11.2.3 Labor costs

- 3.11.2.4 Manufacturing overheads

- 3.11.2.5 Cost optimization strategies

- 3.11.3 Manufacturing facilities analysis

- 3.11.3.1 Key manufacturing locations

- 3.11.3.2 Production capacity assessment

- 3.11.3.3 Facility expansion plans

- 3.11.4 Supply chain challenges and solutions

- 3.11.5 Sustainability in manufacturing processes

- 3.11.5.1 Energy efficiency measures

- 3.11.5.2 Waste reduction strategies

- 3.11.5.3 Eco-friendly materials and processes

- 3.11.1 Manufacturing process overview

- 3.12 Consumer behavior and market trends analysis

- 3.12.1 Consumer preferences and purchasing patterns

- 3.12.2 Factors influencing purchase decisions

- 3.12.2.1 Performance and quality

- 3.12.2.2 Cost considerations

- 3.12.2.3 Sustainability factors

- 3.12.2.4 Brand reputation

- 3.12.3 Industry-specific adoption trends

- 3.12.3.1 Electronics industry adoption

- 3.12.3.2 Automotive industry adoption

- 3.12.3.3 Medical industry adoption

- 3.12.3.4 Aerospace industry adoption

- 3.12.4 Regional variations in consumer behavior

- 3.12.5 Impact of digital transformation on consumer engagement

- 3.12.6 Future consumer trends and their implications

- 3.13 Technological landscape and innovation analysis

- 3.13.1 Current technological trends in metallic glasses

- 3.13.2 Emerging technologies and their potential impact

- 3.13.2.1 Advanced manufacturing techniques

- 3.13.2.2 Novel alloy compositions

- 3.13.2.3 Surface modification technologies

- 3.13.2.4 Composite metallic glasses

- 3.13.3 R&d activities and innovation hubs

- 3.13.4 Technology adoption trends across applications

- 3.13.5 Technology readiness assessment

- 3.13.6 Future technology roadmap 2025-2034

- 3.14 Pricing analysis and economic factors

- 3.14.1 Pricing trends analysis

- 3.14.1.1 Historical price trends

- 3.14.1.2 Current pricing scenario

- 3.14.1.3 Price forecast

- 3.14.2 Factors affecting pricing

- 3.14.2.1 Raw material costs

- 3.14.2.2 Production complexity

- 3.14.2.3 Scale of production

- 3.14.2.4 Market competition

- 3.14.2.5 Application-specific requirements

- 3.14.3 Regional price variations

- 3.14.4 Price-value relationship analysis

- 3.14.5 Economic indicators impacting the market

- 3.14.5.1 Gdp growth and industrial production

- 3.14.5.2 R&d spending

- 3.14.5.3 Metal commodity prices

- 3.14.5.4 Energy costs

- 3.14.6 Pricing strategies of key market players

- 3.14.1 Pricing trends analysis

- 3.15 Raw materials and supply chain analysis

- 3.15.1 Key raw materials overview

- 3.15.1.1 Metals and metalloids

- 3.15.1.2 Rare earth elements

- 3.15.1.3 Other critical materials

- 3.15.2 Raw material sourcing and procurement

- 3.15.2.1 Global supply sources

- 3.15.2.2 Supply concentration and risks

- 3.15.2.3 Sustainable sourcing initiatives

- 3.15.3 Supply chain structure and dynamics

- 3.15.3.1 Upstream supply chain

- 3.15.3.2 Midstream processing

- 3.15.3.3 Downstream distribution

- 3.15.4 Supply chain challenges

- 3.15.4.1 Raw material availability and criticality

- 3.15.4.2 Price volatility

- 3.15.4.3 Geopolitical factors

- 3.15.4.4 Logistics and transportation

- 3.15.5 Supply chain risk mitigation strategies

- 3.15.6 Future trends in raw materials and supply chain

- 3.15.1 Key raw materials overview

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis of key players

- 4.2 Competitive positioning matrix

- 4.3 Competitive strategies adopted by key players

- 4.3.1 Product innovation and development

- 4.3.2 Mergers and acquisitions

- 4.3.3 Partnerships and collaborations

- 4.3.4 Expansion strategies

- 4.4 Investment analysis and market attractiveness

- 4.4.1 Current investment scenario

- 4.4.2 Investment opportunities by segment

- 4.4.3 Investment opportunities by region

- 4.4.4 Roi analysis

- 4.4.5 Venture capital and private equity landscape

- 4.4.6 M&a activity analysis

- 4.4.7 Future investment outlook

- 4.5 Risk assessment and mitigation strategies

- 4.5.1 Market risks

- 4.5.2 Technological risk

- 4.5.3 Regulatory risks

- 4.5.4 Competitive risks

- 4.5.5 Supply chain risks

- 4.5.6 Environmental and sustainability risks

- 4.5.7 Risk mitigation strategies

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Metal-metal metallic glasses

- 5.3 Metal-metalloid metallic glasses

Chapter 6 Market Estimates and Forecast, By Form, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Ribbons

- 6.3 Wires

- 6.4 Powders

- 6.5 Sheets

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Material Composition, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Iron-based

- 7.3 Zirconium-based

- 7.4 Titanium-based

- 7.5 Copper-based

- 7.6 Palladium-based

- 7.7 Magnesium-based

- 7.8 Aluminum-based

- 7.9 Other compositions

Chapter 8 Market Estimates and Forecast, By Manufacturing Process, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Extremely rapid cooling

- 8.3 Physical vapor deposition

- 8.4 Solid-state reaction

- 8.5 Ion irradiation

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Electronics and electrical

- 9.3 Automotive and transportation

- 9.4 Aerospace and defense

- 9.5 Medical and healthcare

- 9.6 Sports and leisure

- 9.7 Energy

- 9.8 Industrial equipment

- 9.9 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amorphology Inc.

- 11.2 Antai Technology Co., Ltd.

- 11.3 EPSON ATMIX Corporation

- 11.4 Exmet AB

- 11.5 Glassimetal Technology

- 11.6 Heraeus Holding

- 11.7 Hitachi Metals Ltd.

- 11.8 Liquidmetal Technologies Inc.

- 11.9 Materion Corporation

- 11.10 PrometalTech

- 11.11 PX Group SA

- 11.12 Qingdao Yunlu Advanced Materials Technology Co., Ltd.

- 11.13 RS Alloys

- 11.14 Usha Amorphous Metals Limited