|

시장보고서

상품코드

1766184

전자 약물 전달 장치 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Electronic Drug Delivery Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

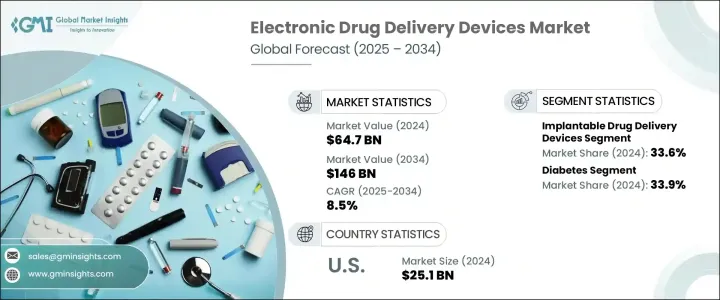

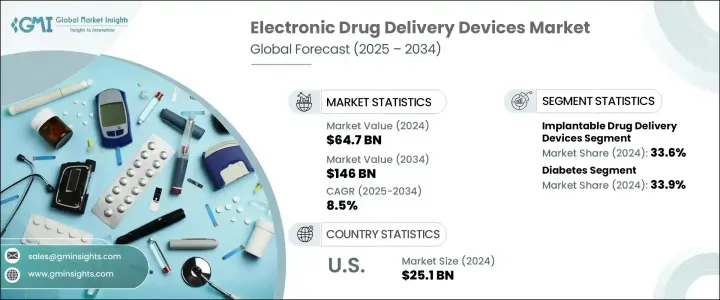

세계의 전자 약물 전달 장치 시장 규모는 2024년에 647억 달러로 평가되었고, 2034년에는 1,460억 달러에 이르며 CAGR은 8.5%를 나타낼 것으로 전망됩니다.

이러한 장치는 사용자가 수동으로 시작하거나 자동 프로그래밍하여 전자적으로 약물을 투여하도록 설계된 고급 시스템으로, 모니터링 및 규정 준수를 위해 투여 이벤트를 기록합니다. 이 기술은 실시간으로 연결된 센서 및 마이크로프로세서와 통합되어 있습니다. 또한 사전 설정된 치료 프로토콜 및 실시간 생리학적 데이터를 기반으로 정확하고 개별화된 약물 전달을 가능하게 합니다.

이것은 일관된 투약에 의한 치료 성적의 향상뿐만 아니라 입원과 모니터링의 비용 절감에도 도움이 되며, 고소득자나 자원이 부족한 헬스케어 환경에 있어서 가치가 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 647억 달러 |

| 예측 금액 | 1,460억 달러 |

| CAGR | 8.5% |

임베디드 약물 전달 장치 부문은 2024년에 33.6%의 점유율을 차지하여 시장을 견인했습니다. 법 포트 및 표적 전달 시스템과 같은 임베디드 장치는 규정 준수 위반을 줄이고 임상 결과를 향상시킵니다. 프로그램 가능한 펌프, 표적 약물 용출 임플란트, 생분해성 임플란트 수요는 통증 관리 및 신경학과 같은 다른 치료 분야로 확대되고 있습니다.

2024년에는 당뇨병 부문의 점유율이 33.9%에 달했습니다. 규제 당국의 승인과 지원적인 상환 정책을 통해 당뇨병용 전자 약물 전달 시스템을 보다 널리 이용할 수 있게 되어 보급을 뒷받침하고 있습니다.

미국의 전자 약물 전달 장치 시장은 2024년 시장 규모가 251억 달러였습니다. 웨어러블 주입 펌프의 채용이 증가하고 있으며, 그 배경에는 원격 외래 모니터링, 헬스 케어 지출 증가, 가치 기반 케어로의 변화가 있습니다.

세계의 전자 약물 전달 장치 시장 주요 기업으로는 Becton, Dickinson and Company, Pfizer, Medtronic, Insulet, West Pharmaceutical Services, Eli Lilly and Company, Novo Nordisk, Tandem Diabetes Care, Gerresheimer, Ypsomed, AstraZeneca, Abbott Laboratories, SHL Group Sanofi 등이 있습니다. 전자 약물 전달 장치 시장에서 사업을 전개하는 기업은 그 존재감을 높이기 위해 다양한 전략을 채용하고 있습니다. 또한 당뇨병 및 심혈관 질환과 같은 만성 질환을 비롯한 여러 치료 영역에 걸친 솔루션을 제공함으로써 포트폴리오를 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성질환의 발생률 상승

- 재택 헬스케어 솔루션에 대한 경향 증가

- 디지털 통합의 진보와 개인화된 치료법에 대한 의식의 고조

- 고령화 인구 증가

- 업계의 잠재적 위험 및 과제

- 고급 약물 전달 장치의 고비용

- 환자의 의식이 낮고 장치 관련 합병증

- 시장 기회

- 헬스케어 인프라가 한정되어 있는 신흥 시장에의 진출

- 개별 투여를 위한 AI와 분석의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 상환 시나리오

- 상환 정책이 시장 성장에 미치는 영향

- 특허 상황

- 소비자 행동 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정·예측 : 제품별(2021-2034년)

- 주요 동향

- 스마트 인퓨전 펌프

- 스마트 정량 흡입기

- 임베디드 약물 전달 장치

- 스마트 경피 패치

- 기타 제품

제6장 시장 추정·예측 : 용도별(2021-2034년)

- 주요 동향

- 당뇨병

- 호흡기 질환

- 종양학

- 심장학

- 기타 용도

제7장 시장 추정·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제8장 기업 프로파일

- Abbott Laboratories

- AstraZeneca

- Becton, Dickinson and Company

- Eli Lilly and Company

- Gerresheimer

- Haselmeier

- Insulet

- Medtronic

- Nemera

- Novo Nordisk

- Pfizer

- Sanofi

- SHL Group

- Tandem Diabetes Care

- West Pharmaceutical Services

- Ypsomed

The Global Electronic Drug Delivery Devices Market was valued at USD 64.7 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 146 billion by 2034. These devices are advanced systems designed to administer medication electronically, either through manual initiation by the user or automatic programming, and often record dosage events for monitoring and compliance. The technology is integrated with sensors and microprocessors that connect in real-time, enabling the delivery of precise, individualized medication based on pre-set therapeutic protocols and real-time physiological data. Unlike traditional drug delivery methods, which may suffer from adherence issues, electronic devices offer programmable, accurate, and patient-focused medication solutions.

This not only improves treatment outcomes through consistent dosing but also helps reduce hospitalization and monitoring costs, which is valuable in both high-income and resource-constrained healthcare settings. The growing elderly population, who often face chronic diseases like cancer, cardiovascular conditions, diabetes, and chronic kidney disease, is a significant factor driving the demand for electronic drug delivery systems, as these patients require continuous, user-friendly treatments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $64.7 Billion |

| Forecast Value | $146 Billion |

| CAGR | 8.5% |

The implantable drug delivery devices segment led the market in 2024, accounting for 33.6% share. With the increasing prevalence of chronic diseases like cancer, diabetes, and heart conditions, the demand for long-term, controlled drug delivery systems has grown significantly. Implantable devices, such as chemotherapy ports and targeted delivery systems, reduce non-compliance and enhance clinical outcomes. The demand for programmable pumps, targeted drug-eluting implants, and biodegradable implants is also expanding into other therapeutic areas, including pain management and neurology.

In 2024, the diabetes segment represented 33.9% share. The rising number of diabetes cases worldwide has driven demand for devices like advanced insulin pumps and patch injectors that offer continuous glucose monitoring and automatic insulin delivery. Furthermore, regulatory approvals and supportive reimbursement policies have made electronic drug delivery systems for diabetes more widely accessible, boosting adoption.

U.S. Electronic Drug Delivery Devices Market was valued at USD 25.1 billion in 2024. As the population ages and chronic diseases continue to rise, the demand for electronic drug delivery devices in the U.S. is expected to grow. The adoption of advanced autoinjectors, digital inhalers, and smart wearable infusion pumps has increased, driven by remote outpatient monitoring, rising healthcare spending, and a shift toward value-based care. The well-established digital health infrastructure in the U.S. further supports the integration of connected medical systems, which fuels the market for these devices.

Major players in the Global Electronic Drug Delivery Devices Market include Becton, Dickinson and Company, Pfizer, Medtronic, Insulet, West Pharmaceutical Services, Eli Lilly and Company, Novo Nordisk, Tandem Diabetes Care, Gerresheimer, Ypsomed, AstraZeneca, Abbott Laboratories, SHL Group, Nemera, and Sanofi. Companies operating in the electronic drug delivery devices market employ various strategies to strengthen their presence. Many are focusing on technological innovation, such as the development of more precise, user-friendly devices with real-time data capabilities. These companies are also expanding their portfolios by offering solutions across multiple therapeutic areas, including chronic diseases like diabetes and cardiovascular conditions. Strategic partnerships with healthcare providers and regulatory bodies help expedite approvals and ensure broader market access.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic diseases

- 3.2.1.2 Increasing inclination toward home-based healthcare solutions

- 3.2.1.3 Advancements in digital integration and heightened awareness around personalized therapeutics

- 3.2.1.4 Growing geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced drug delivery devices

- 3.2.2.2 Low patient awareness and device-related complications

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with limited healthcare infrastructure

- 3.2.3.2 Integration of AI and analytics for personalized dosing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Reimbursement scenario

- 3.11.1 Impact of reimbursement policies on market growth

- 3.12 Patent landscape

- 3.13 Consumer behaviour analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Smart infusion pumps

- 5.3 Smart metered dose inhalers

- 5.4 Implantable drug delivery devices

- 5.5 Smart transdermal patches

- 5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diabetes

- 6.3 Respiratory diseases

- 6.4 Oncology

- 6.5 Cardiology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 AstraZeneca

- 8.3 Becton, Dickinson and Company

- 8.4 Eli Lilly and Company

- 8.5 Gerresheimer

- 8.6 Haselmeier

- 8.7 Insulet

- 8.8 Medtronic

- 8.9 Nemera

- 8.10 Novo Nordisk

- 8.11 Pfizer

- 8.12 Sanofi

- 8.13 SHL Group

- 8.14 Tandem Diabetes Care

- 8.15 West Pharmaceutical Services

- 8.16 Ypsomed