|

시장보고서

상품코드

1766171

연유 및 무가당 연유 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Condensed Or Evaporated Milk Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

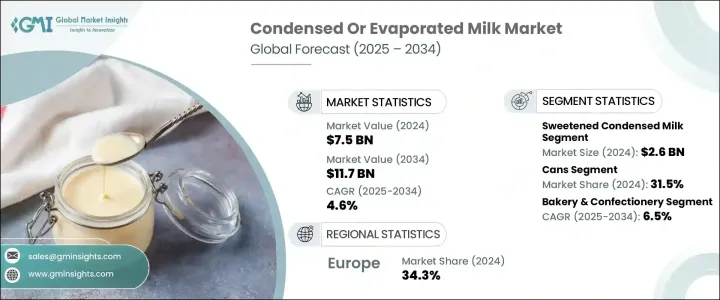

세계의 연유 및 무가당 연유 시장은 2024년에는 75억 달러로 평가되었고, 2034년에는 117억 달러에 이르며 CAGR은 4.6%를 나타낼 것으로 전망됩니다.

특히 냉장시설에의 액세스가 한정되어 있는 지역에서 보존 가능한 유제품의 인기가 높아지고 있는 것이, 이 성장의 원동력이 되고 있습니다. 소비자는 요리나 과자 만들기에 적합해, 신선한 우유의 대용품으로서 장기 보존 가능한 대용유를 요구하게 되어 있습니다.

게다가, 특히 아시아태평양과 라틴아메리카에서는 음식 동향의 변화로 연유를 사용한 레시피에 대한 관심이 다시 높아지고 있습니다. 포장 솔루션의 강화와 온라인 소매의 확대가 액세스와 편의성을 향상시키고, 신선한 유제품과 비유제품과의 경쟁 속에서 시장의 꾸준한 확대를 지원하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 75억 달러 |

| 예측 금액 | 117억 달러 |

| CAGR | 4.6% |

2024년에는 무가당 연유가 점유율 35.2%를 차지하며, 26억 달러에 이르렀습니다. 무가당 연유는 요리용으로 높은 인기를 유지하고 있지만, 초콜릿, 캐러멜, 바닐라 등의 맛있는 무가당 연유는 특히 호화로운 과자를 요구하는 젊은 소비자들 사이에서 인기를 끌고 있습니다.

캔 포장 부문은 2024년에 31.5%의 점유율을 차지했고 CAGR 4%를 나타내 소비자의 밑단을 넓힐 것으로 예측됩니다. 한편, 아셉틱 기술을 사용한 테트라팩의 카톤은 경량으로 리사이클 가능하고, 냉장하지 않고 우유를 보존할 수 있기 때문에 환경 의식이 높은 소비자에게 어필할 수 있기 때문에 인기가 높아지고 있습니다.

유럽의 연유 및 무가당 연유 시장은 2024년에 34.3%의 시장 점유율을 기록했습니다. 주로 제빵과 편의점의 부문에 의해 꾸준한 성장을 이루고 있습니다. 대조적으로, 아시아태평양은 도시화, 식습관의 변화, 이러한 유제품을 사용하는 구미 스타일의 디저트와 음료 수요 증가에 힘입어 급속한 확대를 경험하고 있습니다.

세계의 연유 및 무가당 연유 업계 주요 기업으로는 Friesland Campina NV, Arla Foods, Danone SA, Nestle SA, The JM Smucker Company(Eagle Brand) 등이 있습니다. 연유 및 무가당 연유 시장에서의 지위를 강화하기 위해 각 회사는 제품의 혁신에 주력하고 다양한 소비자의 취향에 대응하기 위해 맛의 유형을 늘리고 있습니다. 저당질, 식물성, 유당 불사용의 선택의 개발에 중점을 두는 것으로, 건강이나 식생활에 대한 관심의 고조에 대응하고 있습니다. 기업은 환경 목표와 소비자의 취향에 맞게 재활용 가능한 판지 및 경량 용기와 같은 지속 가능한 포장 솔루션에 투자하고 있습니다. 온라인 판매 채널을 전략적으로 확대하면 냉장 시설이 제한된 지역에서도 제품에 대한 액세스가 향상됩니다. 또한 외식업자와 소매업체와의 제휴는 시장 확대에 도움이 되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정·예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 가당 연유

- 무가당 연유

- 향이 첨가된 연유

- 저지방 및 무지방 변형

- 유기농 연유 및 무가당 연유

- 기타

제6장 시장 추정·예측 : 포장 유형별(2021-2034년)

- 주요 동향

- 캔

- 테트라팩

- 병

- 튜브

- 파우치

- 기타

제7장 시장 추정·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 슈퍼마켓 및 하이퍼마켓

- 편의점

- 온라인 소매

- 전문점

- 푸드서비스 업계

- 기타

제8장 시장 추정·예측 : 용도별(2021-2034년)

- 주요 동향

- 베이커리 및 과자류

- 음료

- 커피 및 차

- 스무디 및 밀크 셰이크

- 기타 음료

- 디저트 및 아이스크림

- 유아용 식품

- 소스 및 스프

- 직접 소비

- 기타

제9장 시장 추정·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 가정/소매 소비자

- 푸드서비스 업계

- 식품가공업계

- 기타

제10장 시장 추정·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제11장 기업 프로파일

- Nestle SA

- The JM Smucker Company(Eagle Brand)

- Arla Foods amba

- FrieslandCampina NV

- Goya Foods, Inc.

- Dairy Farmers of America, Inc.

- Borden Dairy Company

- Fonterra Co-operative Group Limited

- Danone SA

- Amul(Gujarat Cooperative Milk Marketing Federation Ltd.)

- California Dairies, Inc.

- Almarai Company

- Saputo Inc.

- Alaska Milk Corporation(Royal FrieslandCampina)

The Global Condensed Or Evaporated Milk Market was valued at USD 7.5 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 11.7 billion by 2034. The rising popularity of shelf-stable dairy products, especially in regions with limited refrigeration access, is driving this growth. Consumers increasingly seek long-lasting milk alternatives suitable for cooking and baking, and as substitutes for fresh milk. Demand stems largely from household use and the food service sector, including bakeries, cafes, and dessert outlets.

Additionally, shifting food trends have sparked renewed interest in recipes incorporating condensed milk, especially across Asia-Pacific and Latin America, fueled by the growth of convenience foods and ready-to-eat desserts. Innovations such as new flavors, low-sugar options, and plant-based or lactose-free alternatives are broadening the product's appeal. Enhanced packaging solutions and expanded online retail availability are improving access and convenience, supporting steady market expansion amid competition from fresh and non-dairy milk products. The market remains robust as modern and traditional diets evolve in both developed and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $11.7 Billion |

| CAGR | 4.6% |

In 2024, sweetened condensed milk accounted for a 35.2% share, valued at USD 2.6 billion. This segment continues to thrive due to focused marketing efforts and product innovation that align with consumer preferences. While unflavored condensed milk retains significant popularity for cooking applications, flavored variants-such as those with chocolate, caramel, or vanilla-are gaining traction, especially among younger consumers seeking indulgent treats.

The canned packaging segment held a 31.5% share in 2024 and is projected to grow at a 4% CAGR, expanding its consumer reach. Although cans remain the dominant packaging choice for evaporated milk due to their durability and ability to maintain product freshness, their heavier weight and higher production costs mean growth is steady rather than rapid. Meanwhile, Tetra Pak cartons using aseptic technology are becoming more popular because they are lightweight, recyclable, and preserve milk without refrigeration, appealing to environmentally conscious consumers.

Europe Condensed or Evaporated Milk Market held a 34.3% share in 2024. Regional consumption patterns and culinary traditions heavily influence market dynamics. The European market maintains steady demand driven by the widespread use of evaporated milk in cooking and processed foods. North America represents a mature market with steady growth, largely fueled by the baking and convenience food sectors. In contrast, the Asia-Pacific region is experiencing rapid expansion, propelled by urbanization, changing eating habits, and increased demand for Western-style desserts and beverages that use these dairy products.

Key players in the Global Condensed or Evaporated Milk Industry include Friesland Campina N.V., Arla Foods, Danone S.A., Nestle S.A., and The J.M. Smucker Company (Eagle Brand). To strengthen their position in the condensed or evaporated milk market, companies are focusing on product innovation and expanding flavor varieties to meet diverse consumer tastes. Emphasis on developing low-sugar, plant-based, and lactose-free options addresses growing health and dietary concerns. Firms are investing in sustainable packaging solutions, such as recyclable cartons and lightweight containers, to align with environmental goals and consumer preferences. Strategic expansion of online sales channels improves product accessibility in regions with limited refrigeration. Additionally, partnerships with food service providers and retailers help broaden market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (000’ Liters)

- 5.1 Key trends

- 5.2 Sweetened condensed milk

- 5.3 Unsweetened condensed milk (Evaporated milk)

- 5.4 Flavored condensed milk

- 5.5 Low-fat & fat-free variants

- 5.6 Organic condensed & evaporated milk

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Billion) (000’ Liters)

- 6.1 Key trends

- 6.2 Cans

- 6.3 Tetra packs

- 6.4 Bottles

- 6.5 Tubes

- 6.6 Pouches

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (000’ Liters)

- 7.1 Key trends

- 7.2 Supermarkets & Hypermarkets

- 7.3 Convenience stores

- 7.4 Online retail

- 7.5 Specialty stores

- 7.6 Foodservice industry

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (000’ Liters)

- 8.1 Key trends

- 8.2 Bakery & confectionery

- 8.3 Beverages

- 8.3.1 Coffee & tea

- 8.3.2 Smoothies & milkshakes

- 8.3.3 Other beverages

- 8.4 Desserts & ice cream

- 8.5 Infant food

- 8.6 Sauces & soups

- 8.7 Direct consumption

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (000’ Liters)

- 9.1 Key trends

- 9.2 Household/retail consumers

- 9.3 Food service industry

- 9.4 Food processing industry

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (000’ Liters)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Nestle S.A.

- 11.2 The J.M. Smucker Company (Eagle Brand)

- 11.3 Arla Foods amba

- 11.4 FrieslandCampina N.V.

- 11.5 Goya Foods, Inc.

- 11.6 Dairy Farmers of America, Inc.

- 11.7 Borden Dairy Company

- 11.8 Fonterra Co-operative Group Limited

- 11.9 Danone S.A.

- 11.10 Amul (Gujarat Cooperative Milk Marketing Federation Ltd.)

- 11.11 California Dairies, Inc.

- 11.12 Almarai Company

- 11.13 Saputo Inc.

- 11.14 Alaska Milk Corporation (Royal FrieslandCampina)