|

시장보고서

상품코드

1755203

신경 기기 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Neurology Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

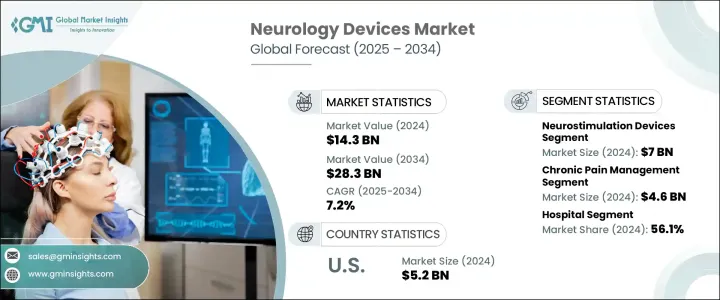

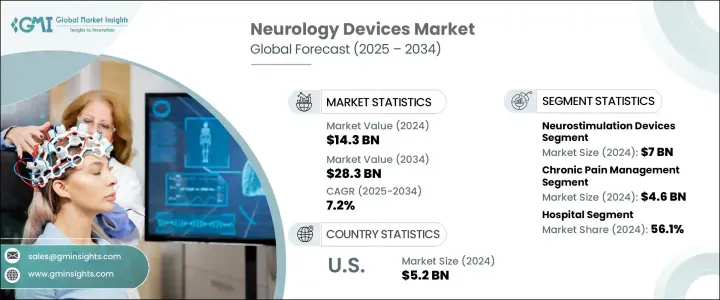

세계 신경 기기 시장은 2024년 143억 달러로 평가되었으며, 기술 혁신, 신경질환 발생률 상승, 헬스케어 지출 증가, 의료서비스 접근성 개선 등이 결합되어 CAGR 7.2%로 성장해 2034년 283억 달러에 이를 것으로 추정되고 있습니다.

AI를 활용한 원격 모니터링과 브레인 컴퓨터 인터페이스 시스템의 개발로 환자의 치료 성적이 대폭 향상되고 있습니다. 이러한 진보는 보다 정확하고 안전하며 효율적인 치료 개입을 가능하게 하며, 신경 기기 분야 전체의 확대에 기여하고 있습니다.

신경 기기는 뇌, 척추, 말초 신경과 같은 신경계에 영향을 미치는 상태를 관리하는 데 사용되는 이식 가능한 도구, 수술 도구, 진단 기술을 포함합니다. 이 장치들은 뇌전증, 파킨슨병, 알츠하이머병, 다발성 경화증, 뇌종양 및 외상성 뇌 손상을 포함한 신경 질환의 발견, 모니터링, 치료 및 재활을 돕기 위해 설계되었습니다. 일상적인 신경학적 평가에서 복잡한 신경외과적 치료에 이르기까지 다양한 임상 장면에서 중요한 역할을 담당하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 143억 달러 |

| 예측 금액 | 283억 달러 |

| CAGR | 7.2% |

주요 카테고리 중 신경 자극 장치 부문은 2024년에 70억 달러를 생산했습니다. 폐쇄형 루프 시스템, MRI 대응 임플란트, 소형화 솔루션 등의 새로운 모델은 환자의 결과를 개선하고 치료 용도를 넓혀 이 부문의 성장을 강화하고 있습니다.

최종 용도별로 병원은 종합적인 인프라와 복잡한 신경학적 사례에 대한 대응 능력을 배경으로 2024년 시장을 56.1%의 압도적인 점유율로 견인했습니다. 병원은 진단이나 치료 처치의 대부분을 실시하기 때문에 신경 화상 진단 시스템이나 신경 조절 시스템의 도입에 있어서 중요한 거점이 되고 있습니다. 발작, 뇌졸중, 외상 등 신경학적 긴급 사태를 관리하는 역할을 담당하고 있기 때문에 최첨단 장비에 대한 수요는 끊임없이 높아지고 있습니다.

미국의 신경 기기 2024년 시장 규모는 52억 달러로, 신경질환 유병률 증가, 견고한 임상연구 인프라, 정부의 엄청난 자금 지원을 지원하고 있습니다. 주요 연방 정부의 이니셔티브와 연구 보조금은 신경 보철과 브레인 컴퓨터 인터페이스 시스템의 진보를 계속 지원합니다. 노인 인구 증가와 신경학의 전문가 부족도, 증가하는 케어 수요에 대응하기 위해, 선진 기기에의 의존도를 높이고 있습니다.

신경 기기 업계 정세를 적극적으로 형성하는 주요 기업은 Synchron, B BRAUN, LivaNova, NeuroPace, ZYLOX TONBRIDGE, Abbott Laboratories, MicroTransponder, KARL STROZ, Medtronic, stryker, Bioness, nevro, Boston Scientific, Enterra Medical, Paradromics 등 주요 기업은 신경 기기 시장에서의 지위를 강화하기 위해 연구 주도형 제품 혁신과 AI 통합 시스템 시장 개척에 주력하고 있습니다. 이러한 기업의 접근 방식의 중심이 되고 있습니다. 각 기업은 이미징 시스템과의 장비 호환성을 개선하고 보다 광범위한 임상 사용을 위해 컴팩트하고 휴대 가능한 형식을 추구하고 있습니다. 대기업은 제조 능력을 확대하고, 계약을 확보하고, 지리적 존재를 높이고, 보다 스마트한 신경학적 케어의 제공을 목표로 하는 헬스 케어 시스템과 연계하기 위해, 세계적인 협력 관계를 맺고자 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 신경질환의 유병률 상승

- 저침습 수술의 채용 증가

- 기술적 진보

- 자금과 투자 증가

- 업계의 잠재적 위험 및 과제

- 장비 및 절차의 높은 비용

- 디바이스의 고장이나 합병증의 위험

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 미국

- 유럽

- 기술의 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 상환 시나리오

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

- 장래 시장 동향

- 밸류체인 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 디바이스별, 2021년-2034년

- 주요 동향

- 신경 자극 장치

- 척수 자극 장치

- 뇌심부 자극장치

- 미주 신경 자극 장치

- 천골신경자극장치

- 위 전기 자극 장치

- 뇌신경외과용 기기

- 정위 방사선 치료 시스템

- 신경 내시경

- 초음파 흡입기

- 동맥류 클립

- 개입적 신경 기기

- 동맥류 코일 색전술

- 색전 코일

- 유량전환장치

- 액체 색전 시약

- 신경 혈전 제거술

- 혈전 제거기

- 흡입흡입장치

- 스네어 장치

- 신경혈관 카테터

- 마이크로카테터

- 마이크로 가이드와이어

- 뇌풍선 혈관성형술 및 스텐트

- 경동맥 스텐트

- 필터 디바이스

- 풍선 폐색 장치

- CSF 관리 장치

- 뇌 션트

- 뇌외 배수원

- 동맥류 코일 색전술

- 뇌 컴퓨터 인터페이스 장치

- 비침습성 BCI

- 부분 침습성 BCI

- 완전 침습성 BCI

- 기타 디바이스

제6장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 만성 통증 관리

- 파킨슨병

- 간질

- 뇌졸중의 관리와 회복

- 알츠하이머병

- 기타 용도

제7장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제8장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott Laboratories

- B BRAUN

- Bioness

- Boston Scietific

- enterra medical

- KARL STROZ

- LivaNova

- Medtronic

- MicroTransponder

- NeuroPace

- nevro

- Paradromics

- stryker

- synchron

- ZYLOX TONBRIDGE

The Global Neurology Devices Market was valued at USD 14.3 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 28.3 billion by 2034, fueled by a combination of technological innovation, rising rates of neurological conditions, increased healthcare spending, and improved access to medical services. Developments in AI-powered remote monitoring and brain-computer interface systems have significantly improved patient care outcomes. In addition, emerging minimally invasive neurotechnologies-such as portable EEG monitors and enhanced stimulation systems-are transforming neurological treatment and diagnosis. These advances have made it possible to deliver more precise, safer, and efficient therapeutic interventions, contributing to the overall expansion of the neurology devices sector. Neurology devices include implantable tools, surgical instruments, and diagnostic technologies used to manage conditions affecting the nervous system, such as the brain, spine, and peripheral nerves.

Neurology devices include implantable tools, surgical instruments, and diagnostic technologies used to manage conditions affecting the nervous system, such as the brain, spine, and peripheral nerves. These devices are designed to aid in the detection, monitoring, treatment, and rehabilitation of neurological disorders, including epilepsy, Parkinson's disease, Alzheimer's disease, multiple sclerosis, brain tumors, and traumatic brain injuries. They serve a critical role across a range of clinical settings, from routine neurological assessments to complex neurosurgical procedures. Diagnostic tools such as EEG systems and neuroimaging technologies help in the early and accurate identification of neurological conditions, while implantable devices like neurostimulators offer long-term therapeutic benefits for patients suffering from chronic and progressive diseases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.3 Billion |

| Forecast Value | $28.3 Billion |

| CAGR | 7.2% |

Among the main categories, the neurostimulation devices segment generated USD 7 billion in 2024. These include systems like spinal cord stimulators and vagus nerve stimulators, designed to address movement disorders, chronic pain, psychiatric issues, and epilepsy. Newer models, such as closed-loop systems, MRI-compatible implants, and miniaturized solutions, have improved patient outcomes and broadened therapeutic applications, reinforcing growth in this segment.

By end use, hospitals led the market in 2024 with a dominant share of 56.1%, driven by their comprehensive infrastructure and ability to handle complex neurological cases. Hospitals conduct a majority of diagnostic and therapeutic procedures, making them key hubs for the adoption of neuroimaging and neuromodulation systems. Their role in managing emergency neurological events such as seizures, strokes, and traumatic injuries ensures constant demand for cutting-edge equipment.

United States Neurology Devices Market was valued at USD 5.2 billion in 2024, supported by increasing neurological disease prevalence, robust clinical research infrastructure, and substantial government funding. Major federal initiatives and research grants continue to back advancements in neuroprosthetics and brain-computer interface systems. A growing elderly population and a shortage of specialized neurology professionals are also pushing greater reliance on advanced devices to meet the rising demand for care.

Key players actively shaping The Neurology Devices Industry landscape include Synchron, B BRAUN, LivaNova, NeuroPace, ZYLOX TONBRIDGE, Abbott Laboratories, MicroTransponder, KARL STROZ, Medtronic, stryker, Bioness, nevro, Boston Scientific, Enterra Medical, and Paradromics. To strengthen their position in the neurology devices market, leading companies are focusing on research-driven product innovation and the development of AI-integrated systems. These firms are expanding their portfolios with minimally invasive devices and patient-specific solutions that enhance safety and precision. Strategic partnerships, regulatory approvals, and increased investments in neurotechnology R&D are also central to their approach. Businesses are refining device compatibility with imaging systems and pursuing compact, portable formats for broader clinical use. Additionally, major players are scaling up manufacturing capabilities and entering into global collaborations to secure contracts, boost geographic presence, and align with healthcare systems aiming for smarter neurological care delivery.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of neurological disorders

- 3.2.1.2 Growing adoption of minimally invasive procedure

- 3.2.1.3 Technological advancements

- 3.2.1.4 Increased funding and investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and procedures

- 3.2.2.2 Risk of device failure and complications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Reimbursement scenario

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Gap analysis

- 3.11 Future market trends

- 3.12 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Device, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Neurostimulation devices

- 5.2.1 Spinal cord stimulators

- 5.2.2 Deep brain stimulators

- 5.2.3 Vagus nerve stimulators

- 5.2.4 Sacral nerve stimulators

- 5.2.5 Gastric electrical stimulators

- 5.3 Neurosurgical devices

- 5.3.1 Stereotactic systems

- 5.3.2 Neuroendoscopes

- 5.3.3 Ultrasonic aspirators

- 5.3.4 Aneurysm clips

- 5.4 Interventional neurology devices

- 5.4.1 Aneurysm coiling and embolisation

- 5.4.1.1 Embolic coils

- 5.4.1.2 Flow diversion devices

- 5.4.1.3 Liquid embolic reagents

- 5.4.2 Neurothromobectomy

- 5.4.2.1 Clot retrievers

- 5.4.2.2 Suction aspiration devices

- 5.4.2.3 Snare devices

- 5.4.3 Neurovascular catheters

- 5.4.3.1 Micro catheters

- 5.4.3.2 Micro guidewires

- 5.4.4 Cerebral balloon angioplasty and stents

- 5.4.4.1 Carotid artery stents

- 5.4.4.2 Filter devices

- 5.4.4.3 Balloon occlusion devices

- 5.4.5 Csf management devices

- 5.4.5.1 Cerebral shunts

- 5.4.5.2 Cerebral external drainage

- 5.4.1 Aneurysm coiling and embolisation

- 5.5 Brain-computer interface devices

- 5.5.1 Non-invasive BCI

- 5.5.2 Partially invasive BCI

- 5.5.3 Fully invasive BCI

- 5.6 Other devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chronic pain management

- 6.3 Parkinson’s disease

- 6.4 Epilepsy

- 6.5 Stroke management and recovery

- 6.6 Alzheimer

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 B BRAUN

- 9.3 Bioness

- 9.4 Boston Scietific

- 9.5 enterra medical

- 9.6 KARL STROZ

- 9.7 LivaNova

- 9.8 Medtronic

- 9.9 MicroTransponder

- 9.10 NeuroPace

- 9.11 nevro

- 9.12 Paradromics

- 9.13 stryker

- 9.14 synchron

- 9.15 ZYLOX TONBRIDGE