|

시장보고서

상품코드

1755258

디스플레이 포장 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Display Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

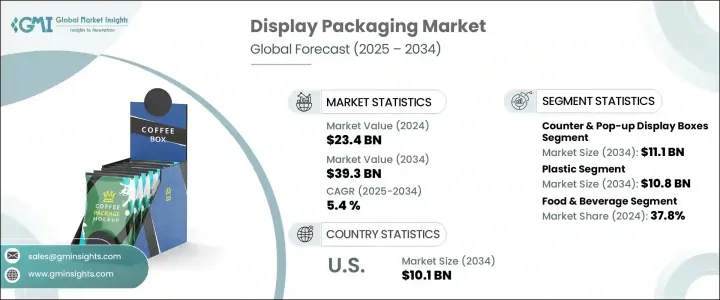

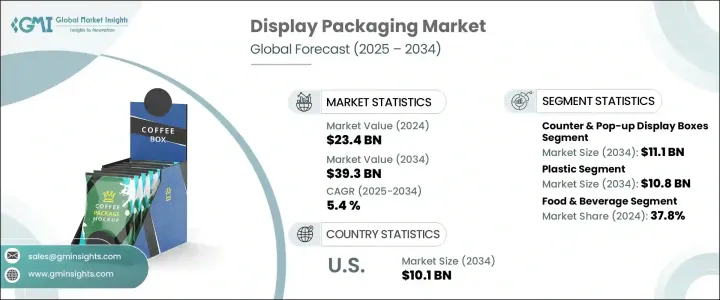

세계의 디스플레이 포장 시장은 2024년 234억 달러로 평가되었고, 2034년에는 393억 달러에 이를 것으로 추정되며, CAGR 5.4%로 성장할 전망입니다. 온라인 구매를 선택하는 쇼핑객이 증가함에 따라 창의적이고 브랜드가 돋보이는 디스플레이 포장의 매력이 주요 판매 요인이 되고 있습니다. 소셜 미디어의 동향, 특히 언박싱 콘텐츠는 미적 포장의 중요성을 더욱 부각시켰습니다.

그러나 전 세계 무역 긴장과 관세, 특히 트럼프 행정부에서 시작된 관세는 판지 및 플라스틱과 같은 원자재의 가격을 상승시켜 공급망을 혼란에 빠뜨렸습니다. 이러한 혼란은 생산 지연으로 이어져 제조업체와 공급업체 모두에 영향을 미쳤습니다. 맞춤화는 디스플레이 포장 성공의 핵심 요소로, 브랜드가 소비자와 감정적으로 연결되고 차별화하는 데 도움을 줍니다. 시장 발전은 지속 가능성과 밀접하게 연결되어 있으며, 재활용 가능 재료와 친환경 디자인에 대한 관심이 증가하고 있습니다. 기업들이 친환경 솔루션으로 전환함에 따라, 변화하는 소비자 선호도와 환경 규제를 반영한 디스플레이 포장 혁신이 계속 등장하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 234억 달러 |

| 예측 금액 | 393억 달러 |

| CAGR | 5.4% |

디스플레이 포장 산업은 제품 프레젠테이션을 개선하고 소비자 참여를 촉진하기 위해 설계된 형식을 포함합니다. 여기에는 엔드캡 디스플레이, 팔레트 디스플레이, 투명 포장, 플로어 스탠드 디스플레이, 카운터 및 팝업 디스플레이 박스가 포함됩니다. 각 유형은 소매 환경에서 뚜렷한 목적을 가지고 있습니다. 카운터 및 팝업 디스플레이 박스 부문은 2034년까지 111억 달러에 달할 것으로 예상되며, 가장 영향력 있고 상업적으로 성공적인 형식 중 하나로 부상하고 있습니다. 이러한 디스플레이는 시각적 매력과 기능적 다목적성을 결합한 능력으로 촉진되고 있습니다. 브랜드는 생생한 그래픽, 창의적인 모양 및 전략적인 배치가 구매 결정에 큰 영향을 미치는 판매 지점에서 이러한 제품을 선호합니다.

독일의 디스플레이 포장 시장은 2034년까지 연평균 성장률(CAGR) 4.9%로 성장할 것으로 예상됩니다. 독일의 공학 및 제조 분야의 깊은 전문성은 포장 솔루션 혁신을 주도하고 있으며, 특히 가벼우면서도 내구성이 뛰어난 카드보드 재료 분야에서 두드러집니다. 독일 기업들은 과도한 바닥 공간을 차지하지 않으면서 최대 가시성을 제공하는 컴팩트한 디스플레이 디자인에 집중하고 있습니다. 자동화 및 디지털 인쇄 기술을 통합하여 신속한 맞춤화 및 확장 가능한 생산이 가능해져, 독일은 유럽 디스플레이 포장 분야의 선두 주자로서의 위치를 더욱 공고히 하고 있습니다.

경쟁 구도를 형성하는 주요 기업은 Smurfit Kappa, Mondi Group, DS Smith, International Paper, WestRock Company 등입니다. 시장 입지를 공고히 하기 위해, 주요 디스플레이 포장 업체들은 혁신, 전략적 파트너십 및 지속 가능한 관행에 중점을 둔 전략을 실행하고 있습니다. 이들은 전 세계 환경 기준에 부합하는 친환경 포장 솔루션을 개발하기 위해 R&D에 투자하고 있습니다. 소매업체 및 브랜드 소유주와의 협력을 통해 진화하는 소비자 선호도에 맞는 맞춤형 디자인을 구현할 수 있습니다. 또한, 기업들은 인수 및 시설 업그레이드를 통해 전 세계에 입지를 확대하고, 생산 효율성과 지리적 도달 범위를 강화하고 있습니다. 스마트 포장 및 자동화 생산 라인과 같은 디지털 기술을 수용하는 것은 빠르게 변화하는 소매 환경에서 확장성과 대응력을 높이기 위한 또 다른 핵심 전략입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 산업에 미치는 영향

- 공급측의 영향(원료)

- 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원료)

- 영향을 받는 주요 기업

- 전략적인 산업 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 시책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 산업에 미치는 영향요인

- 성장 촉진요인

- 전자상거래 소매업의 성장

- 소비자의 제품 가시성 향상 요구 증가

- 지속 가능한 포장 재료로의 전환

- 편의성과 사용 편의성을 중시하는 소비자 선호도

- 포장 솔루션 분야의 기술 혁신

- 산업의 잠재적 리스크 및 과제

- 맞춤화 및 혁신에 드는 높은 비용

- 디자인의 복잡성과 소비자의 기대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 포장 형태별(2021-2034년)

- 주요 동향

- 카운터 및 팝업 디스플레이 박스

- 플로어 스탠드 디스플레이

- 팔레트 디스플레이

- 엔드캡 디스플레이

- 투명 포장

제6장 시장 추정 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 플라스틱

- 종이 및 판지

- 유리

- 금속

- 기타

- 연질

제7장 시장 추정 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 음식

- 화장품 및 퍼스널케어

- 의약품

- 전자기기 및 소비자용 가전제품 제품

- 기타

제8장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- alphaglobalpackaging

- Amcor plc

- CustomBoxline

- DS Smith

- Graphic Packaging International, LLC

- Ibex Packaging

- International Paper

- Mondi Group

- Orora Visual

- Packaging Corporation of America

- PakFactory

- Rengo Co.

- Salazar Packaging

- Smurfit Kappa

- Stora Enso

- WestRock Company

The Global Display Packaging Market was valued at USD 23.4 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 39.3 billion by 2034, driven by the rapid growth in e-commerce continues to demand visually appealing packaging that enhances product visibility and encourages consumer engagement. As more shoppers opt for online purchases, the appeal of creative and branded display packaging becomes a key sales driver. Social media trends, particularly unboxing content, have amplified the importance of aesthetic packaging.

However, global trade tensions and tariffs-especially those initiated during the Trump administration-have disrupted supply chains by increasing the cost of raw materials like paperboard and plastic. These disruptions have resulted in production delays, impacting manufacturers and suppliers alike. Customization remains central to the success of display packaging as it helps brands differentiate and connect emotionally with consumers. The market's evolution is closely tied to sustainability, with rising interest in recyclable materials and eco-friendly design. As companies shift toward greener solutions, innovations in display packaging continue to emerge in response to changing consumer preferences and environmental regulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.4 Billion |

| Forecast Value | $39.3 Billion |

| CAGR | 5.4% |

The display packaging industry encompasses formats designed to enhance product presentation and drive consumer engagement. These include endcap displays, pallet displays, transparent packaging, floor stand displays, and counter & pop-up display boxes. Each type serves a distinct purpose within the retail environment, The counter & pop-up display boxes segment is projected to reach USD 11.1 billion by 2034, emerging as one of the most impactful and commercially successful formats. These displays are driven by their ability to combine visual appeal with functional versatility. Brands favor these units for point-of-sale locations, where vibrant graphics, creative shapes, and strategic placement significantly influence purchase decisions.

Based on material usage, the plastic segment remains a leading choice across the industry and is expected to achieve a market value of USD 10.8 billion by 2034. The growing preference for transparent packaging has been instrumental in this growth, as consumers are more inclined to purchase items when the product is visible. This transparency builds trust and enhances shelf appeal. Simultaneously, the industry is undergoing a transition toward more eco-friendly plastic alternatives. Brands adopt recyclable and biodegradable plastics to meet tightening environmental standards and consumer demand for sustainable packaging.

Germany Display Packaging Market is forecasted to grow at a CAGR of 4.9% through 2034. The country's deep-rooted expertise in engineering and manufacturing is fueling innovation in packaging solutions, especially in lightweight yet durable cardboard materials. German companies focus on compact display designs that deliver maximum visibility without occupying excessive floor space. Integrating automation and digital printing technologies allows for rapid customization and scalable production, further solidifying Germany's position as a leader in the European display packaging landscape.

Key players shaping the competitive landscape include Smurfit Kappa, Mondi Group, DS Smith, International Paper, and WestRock Company. To solidify their market presence, leading display packaging companies are implementing strategies focused on innovation, strategic partnerships, and sustainable practices. They invest in R&D to develop eco-friendly packaging solutions that align with global environmental standards. Collaboration with retailers and brand owners allows for tailored designs that meet evolving consumer preferences. Companies are also expanding their global footprint through acquisitions and facility upgrades, enhancing production efficiency and geographic reach. Embracing digital technologies, such as smart packaging and automated production lines, is another core move to boost scalability and responsiveness in the fast-changing retail landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw material)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Growth of e-commerce retailing

- 3.3.1.2 Rising consumer demand for enhanced product visibility

- 3.3.1.3 Shift towards sustainable packaging materials

- 3.3.1.4 Consumer preference for convenience and easy-to-use packaging

- 3.3.1.5 Technological advancements in packaging solutions

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of customization and innovation

- 3.3.2.2 Design complexity and consumer expectations

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Counter & pop-up display boxes

- 5.3 Floor stand displays

- 5.4 Pallet displays

- 5.5 Endcap displays

- 5.6 Transparent packaging

Chapter 6 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Paper & paperboard

- 6.4 Glass

- 6.5 Metal

- 6.6 Others

- 6.7 Flexible

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Cosmetics & personal care

- 7.4 Pharmaceuticals

- 7.5 Electronics & appliances

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 alphaglobalpackaging

- 9.2 Amcor plc

- 9.3 CustomBoxline

- 9.4 DS Smith

- 9.5 Graphic Packaging International, LLC

- 9.6 Ibex Packaging

- 9.7 International Paper

- 9.8 Mondi Group

- 9.9 Orora Visual

- 9.10 Packaging Corporation of America

- 9.11 PakFactory

- 9.12 Rengo Co.

- 9.13 Salazar Packaging

- 9.14 Smurfit Kappa

- 9.15 Stora Enso

- 9.16 WestRock Company