|

시장보고서

상품코드

1755249

3D 프린터 의지 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)3D Printed Prosthetics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

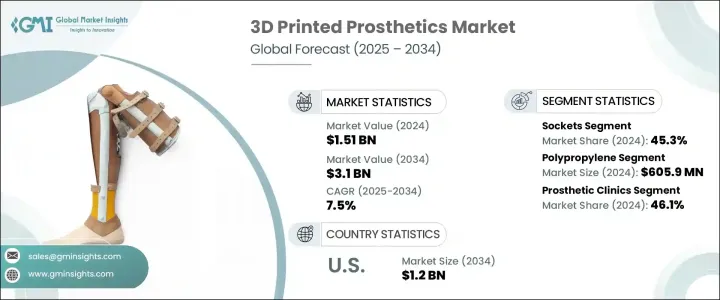

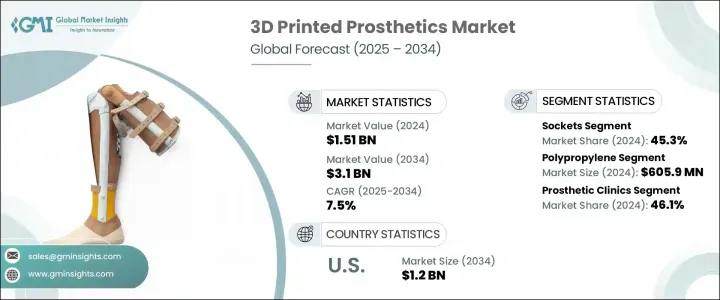

세계의 3D 프린터 의지 시장은 2024년에는 15억 1,000만 달러로 평가되었으며, 2034년에는 31억 달러에 이를 것으로 예측되며 CAGR 7.5%로 성장할 전망입니다.

종종 속도가 느리고 비용이 많이 들며 여러 번의 피팅이 필요한 기존의 제조 방법과 달리, 3D 프린팅 기술은 더 빠르고 비용 효율적인 접근 방식을 제공합니다. 이러한 맞춤형 솔루션은 생산 시간을 단축하면서 전반적인 사용자 경험을 개선합니다. 개인화는 성장에 따라 요구 사항이 자주 바뀌고 교체가 더 자주 필요한 소아 환자에게 특히 유용합니다. 보철 분야의 첨단 3D 프린팅은 개별화된 의료 기기에 대한 전 세계의 의료 수요를 충족하는 데 큰 도약입니다.

적층 제조 기술의 발전, 특히 스테레오리소그래피(SLA), 선택적 레이저 소결(SLS), 융합 적층 모델링(FDM)은 내구성이 뛰어나고 가벼우며 기능적인 의수 및 의족 부품의 제작을 가능하게 했습니다. 미국 식품의약국(FDA) 등 규제 기관의 승인을 받은 3D 프린팅 의수 및 의족 기기의 증가로 이 기술은 신뢰성과 확산 속도를 높이고 있습니다. 의료용 폴리머와 합금 등 생체적합성 재료의 가용성은 의수 의족 장치의 내구성, 편안함, 적응성을 더욱 향상시켰습니다. 이러한 혁신은 생산 주기를 단축할 뿐만 아니라 의수 의족의 품질과 정밀도를 높여 의료 전문가와 환자 모두에게 더 접근하기 쉬운 제품을 제공합니다.

| 시장 범위 | |

|---|---|

| 시장 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 15억 1,000만 달러 |

| 예측 금액 | 31억 달러 |

| CAGR | 7.5% |

폴리프로필렌은 유리한 강도 대 중량 비율, 피로 저항성 및 화학적 안정성으로 인해 2024년에 6억 590만 달러를 창출하며 재료 부문을 주도했습니다. 의료 제조에 널리 사용되는 폴리프로필렌은 생체 적합성과 살균에 대한 내성으로 높은 평가를 받고 있습니다. 보철 소켓, 수술용 가이드 및 정형용 지지대 제작에 광범위하게 사용됩니다. 3D 프린팅을 통한 경량화 및 개인 맞춤형 의료 솔루션에 대한 수요가 증가함에 따라 폴리프로필렌의 활용도 계속 확대되고 있습니다. 부드러움과 기능성이 조화를 이루는 폴리프로필렌은 환자 중심의 디자인에 선호되는 소재입니다.

보철 클리닉 부문은 2024년에 46.1%의 점유율을 차지했습니다. 이 전문 센터들은 만성 질환(당뇨병, 혈관 질환 등)으로 인한 절단 환자가 많은 지역에서 증가하는 환자 수를 관리하기 위해 3D 프린팅을 점점 더 통합하고 있습니다. 클리닉은 3D 프린팅의 효율성으로부터 혜택을 받으며, 특히 소아 환자에게 중요한 빠른 수정과 자주 교체가 가능합니다. 이러한 시설은 재활, 훈련, 후속 관리 서비스를 제공하는 원스톱 제공자로 기능하며, 3D 프린팅 인공 관절의 채택을 촉진합니다. 이러한 중앙 집중식 접근 방식은 사용자 경험을 단순화하고 장기적인 해결책을 찾는 환자들 사이에서 신뢰를 쌓아갑니다.

미국의 3D 프린터 의지 시장은 비만, 당뇨병, 말초 동맥 질환의 발병률 증가에 힘입어 2034년까지 12억 달러 규모로 성장할 것으로 예상되며, 이는 첨단 보철 솔루션에 대한 긴급한 필요성을 강조하고 있습니다. 원격 의료, 클라우드 기반 워크플로우, 원격 환자 스캐닝과 같은 디지털 건강 혁신의 통합은 3D 프린팅 보철물의 확장을 위한 유리한 토대를 마련하고 있습니다. 이러한 발전으로 의료진은 보다 정확하고 시기적절한 치료를 제공할 수 있게 되어 의료 분야의 미래에 더 널리 채택될 수 있게 되었습니다.

3D 프린터 의지 업계를 형성하는 주요 기업으로는 YouBionic, WillowWood, Mercuris, Limbitless Solutions, Stratasys, Bionic Prosthetics and Orthotics, Create Prosthetics, UNYQ, Protostics, Prothea, Open Bionics, Eqwal Group(Steeper Group) 시장의 발판을 굳히기 위해 3D 프린터 의지 분야의 기업은 여러 전략적 접근 방식을 시행하고 있습니다. 주요 초점은 고급 소프트웨어 및 스캔 기술을 활용하여 제품 사용자 정의를 확대하는 것입니다. 기업들은 재료 품질과 편안함을 개선하기 위해 연구개발(R&D)에 투자하고 있습니다. 병원, 재활 센터, 연구 기관과의 전략적 협력을 통해 접근성을 높이고 혁신을 가속화하고 있습니다. 또한, 원격 사지 스캐닝과 클라우드 기반 디자인 등 디지털 워크플로우를 강화해 생산 효율성을 높이고 온라인 플랫폼과 지역별 프린팅 허브를 통해 지리적 확장을 추진하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 개인화되고 저렴한 의지 솔루션에 대한 수요 증가

- 3D 프린팅 및 재료 기술의 발전

- 당뇨병, 외상, 혈관 질환으로 인한 사지 손실 사례 증가

- 비영리 단체와 인도 지원 단체로부터의 지원 증가

- 업계의 잠재적 위험 및 과제

- 표준화된 규정 및 품질 관리의 부재

- 숙련된 전문가? 기술 지식의 부족

- 성장 촉진요인

- 성장 가능성 분석

- 갭 분석

- 기술의 상황

- 장래 시장 동향

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 특허 분석

- 가격 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 경쟁 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 사지

- 소켓

- 관절

- 기타 유형

제6장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 폴리프로필렌

- 폴리에틸렌

- 아크릴

- 폴리우레탄

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 재활센터

- 보철 클리닉

- 기타 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 일본

- 중국

- 인도

- 호주

- 한국

- 라틴아메리카

- 멕시코

- 브라질

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Bionic Prosthetics and Orthotics

- Create Prosthetics

- Eqwal Group(Steeper Group)

- Exone

- Limbitless Solutions

- Materialise

- Mercuris

- Motorica

- Open Bionics

- Prothea

- Protosthetics

- Stratasys

- UNYQ

- WillowWood

- YouBionic

The Global 3D Printed Prosthetics Market was valued at USD 1.51 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 3.1 billion by 2034, driven by the increasing demand for highly personalized prosthetic solutions, as patients seek devices tailored to their specific anatomy and day-to-day needs. Unlike conventional manufacturing methods-which are often slow and expensive and involve numerous fitting sessions-3D printing technology offers a faster and more cost-efficient approach. These custom solutions improve the overall user experience while cutting down production time. Personalization is especially valuable for pediatric patients, whose needs change frequently as they grow, requiring replacements more often. Advanced 3D printing in prosthetics is a major leap forward in meeting global healthcare demands for individualized medical devices.

Technological advancements in additive manufacturing, including Stereolithography (SLA), Selective Laser Sintering (SLS), and Fused Deposition Modeling (FDM), are enabling the creation of durable, lightweight, and functional prosthetic components. With the approval of multiple 3D printed prosthetic devices by regulatory bodies like the U.S. FDA, the technology continues gaining credibility and momentum. The availability of biocompatible materials such as medical-grade polymers and alloys has further enhanced the durability, comfort, and adaptability of prosthetic devices. These innovations not only reduce production cycles but also elevate the quality and precision of prosthetics, making them more accessible for medical professionals and patients alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.51 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 7.5% |

Polypropylene led the material segment generating USD 605.9 million in 2024, owing to its favorable strength-to-weight ratio, fatigue resistance, and chemical stability. Widely adopted in medical manufacturing, polypropylene is valued for its biocompatibility and ability to withstand sterilization. It is extensively used to fabricate prosthetic sockets, surgical guides, and orthotic supports. As demand rises for lightweight and personalized medical solutions via 3D printing, the utilization of polypropylene continues to expand. Its blend of softness and functionality makes it a preferred choice in patient-centric designs.

The prosthetic clinics segment held a 46.1% share in 2024. These specialized centers are increasingly integrating 3D printing to manage growing patient volumes, especially in regions with high rates of amputation caused by chronic conditions like diabetes and vascular disease. Clinics benefit from 3D printing's efficiency, as it allows for quick modifications and frequent replacements-particularly vital for pediatric patients. These facilities often serve as all-in-one providers, offering rehabilitation, training, and follow-up services, encouraging greater adoption of 3D printed prosthetics. Their centralized approach simplifies the user experience and builds trust among patients seeking long-term solutions.

U.S. 3D Printed Prosthetics Market is expected to reach USD 1.2 billion by 2034 driven by rising incidences of obesity, diabetes, and peripheral artery disease, underscoring the urgent need for advanced prosthetic solutions. The integration of digital health innovations such as telehealth, cloud-based workflows, and remote patient scanning is creating fertile ground for the expansion of 3D printed prosthetics. These developments allow clinicians to deliver more accurate and timely care, contributing to broader adoption across the healthcare landscape.

Key players shaping the 3D Printed Prosthetics Industry include YouBionic, WillowWood, Mercuris, Limbitless Solutions, Stratasys, Bionic Prosthetics and Orthotics, Create Prosthetics, UNYQ, Protosthetics, Prothea, Open Bionics, Eqwal Group (Steeper Group), Materialise, Exone, and Motorica. To strengthen their market foothold, companies in the 3D printed prosthetics space are implementing multiple strategic approaches. A primary focus is expanding product customization by leveraging advanced software and scanning technologies. Firms are also investing in R&D to improve material quality and comfort. Strategic collaborations with hospitals, rehabilitation centers, and research institutions are helping to increase access and accelerate innovation. In addition, companies are enhancing digital workflows, such as remote limb scanning and cloud-based design, to streamline production and expand geographically through online platforms and localized printing hubs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for personalized and affordable prosthetic solutions

- 3.2.1.2 Technological advancements in 3D printing and materials

- 3.2.1.3 Rising incidence of limb loss due to diabetes, trauma, and vascular diseases

- 3.2.1.4 Growing support from non-profits and humanitarian initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of standardized regulations and quality control

- 3.2.2.2 Limited availability of skilled professionals and technical knowledge

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Gap analysis

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Limbs

- 5.3 Sockets

- 5.4 Joints

- 5.5 Other types

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polypropylene

- 6.3 Polyethylene

- 6.4 Acrylics

- 6.5 Polyurethane

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Rehabilitation centers

- 7.4 Prosthetic clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bionic Prosthetics and Orthotics

- 9.2 Create Prosthetics

- 9.3 Eqwal Group (Steeper Group)

- 9.4 Exone

- 9.5 Limbitless Solutions

- 9.6 Materialise

- 9.7 Mercuris

- 9.8 Motorica

- 9.9 Open Bionics

- 9.10 Prothea

- 9.11 Protosthetics

- 9.12 Stratasys

- 9.13 UNYQ

- 9.14 WillowWood

- 9.15 YouBionic