|

시장보고서

상품코드

1755294

신경혈관 내 코일 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Neuroendovascular Coil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

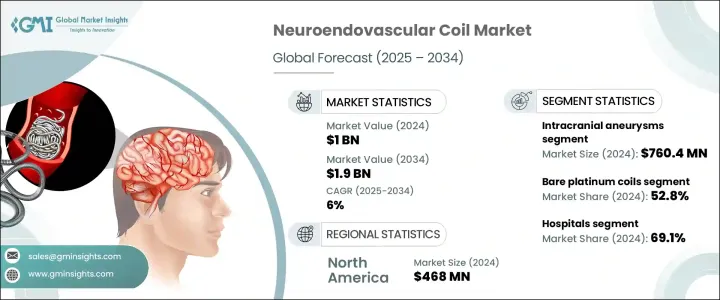

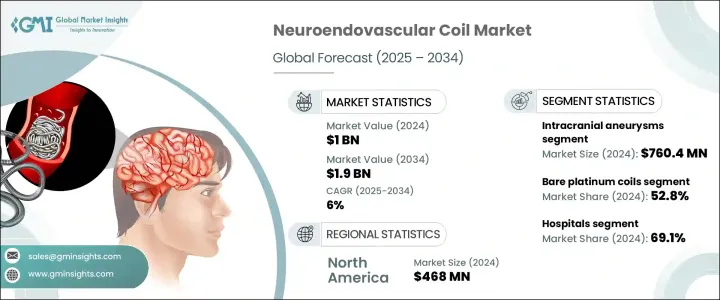

세계의 신경혈관 내 코일 시장은 2024년 10억 달러로 평가되었으며 2034년에는 19억 달러에 이를 것으로 추정되며, CAGR 6%로 성장할 전망입니다. 고혈압, 당뇨병, 흡연과 같은 위험 요인과 함께 뇌동맥류 및 허혈성 뇌졸중의 발병률이 증가하면서 신경혈관 내 코일에 대한 수요가 증가하고 있습니다. 고령화 인구 증가도 뇌동맥류 진단 사례 증가에 기여하고 있습니다. 코일 재료, 디자인, 전달 시스템 분야의 혁신은 내혈관 치료의 안전성, 정확성, 효과성을 향상시켰습니다. 최근 기술 발전으로 FDA 승인을 받은 새로운 코일링 시스템이 여러 개 출시되었으며, 이는 이 치료법의 빠른 발전을 반영합니다.

이 새로운 코일은 더 유연하고 분리 가능하며 방사선 투과성이 높아 복잡한 혈관 해부학에서도 동맥류를 치료하는 데 적합합니다. 신경혈관 내 코일링은 전통적인 수술적 접근 방식보다 절차적 합병증 위험이 낮아 의료진 사이에서 채택이 증가하고 있습니다. 최소 침습적 치료는 빠른 회복 시간, 낮은 위험, 짧은 입원 기간으로 인해 의사들과 환자 모두에게 선호되고 있습니다. 미국 심장 협회(American Heart Association)와 미국 뇌졸중 협회(American Stroke Association)는 대부분의 뇌내 동맥류 유형의 초기 치료로 신경혈관 내 코일링을 권장하며, 이는 수술적 클리핑의 중요한 대안으로 자리매김했습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 10억 달러 |

| 예측 금액 | 19억 달러 |

| CAGR | 6% |

신경혈관 내 코일 시장에서 베어 플래티넘 코일 부문은 2024년에 52.8%의 점유율을 차지했습니다. 이 코일은 두개 내 동맥류 치료에 대한 임상적 효과가 입증되어 널리 사용되고 있습니다. 베어 플래티넘 코일은 일단 삽입되면 시간이 지나도 신뢰할 수 있는 동맥류 폐색 효과를 제공합니다. 이 코일의 오랜 임상 실적을 통해 합병증 발생률이 최소화되어 많은 경우에 선호되는 제품입니다. 입증된 신뢰성은 선진국과 신흥 시장 모두에서 수요를 계속 촉진하고 있습니다. 또한 베어 플래티넘 코일의 가격대는 비용 민감도가 중요한 요인이 되고 상환이 항상 가능한 것은 아닌 의료 시스템에서 장점입니다.

병원은 신경혈관 내 코일 시장에서 가장 큰 부문을 차지하며 2024년에는 69.1%의 점유율을 기록할 것으로 예상됩니다. 전 세계 병원은 동맥류 코일링과 같은 시간 민감적인 시술에 대한 수요가 증가함에 따라 뇌졸중 및 신경혈관 치료 전용 부서를 점점 더 많이 설치하고 있습니다. 이러한 전문 부서는 뇌혈관 질환 치료에 필수적인 신경혈관 내 코일의 안정적 공급에 크게 의존하고 있습니다. 신경학적 치료와 뇌졸중 후 합병증 예방에 초점을 맞추면서 고급 코일 장치에 대한 수요가 급증하고 있습니다. 고소득 국가에서는 민간 보험사 및 공공 의료 시스템이 병원 기반 내혈관 치료에 대한 지원 보상 정책을 제공합니다.

미국의 신경혈관 내 코일 미국 시장은 2034년까지 7억 5,220만 달러에 이를 것으로 예상되고 있습니다. 미국에는 전문 뇌졸중 센터와 신경외과 부서가 광범위한 네트워크를 형성하고 있어 많은 신경혈관 시술이 진행되고 있습니다. 이러한 견고한 의료 인프라를 통해 신경혈관 내 코일의 사용이 널리 보급되고 있으며, 새로운 기술의 도입도 지속적으로 진행되고 있습니다. 이러한 의료 시설의 꾸준한 성장과 신경혈관 치료 기술의 보급 확대는 미국 시장의 확장에 기여하는 주요 요인입니다.

세계의 신경혈관 내 코일 시장의 주요 기업은 Acandis, Allium Medical, Balt, Boston Scientific, Cardinal Health, Cook Medical, Kaneka, Medtronic, MicroPort, MicroVention, Penumbra, Rapid Medical, Shape Memory Medical, Stryker, Terumo 등입니다. 신경혈관 내 코일 시장에서 입지를 다지기 위해 기업들은 다양한 전략을 추진하고 있습니다. 이에는 고급 코일 기술 도입을 위한 연구 개발에 대한 대규모 투자, 특히 안전성, 정밀도, 전달 메커니즘 개선에 중점을 두고 있습니다. 새로운 코일 재료와 디자인을 개발함으로써 제조업체들은 복잡한 동맥류 치료를 위한 더 효과적인 치료법에 대한 수요 증가에 대응하고 있습니다. 기업들은 또한 병원 및 의료 센터와의 파트너십과 협력을 통해 지리적 범위를 확장하고 있으며, 특히 의료 인프라가 빠르게 발전하는 지역에서 이를 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 산업에 미치는 영향요인

- 성장 촉진요인

- 뇌동맥류와 뇌졸중의 발생률 증가

- 코일 설계 및 전달 시스템의 기술적 발전

- 고령화 인구 증가

- 영상 유도 및 내혈관적 시술의 확산

- 산업의 잠재적 리스크 및 과제

- 신경혈관 시술 및 기기의 높은 비용

- 수술과 관련된 합병증과 동맥류 재발 위험

- 성장 촉진요인

- 성장 가능성 분석

- 기술

- 장래 시장 동향

- 규제 상황

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 상환 시나리오

제4장 경쟁 구도

- 소개

- 경쟁 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 베어 플래티넘 코일

- 하이드로겔 코팅 코일

- 기타

제6장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 두개내 동맥류

- 동정맥 기형

- 기타

제7장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 학술연구기관

제8장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 일본

- 중국

- 인도

- 호주

- 한국

- 라틴아메리카

- 멕시코

- 브라질

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Acandis

- Allium Medical

- Balt

- Boston Scientific

- Cardinal Health

- Cook Medical

- Kaneka

- Medtronic

- MicroPort

- MicroVention

- Penumbra

- Rapid Medical

- Shape Memory Medical

- Stryker

- Terumo

The Global Neuroendovascular Coil Market was valued at USD 1 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 1.9 billion by 2034. The increasing prevalence of brain aneurysms and ischemic strokes, coupled with risk factors like hypertension, diabetes, and smoking, is fueling the demand for neuroendovascular coils. The aging population is also contributing to the rise in cerebral aneurysm diagnoses. Innovations in coil materials, designs, and delivery systems have made endovascular therapy safer, more accurate, and more effective. Recent advancements in technology have led to FDA approvals for several new coiling systems, which reflect the rapid development of this treatment method.

These new coils are more conformable, detachable, and radiopaque, making them suitable for treating aneurysms, even in complex vascular anatomies. Endovascular coiling has been shown to have a lower risk of procedural complications than traditional surgical approaches, contributing to its growing adoption by physicians. Minimally invasive treatments are increasingly favored by both doctors and patients because they involve quicker recovery times, fewer risks, and shorter hospital stays. The American Heart Association and American Stroke Association recommend neuroendovascular coiling for the initial treatment of most intracranial aneurysm types, making it an important alternative to surgical clipping.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $1.9 Billion |

| CAGR | 6% |

The bare platinum coils segment in the neuroendovascular coil market held 52.8% share in 2024. These coils are widely used due to their proven clinical effectiveness in treating intracranial aneurysms. Once placed, bare platinum coils provide reliable aneurysm occlusion over time, even as they age. The long-standing clinical track record of these coils ensures minimal complication rates, making them the preferred choice for many cases. Their established reliability continues to drive demand in both developed and emerging markets. Additionally, the price point of bare platinum coils offers an advantage in healthcare systems where cost sensitivity is a significant factor, and reimbursement is not always available.

Hospitals represented the dominant segment in the neuroendovascular coil market, contributing a 69.1% share in 2024. Hospitals worldwide are increasingly setting up dedicated units for stroke and neurovascular care to meet the growing demand for time-sensitive procedures such as aneurysm coiling. These specialized units rely heavily on a steady supply of neuroendovascular coils, which are essential for treating cerebrovascular diseases. With the focus on neurological care and preventing complications after stroke, the demand for advanced coiling devices has risen significantly. In high-income nations, private insurance providers and public healthcare systems offer supportive reimbursement policies for hospital-based endovascular therapies.

U.S Neuroendovascular Coil Market is expected to reach 752.2 million by 2034. The country's extensive network of specialized stroke centers and neurosurgical departments facilitates a high volume of neuroendovascular procedures. This robust healthcare infrastructure promotes the widespread use of neuroendovascular coils and supports the adoption of new technologies over time. The steady growth of these healthcare facilities and the increasing uptake of neuroendovascular treatment technologies are key factors contributing to the market's expansion in the U.S.

Key players in the Global Neuroendovascular Coil Market include: Acandis, Allium Medical, Balt, Boston Scientific, Cardinal Health, Cook Medical, Kaneka, Medtronic, MicroPort, MicroVention, Penumbra, Rapid Medical, Shape Memory Medical, Stryker, Terumo. To solidify their position in the neuroendovascular coil market, companies are focusing on multiple strategies. These include heavy investments in research and development to introduce advanced coil technologies, with a particular focus on improving safety, precision, and delivery mechanisms. By developing new coil materials and designs, manufacturers are responding to the growing demand for more effective treatments for complex aneurysms. Companies are also expanding their geographic reach through partnerships and collaborations with hospitals and medical centers, particularly in regions where healthcare infrastructure is rapidly developing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of cerebral aneurysms and stroke

- 3.2.1.2 Technological advancements in coil design and delivery systems

- 3.2.1.3 Rising geriatric population

- 3.2.1.4 Growing adoption of image-guided and endovascular procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of neuroendovascular procedures and devices

- 3.2.2.2 Risk of procedure-related complications and recurrence of aneurysms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.7 Patent analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Reimbursement scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Bare platinum coils

- 5.3 Hydrogel-coated coils

- 5.4 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Intracranial aneurysms

- 6.3 Arteriovenous malformation

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Acandis

- 9.2 Allium Medical

- 9.3 Balt

- 9.4 Boston Scientific

- 9.5 Cardinal Health

- 9.6 Cook Medical

- 9.7 Kaneka

- 9.8 Medtronic

- 9.9 MicroPort

- 9.10 MicroVention

- 9.11 Penumbra

- 9.12 Rapid Medical

- 9.13 Shape Memory Medical

- 9.14 Stryker

- 9.15 Terumo