|

시장보고서

상품코드

1755382

단열 콘크리트 폼 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Insulated Concrete Form (ICF) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

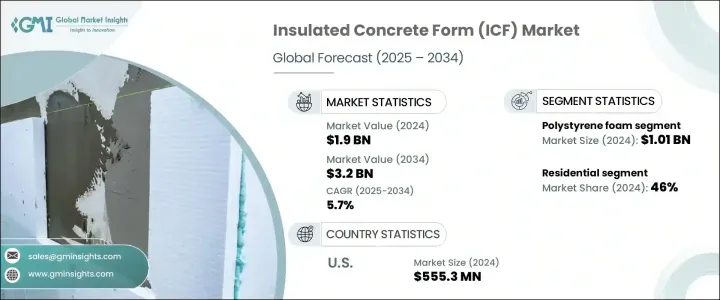

세계의 단열 콘크리트 폼 시장은 2024년에는 19억 달러로 평가되었고 2034년에는 32억 달러에 이를 것으로 추정되며, CAGR 5.7%로 성장할 전망입니다.

이러한 추세는 주로 도시화의 속도가 빨라지고 내구성이 뛰어나고 에너지 효율이 높은 주거 및 상업용 건축물에 대한 수요가 증가하기 때문입니다. 도시가 확장되고 인프라 프로젝트가 인구 증가 수요를 충족시키기 위해 확대되면서 건설 산업은 에너지 효율성, 소음 차단, 지속 가능성을 제공하는 솔루션을 우선순위로 삼고 있습니다. 단열 콘크리트 폼은 열 절연 성능과 구조적 강도에서 우수한 성능을 보여 다양한 지역에서 주목받고 있습니다.

정부와 규제 기관은 에너지 절약형 건설 관행을 장려함으로써 중요한 역할을 수행하고 있습니다. 이러한 노력은 개발자와 시공업체가 장기적인 에너지 절감과 환경 책임을 지원하는 고급 건설 기술로 전환하도록 장려하고 있습니다. 전 세계의 에너지 정책은 점차 제로 에너지 건물로 전환을 추진하며 ICF와 같은 현대적인 건축 자재로의 전환을 촉진하고 있습니다. 특히 주택 소유자와 개발업자 사이에서 친환경 의식이 급속히 확산되면서, 기존 건축 방식에 비해 우수한 대안으로 여겨지는 ICF 시스템의 채택이 증가하고 있습니다. 지속 가능한 건축 법규, 엄격한 에너지 규제, 친환경 인증 프로그램의 추진은 ICF 기반 건축의 광범위한 수용을 계속 촉진하고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025년-2034년 |

| 시작 금액 | 19억 달러 |

| 예측 금액 | 32억 달러 |

| CAGR | 5.7% |

소재별로는 폴리스티렌 폼 부문은 2024년에 약 10억 1,000만 달러의 매출로 시장을 주도했으며, 예측 기간 동안 연평균 6.3%의 성장률을 보일 것으로 예상됩니다. 이 부문의 성장은 우수한 단열성과 비용 효율성에서 기인합니다. 가볍고 내구성이 뛰어나 건설 현장에서 취급이 용이하여 시간과 인건비를 모두 절감할 수 있습니다. 현장 건설 활동 중 재료의 형태와 크기를 자유롭게 가공할 수 있는 유연성은 이 제품의 선호도를 높이고 있습니다. 폴리스티렌 폼 제품은 지속 가능성, 열 성능, 적용 편의성을 강조하는 현대 건축 기준과 일치합니다. 이 호환성은 소규모 주택부터 대규모 기관 및 상업 시설까지 다양한 건설 프로젝트에 적합하며, 다양한 구조 시스템과 콘크리트 적용 분야에 걸쳐 일관된 수요를 보장합니다.

용도별로는 주거 부문이 2024년에 전체 시장 매출의 46%를 차지하며 선두로 부상했으며, 2034년까지 연평균 6% 이상의 CAGR을 기록할 것으로 예상됩니다. 주거 부문은 방음 성능, 에너지 효율성, 극한 기상 조건에서의 복원력 때문에 ICF 시스템을 계속 선호하고 있습니다. 에너지 비용이 상승하고 소비자들이 지속 가능한 생활의 이점을 더 많이 인식함에 따라 주택 건축에 친환경 건축 관행을 채택하는 움직임이 크게 확산되고 있습니다. 이러한 동향은 지속 가능한 주택 솔루션을 장려하는 정책 수준의 지원에 의해 더욱 강화되고 있습니다. 건설업체들은 특히 기후 변화가 심하거나 혹독한 기후 조건을 가진 지역에서 ICF가 제공하는 장기적 가치를 인식하고 있습니다. 친환경 주택 솔루션에 대한 관심 증가와 엄격한 에너지 규정의 도입 확대는 향후 몇 년간 ICF의 주요 적용 분야로 주거용 건설이 유지될 것으로 예상됩니다.

지역별로는 미국이 2024년에 5억 5,530만 달러의 추정 가치로 북미 시장을 주도했으며, 2025년부터 2034년까지 연평균 6%의 성장률을 보일 것으로 예상됩니다. 시장 확장은 첨단 건축 관행, 높은 에너지 효율 기준, 주거 및 상업용 건축에 대한 투자 증가가 결합되어 촉진되고 있습니다. 현대적인 에너지 성능 기대치를 충족하거나 초과하는 건물에 대한 수요가 증가하면서 개발업자들은 ICF를 점점 더 많이 채택하고 있습니다. 이 동향에는 미국의 다양한 기후대도 중요한 역할을 하고 있습니다. 미국은 일년 내내 에너지 소비를 줄이기 위해 고성능 단열 시스템이 필요하기 때문입니다. 에너지에 민감한 소비자가 증가하고 지속 가능한 건축 관행을 보상하는 인증 제도가 추진됨에 따라 ICF는 미국 건축 프로젝트의 핵심 재료로 자리매김했습니다.

세계의 단열 콘크리트 폼 시장에 기여하는 주요 기업은 BecoWallform, Amvic, Buildblock Building System, Fox Blocks, Foam Holdings, Liteform Technologies, Nexcem, Neopar, PFB Corporation, Quad-Lock Building Systems, Polysteel Warmer Wall, Rastra Holding, Products 등입니다. 이 기업들은 시장 지위를 강화하고 전 세계적으로 증가하는 단열 콘크리트 폼에 대한 수요에 부응하기 위해 전략적 파트너십, 제품 혁신, 지역 확장에 적극적으로 참여하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 소매업체

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(고객에 대한 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 영향요인

- 성장 촉진요인

- 도시화와 인프라 개발

- 에너지 효율을 촉진하는 정부의 대처

- 재난 저항성 구조물에 대한 수요 증가

- 업계의 잠재적 위험 및 과제

- 기존 재료에 비해 높은 초기 비용

- 인식 부족 및 숙련된 인력 부족

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 가격 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 산업 구조와 집중

- 경쟁 강도 평가

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 제품의 위치 지정

- 가격 성능비 포지셔닝

- 지역적 존재

- 혁신 능력

- 전략적 대시보드

- 경쟁 벤치마킹

- 전략적 이니셔티브 평가

- 주요 업체의 SWOT 분석

- 미래 경쟁 전망

제5장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 폴리스티렌 폼

- 폴리우레탄 폼

- 시멘트 결합 목질 섬유

- 시멘트 결합 폴리스티렌 비드

- 셀룰러 콘크리트

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 상업용

- 산업용

- 인프라

- 주거용

제7장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 인도네시아

- 말레이시아

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제8장 기업 프로파일

- Amvic

- BecoWallform

- Buildblock Building System

- Foam Holdings

- Fox Blocks

- Liteform Technologies

- Logix Brands Ltd.

- Neopar

- Nexcem

- PFB Corporation

- Polysteel Warmer Wall

- Quad-Lock Building Systems

- Rastra Holding

- Standard ICF

- Superform Products

The Global Insulated Concrete Form Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 3.2 billion by 2034. This momentum is largely attributed to the increasing pace of urbanization and the growing demand for durable, energy-efficient residential and commercial structures. As cities expand and infrastructure projects scale up to meet rising population needs, the construction sector is prioritizing solutions that offer better energy efficiency, soundproofing, and sustainability. Insulated concrete forms are gaining recognition across various regions due to their high performance in thermal insulation and structural strength.

Governments and regulatory bodies are playing a crucial role by promoting energy-saving construction practices. These initiatives are encouraging developers and contractors to switch to advanced building techniques that support long-term energy savings and environmental responsibility. Global energy policies are progressively pushing for near-zero energy buildings, driving a notable shift toward modern construction materials like ICFs. The surge in eco-consciousness, especially among homeowners and developers, is leading to increased adoption of ICF systems, which are considered superior alternatives to conventional building methods. The push for sustainable building codes, stricter energy regulations, and green certification programs continues to fuel the widespread acceptance of ICF-based construction.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 5.7% |

In terms of material, the polystyrene foam segment led the market with a revenue of approximately USD 1.01 billion in 2024 and is projected to expand at a CAGR of 6.3% over the forecast period. The growth of this segment stems from its excellent thermal insulation properties and cost-effectiveness. Its lightweight and durable nature makes it highly manageable on construction sites, reducing both time and labor expenses. The flexibility to shape and cut these materials during on-site construction activities adds to their growing preference. Polystyrene foam products are aligned with modern building standards that emphasize sustainability, thermal performance, and ease of application. This compatibility makes them ideal for a broad range of construction projects, from small-scale homes to large institutional and commercial developments. Their adaptability across different structural systems and concrete applications ensures consistent demand over the forecast timeline.

Application-wise, the residential segment emerged as the frontrunner in 2024, accounting for 46% of the total market revenue, and is anticipated to register a CAGR of over 6% through 2034. The residential sector continues to favor ICF systems due to their soundproofing capabilities, energy efficiency, and resilience in extreme weather conditions. As energy costs rise and consumers become more aware of the benefits of sustainable living, there is a significant push toward adopting green construction practices in home building. This trend is amplified by policy-level support that incentivizes sustainable housing solutions. Builders are recognizing the long-term value offered by ICFs, particularly in regions with fluctuating or harsh climates. The growing interest in eco-friendly housing solutions and the increasing implementation of stringent energy codes are expected to keep residential construction as the dominant application area for ICFs over the coming years.

Regionally, the United States led the North American market with an estimated valuation of USD 555.3 million in 2024 and is set to witness a CAGR of 6% between 2025 and 2034. The market expansion is driven by a combination of advanced building practices, high energy-efficiency standards, and rising investments in both residential and commercial construction. The demand for buildings that meet or exceed modern energy performance expectations is intensifying, prompting developers to adopt ICFs at a growing rate. The country's diverse climate zones also play a significant role in this trend, as they necessitate high-performance insulation systems to reduce energy consumption throughout the year. The growing number of energy-conscious consumers, combined with the push for certifications that reward sustainable construction practices, has cemented ICFs as a key material in U.S. building projects.

Key players contributing to the global insulated concrete form market include BecoWallform, Amvic, Buildblock Building System, Fox Blocks, Foam Holdings, Liteform Technologies, Nexcem, Neopar, PFB Corporation, Quad-Lock Building Systems, Polysteel Warmer Wall, Rastra Holding, Standard ICF, and Superform Products. These companies are actively engaged in strategic partnerships, product innovation, and regional expansions to strengthen their market positions and cater to the growing global demand for insulated concrete forms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (Cost to customers)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook & future considerations

- 3.2.1 Trade impact

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Urbanization and infrastructure development

- 3.3.1.2 Government initiatives promoting energy efficiency

- 3.3.1.3 Increasing demand for disaster-resistant structures

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Higher initial costs compared to traditional materials

- 3.3.2.2 Limited awareness and skilled workforce

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Pricing analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.1.1 Industry structure and concentration

- 4.1.2 Competitive intensity assessment

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.3.1 Product positioning

- 4.3.2 Price-performance positioning

- 4.3.3 Geographic presence

- 4.3.4 Innovation capabilities

- 4.4 Strategic dashboard

- 4.4.1 Competitive benchmarking

- 4.4.1.1 Manufacturing capabilities

- 4.4.1.2 Product portfolio strength

- 4.4.1.3 Distribution network

- 4.4.1.4 R&D investments

- 4.4.2 Strategic initiatives assessment

- 4.4.3 SWOT analysis of key players

- 4.4.1 Competitive benchmarking

- 4.5 Future competitive outlook

Chapter 5 Market Estimates & Forecast, By Material, 2021 – 2034, (USD Million) (Thousand Per Sq foot)

- 5.1 Key trends

- 5.2 Polystyrene foam

- 5.3 Polyurethane foam

- 5.4 Cement-bonded wood fiber

- 5.5 Cement-bonded polystyrene beads

- 5.6 Cellular concrete

Chapter 6 Market Estimates & Forecast, By Application, 2021 – 2034, (USD Million) (Thousand Per Sq foot)

- 6.1 Key trends

- 6.2 Commercial

- 6.3 Industrial

- 6.4 Infrastructure

- 6.5 Residential

Chapter 7 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Million) (Thousand Per Sq foot)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 South Africa

Chapter 8 Company Profiles

- 8.1 Amvic

- 8.2 BecoWallform

- 8.3 Buildblock Building System

- 8.4 Foam Holdings

- 8.5 Fox Blocks

- 8.6 Liteform Technologies

- 8.7 Logix Brands Ltd.

- 8.8 Neopar

- 8.9 Nexcem

- 8.10 PFB Corporation

- 8.11 Polysteel Warmer Wall

- 8.12 Quad-Lock Building Systems

- 8.13 Rastra Holding

- 8.14 Standard ICF

- 8.15 Superform Products