|

시장보고서

상품코드

1755198

정제 유당 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Refined Lactose Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

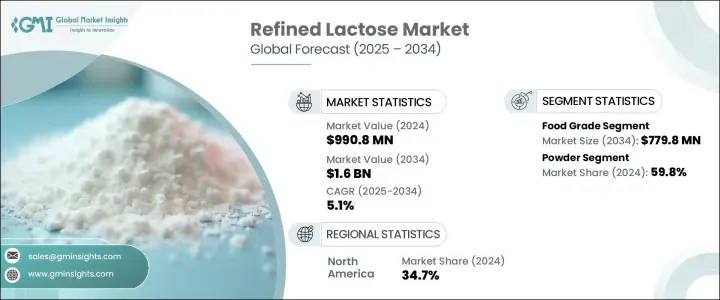

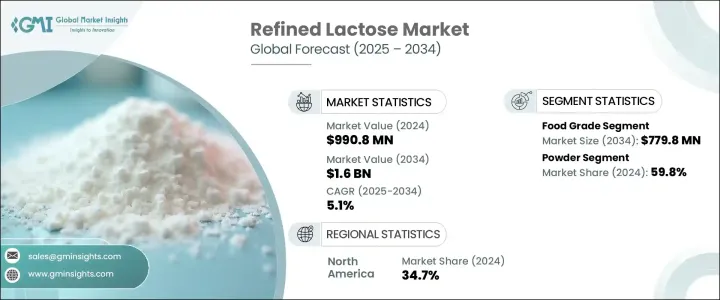

정제 유당 세계 시장은 2024년에는 9억 9,080만 달러로 평가되었으며, 음식, 의약품, 동물사료 등 다양한 산업에서 수요 증가를 배경으로 CAGR 5.1%로 성장해 2034년에는 16억 달러에 달할 것으로 예측되고 있습니다.

식품 분야에서는 정제 유당은 베이커리 제품, 과자류, 유제품의 감미료나 충전제로 이용되고 있습니다. 향료로 자리매김하고, 정제 유당 수요를 한층 더 촉진하고 있습니다. 의약품에서는 정제 유당은 압축성과 용해성이 뛰어나기 때문에 정제나 캡슐제의 부형제로서 사용되어 시장의 확대에 공헌하고 있습니다.

게다가, 정제 유당을 동물용 사료(특히 돼지나 송아지 등의 어린 가축용)에 배합하는 것으로, 소화기 건강을 촉진해, 초기의 에너지 대사를 서포트하는 높은 효과가 증명되고 있습니다. 축우의 건강과 급속한 성장이 경제적인 존속에 불가결한 축산 및 낙농 분야에서의 채택의 원동력이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 9억 9,080만 달러 |

| 예측 금액 | 16억 달러 |

| CAGR | 5.1% |

식품 등급 분야는 가공 식품에서 깨끗한 라벨의 천연 유래 원료에 대한 소비자 수요 증가에 힘입어 CAGR 5.2%로 성장하여 2034년까지 7억 7,980만 달러에 달할 것으로 예측됩니다. 사용 중인 베이커리, 과자류, 유제품의 사용량 증가는 제형화 및 기능성 식품 개발의 혁신과 함께 예측 기간을 통해 이 부문의 지속적인 기세를 촉진할 것으로 예측됩니다.

정제 유당의 다양한 형태 중에서 분말형태는 2024년에 59.8%를 차지하여 최대 시장 점유율을 차지하며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 6.8%로 성장할 것으로 예측됩니다. 분말 형태는 범용성이 높고 취급이 용이하기 때문에 의약품, 식음료, 유아 영양 등 다양한 용도에 적합합니다.

북미의 정제 유당 시장은 2024년에 34.7%의 점유율을 차지했지만, 이는 이 지역의 낙농 부문이 발전하고 있어 의약품 용도로 유당의 요구가 높아지고 있기 때문입니다. 미국은 정교한 생산 능력과 유당 정제를 위한 연구개발에 대한 높은 투자로 이 지역 시장 점유율에 크게 공헌하고 있습니다. 또한, 의약품 제제에 있어서의 유당 기반의 부형제의 사용이 증가하고 있는 것도 이 지역 시장 성장을 뒷받침하고 있습니다.

세계의 정제 유당 시장의 주요 기업은 Arla Foods Ingredients Group P/S, Fonterra Co-operative Group Limited, Lactalis Ingredients, FrieslandCampina Ingredients, Agropur Cooperative, Hilmar Cheese Company, Inc. 등입니다. 이러한 기업은 제품 포트폴리오의 확대, 생산 능력의 강화, 연구 개발에 대한 투자에 주력해, 다양한 용도에 있어서의 정제 유당 수요 증가에 대응하고 있습니다. 글로벌 정제 유당 산업의 기업들은 시장 입지를 강화하기 위해 중요한 전략을 채용하고 있습니다. 이것에는 수요 증가에 대응하기 위한 생산 능력의 확대, 제품 품질의 혁신과 향상을 위한 연구 개발에 대한 투자, 유통망과 시장 리치를 강화하기 위한 전략적 파트너십이나 협력 관계의 구축 등이 포함됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 주요 제조업체

- 리셀러

- 업계 전체의 이익률

- 공급망과 유통분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국, 2021년-2024년

- 주요 수출국, 2021년-2024년

참고: 위의 무역 통계는 주요 국가에만 제공됩니다.

- 영향요인

- 성장 촉진요인

- 식품 및 음료 업계 수요 증가

- 건강과 웰빙 동향

- 제약 업계 수요

- 동물사료 산업의 확대

- 업계의 잠재적 위험 및 과제

- 유당 불내증 증가

- 원재료 가격 변동

- 시장 기회

- 시장의 과제

- 시장 기회

- 성장 촉진요인

- 원재료의 정세

- 제조업의 동향

- 기술의 진화

- 가격 분석과 비용 구조

- 가격 동향(달러/톤)

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 가격요인(원재료, 에너지, 노동력)

- 지역별 가격 차이

- 코스트 구조의 내역

- 수익성 분석

- 가격 동향(달러/톤)

- 규제 프레임워크과 기준

- 식품안전규제

- 의약품 품질 기준

- 유아용 조제 분유 규제

- 라벨 요건

- 수출입 규제

- Porter's Five Forces 분석

- PESTEL 분석

- 제조 공정 분석

- 유청 가공

- 결정화 기술

- 정제방법

- 건조와 분쇄

- 품질 관리 절차

- 원재료 분석 및 조달 전략

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 히트맵 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

- Expansion

- Mergers &acquisition

- Collaborations

- New product launches

- Research &development

- 주요 기업에 의한 최근의 동향과 영향 분석

- 기업 분류

- 참가자의 개요

- 재무실적

- 제품 벤치마킹

제5장 시장 추정 및 예측 : 그레이드별, 2021년-2034년

- 주요 동향

- 식품 등급

- 표준 식품 등급

- 고순도 식품 등급

- 기타 식품 등급

- 의약품 등급

- USP/EP/JP등급

- 무수 유당

- 스프레이 건조 유당

- 일수화 유당

- 기타 의약품 등급

- 테크니컬 그레이드

- 기타 등급

제6장 시장 추정 및 예측 : 형태별, 2021년-2034년

- 주요 동향

- 분말

- 미분말

- 조분

- 과립

- 분쇄 과립

- 응집 과립

- 크리스탈

- 기타 형태

제7장 시장 추정 및 예측 : 제조 방법별, 2021년-2034년

- 주요 동향

- 유청 유래 유당

- 스위트 유청 유래

- 산성 유청 유래

- 우유 유래의 유당

- 기타 제조방법

제8장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 식품?음료

- 과자류

- 베이커리 제품

- 유제품

- 가공식품

- 음료

- 기타 식품 용도

- 의약품

- 정제 제제(부형제)

- 캡슐 제형

- 흡입제품

- 주사제

- 기타 의약품 용도

- 유아용 조제 분유

- 표준 유아용 조제 분유

- 후속 포뮬러

- 특별한 처방

- 기타 유아 영양 제품

- 동물사료

- 화장품 및 퍼스널케어

- 기타 용도

제9장 시장 추정 및 예측 : 최종 이용 산업별, 2021년-2034년

- 주요 동향

- 식품 및 음료 업계

- 주요 식품 제조업체

- 중형 및 소형 푸드 프로세서

- 장인에 의한 식품 생산자

- 제약업계

- 주요 제약 회사

- 제네릭 의약품 제조업체

- 계약 제조 조직

- 유아용 조제 분유 제조업체

- 동물사료 산업

- 화장품 및 퍼스널케어 업계

- 기타 최종 이용 산업

제10장 시장 추정 및 예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 직접 판매/B2B

- 리셀러 및 도매업체

- 온라인 채널

- 기타 유통 채널

제11장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Arla Foods Ingredients Group P/S

- Fonterra Co-operative Group Limited

- Lactalis Ingredients

- FrieslandCampina Ingredients

- Agropur Cooperative

- Hilmar Cheese Company, Inc.

- Leprino Foods Company

- Meggle Group GmbH

- DFE Pharma

- Kerry Group plc

- Milei GmbH(Hochdorf Group)

- Molkerei MEGGLE Wasserburg GmbH &Co. KG

- Actus Nutrition

The Global Refined Lactose Market was valued at USD 990.8 million in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 1.6 billion by 2034, driven by increasing demand across various industries, including food and beverage, pharmaceuticals, and animal feed. In the food sector, refined lactose is utilized as a sweetener and filler in bakery items, confectioneries, and dairy products. Consumers' preference for natural and minimally processed ingredients has further fueled the demand for refined lactose, positioning it as a healthier alternative to synthetic sweeteners. In pharmaceuticals, refined lactose serves as an excipient in tablet and capsule formulations due to its excellent compressibility and solubility, contributing to the expansion of the market.

Additionally, incorporating refined lactose into animal feed formulations-especially for young livestock such as piglets and calves-has proven highly effective in promoting digestive health and supporting early-stage energy metabolism. This functional benefit drives its adoption in the livestock and dairy farming sectors, where animal health and rapid growth are critical for economic viability. As producers aim to improve feed efficiency and minimize synthetic additives, lactose is a natural, palatable, and nutrient-rich component.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $990.8 Million |

| Forecast Value | $1.6 Billion |

| CAGR | 5.1% |

The food-grade segment is projected to reach USD 779.8 million by 2034, growing at a CAGR of 5.2% fueled by increasing consumer demand for clean-label, naturally derived ingredients in processed foods. Food-grade lactose is widely used not only for its mild sweetness and textural properties but also due to its digestibility and essential role in infant nutrition. Its rising usage in bakery, confectionery, and dairy products-coupled with innovation in formulation and functional food development-is expected to drive sustained momentum in this segment throughout the forecast period.

Among the various forms of refined lactose, the powder form held the largest market share, accounting for 59.8% in 2024, and is projected to grow at a CAGR of 6.8% from 2025 to 2034. The powder form's versatility and ease of handling make it suitable for various applications in pharmaceuticals, food and beverage industries, and infant nutrition. However, challenges such as fluctuating raw material prices and the requirement for consistent quality standards may impact growth. Innovations in processing techniques to enhance purity and performance are expected to drive the continued expansion of the refined lactose market.

North America Refined Lactose Market held a 34.7% share in 2024 due to the region's developed dairy sector and the growing need for lactose in pharmaceutical applications. The United States significantly contributes to this region's market share, owing to its sophisticated production capabilities and high investment in research and development for refining lactose. Additionally, the increasing use of lactose-based excipients in drug formulations continues to bolster market growth in this region.

Key players in the Global Refined Lactose Market include Arla Foods Ingredients Group P/S, Fonterra Co-operative Group Limited, Lactalis Ingredients, FrieslandCampina Ingredients, Agropur Cooperative, and Hilmar Cheese Company, Inc. These companies are focusing on expanding their product portfolios, enhancing production capacities, and investing in research and development to meet the rising demand for refined lactose across various applications. To strengthen their market presence, companies in the Global Refined Lactose Industry are adopting several key strategies. These include expanding production capacities to meet the growing demand, investing in research and development to innovate and improve product quality, and forming strategic partnerships and collaborations to enhance distribution networks and market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.1.4 Supply chain and distribution analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major exporting countries, 2021-2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only

- 3.4 Impact forces

- 3.4.1 Growth drivers

- 3.4.1.1 Rising demand in food & beverage industry

- 3.4.1.2 Health & wellness trends

- 3.4.1.3 Pharmaceutical industry demand

- 3.4.1.4 Expansion in animal feed industry

- 3.4.2 Industry pitfalls & challenges

- 3.4.2.1 Increasing lactose intolerance

- 3.4.2.2 Raw material price fluctuations

- 3.4.3 Market opportunities

- 3.4.4 Market challenges

- 3.4.5 Market opportunity

- 3.4.1 Growth drivers

- 3.5 Raw material landscape

- 3.5.1 Manufacturing trends

- 3.5.2 Technology evolution

- 3.6 Pricing analysis and cost structure

- 3.6.1 Pricing trends (USD/Ton)

- 3.6.1.1 North America

- 3.6.1.2 Europe

- 3.6.1.3 Asia Pacific

- 3.6.1.4 Latin America

- 3.6.1.5 Middle East Africa

- 3.6.2 Pricing factors (raw materials, energy, labor)

- 3.6.3 Regional price variations

- 3.6.4 Cost structure breakdown

- 3.6.5 Profitability analysis

- 3.6.1 Pricing trends (USD/Ton)

- 3.7 Regulatory framework and standards

- 3.7.1 Food safety regulations

- 3.7.2 Pharmaceutical quality standards

- 3.7.3 Infant formula regulations

- 3.7.4 Labeling requirements

- 3.7.5 Import/Export regulations

- 3.8 Porter's analysis

- 3.9 Pestel analysis

- 3.10 Manufacturing process analysis

- 3.10.1 Whey processing

- 3.10.2 Crystallization techniques

- 3.10.3 Purification methods

- 3.10.4 Drying & milling

- 3.10.5 Quality control procedures

- 3.11 Raw material analysis & procurement strategies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.6.1 Expansion

- 4.6.2 Mergers & acquisition

- 4.6.3 Collaborations

- 4.6.4 New product launches

- 4.6.5 Research & development

- 4.7 Recent developments & impact analysis by key players

- 4.7.1 Company categorization

- 4.7.2 Participant’s overview

- 4.7.3 Financial performance

- 4.8 Product benchmarking

Chapter 5 Market Estimates & Forecast, By Grade, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Food grade

- 5.2.1 Standard food grade

- 5.2.2 High purity food grade

- 5.2.3 Other food grades

- 5.3 Pharmaceutical Grade

- 5.3.1 USP/EP/JP grade

- 5.3.2 Anhydrous lactose

- 5.3.3 Spray-dried lactose

- 5.3.4 Monohydrate lactose

- 5.3.5 Other pharmaceutical grades

- 5.4 Technical grade

- 5.5 Other grades

Chapter 6 Market Estimates & Forecast, By Form, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder

- 6.2.1 Fine powder

- 6.2.2 Coarse powder

- 6.3 Granules

- 6.3.1 Milled granules

- 6.3.2 Agglomerated granules

- 6.4 Crystals

- 6.5 Other forms

Chapter 7 Market Estimates & Forecast, By Production Method, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Whey-derived lactose

- 7.2.1 Sweet whey-derived

- 7.2.2 Acid whey-derived

- 7.3 Milk-derived lactose

- 7.4 Other production methods

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.2.1 Confectionery

- 8.2.2 Bakery products

- 8.2.3 Dairy products

- 8.2.4 Processed foods

- 8.2.5 Beverages

- 8.2.6 Other food applications

- 8.3 Pharmaceuticals

- 8.3.1 Tablet formulations (excipient)

- 8.3.2 Capsule formulations

- 8.3.3 Inhalation products

- 8.3.4 Injectable formulations

- 8.3.5 Other pharmaceutical applications

- 8.4 Infant formula

- 8.4.1 Standard infant formula

- 8.4.2 Follow-on formula

- 8.4.3 Specialty formula

- 8.4.4 Other infant nutrition products

- 8.5 Animal feed

- 8.6 Cosmetics & personal care

- 8.7 Other applications

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Food & beverage industry

- 9.2.1 Large food manufacturers

- 9.2.2 Medium & small food processors

- 9.2.3 Artisanal food producers

- 9.3 Pharmaceutical industry

- 9.3.1 Large pharmaceutical companies

- 9.3.2 Generic drug manufacturers

- 9.3.3 Contract manufacturing organizations

- 9.4 Infant formula manufacturers

- 9.4.1 Animal feed industry

- 9.4.2 Cosmetics & personal care industry

- 9.4.3 Other end-use industries

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct sales/B2B

- 10.3 Distributors & wholesalers

- 10.4 Online channels

- 10.5 Other distribution channels

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Arla Foods Ingredients Group P/S

- 12.2 Fonterra Co-operative Group Limited

- 12.3 Lactalis Ingredients

- 12.4 FrieslandCampina Ingredients

- 12.5 Agropur Cooperative

- 12.6 Hilmar Cheese Company, Inc.

- 12.7 Leprino Foods Company

- 12.8 Meggle Group GmbH

- 12.9 DFE Pharma

- 12.10 Kerry Group plc

- 12.11 Milei GmbH (Hochdorf Group)

- 12.12 Molkerei MEGGLE Wasserburg GmbH & Co. KG

- 12.13 Actus Nutrition