|

시장보고서

상품코드

1773413

자동차용 통합 스타터 발전기(ISG) 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Automotive Integrated Starter-Generator Units Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

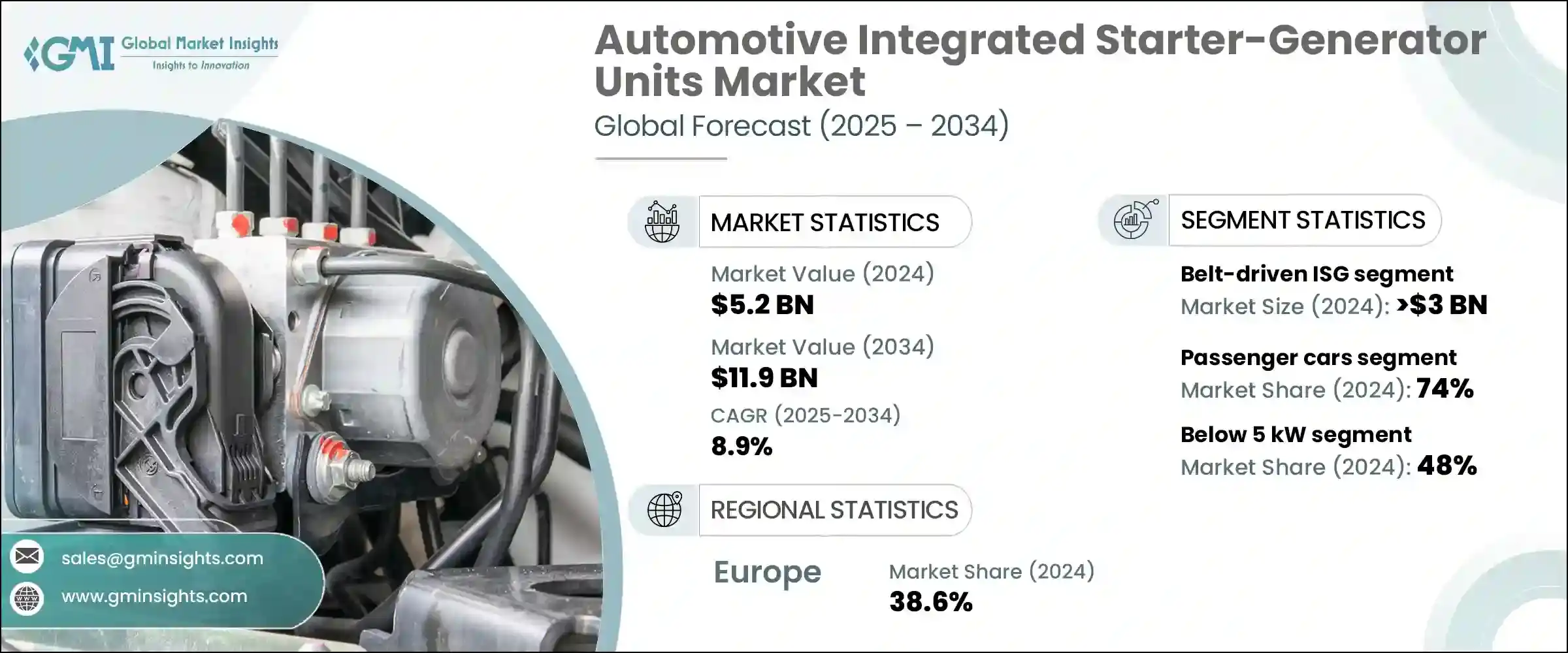

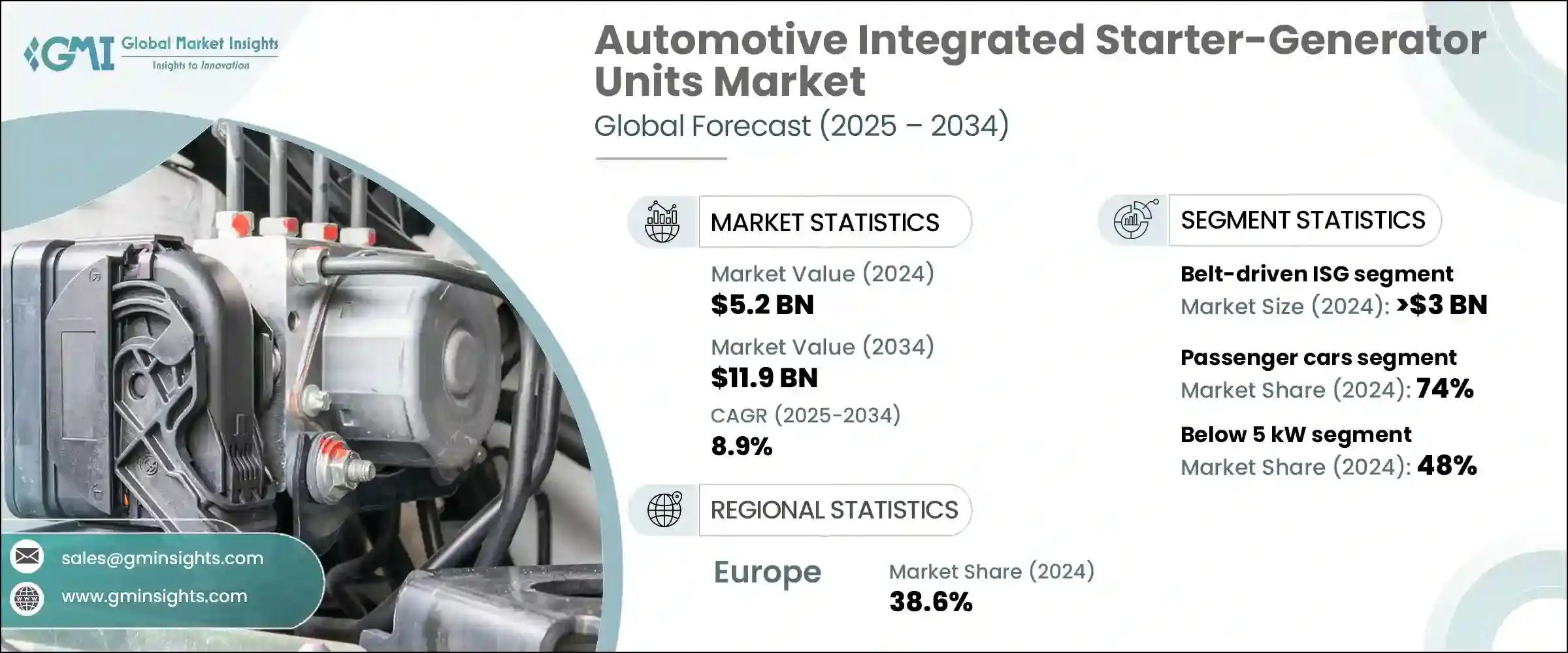

세계의 자동차용 통합 스타터 발전기(ISG) 시장 규모는 2024년에 52억 달러에 달하였고, CAGR 8.9%로 성장하여 2034년에는 119억 달러에 이를 것으로 예측됩니다.

이 성장의 주된 요인은 효율성 향상과 환경 부하 저감을 양립시킨 자동차에 대한 수요 증가를 들 수 있습니다. 통합 스타터 발전기는 풀 하이브리드 및 플러그인 하이브리드 등의 높은 가격을 지불하지 않고 더 나은 연비를 요구하는 소비자에게 매력적입니다.

프리미엄 자동차와 퍼포먼스 자동차에 대한 요구 증가도 ISG의 채용을 가속시키고 있습니다. 도시에서의 정체 증가에 따라 공회전이나 빈번한 정차 시의 연료 소비를 억제하는 시스템 수요가 급증하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 52억 달러 |

| 예측금액 | 119억 달러 |

| CAGR | 8.9% |

2024년 벨트 구동 ISG 시스템 부문은 30억 달러를 달성하였고 자동차 제조업체에 실용적이고 비용효율적인 전기화 방안을 제공함으로써 시장을 독점했습니다. 벨트 구동식은 벨트를 통해 크랭크축에 연결되므로 제조업체는 주요 부품을 재설계하지 않고도 통합할 수 있습니다.

마일드 하이브리드 전기자동차는 2024년에 가장 큰 시장 점유율을 차지하였고 앞으로도 주요 성장 분야로 지속될 것으로 예측됩니다. 마일드 하이브리드는 특히 정차가 잦은 교통 환경에서 운전성을 향상시킵니다. 또한, 마일드 하이브리드는 외부 충전에 의존하지 않기 때문에 운전 습관을 유지하면서도 환경친화적인 선택을 요구하는 소비자에게 이상적입니다.

독일의 2024년 자동차용 ISG(Integrated Starter Generator) 시장 규모는 4억 9,670만 달러를 달성하였습니다. 선도적인 제조업체는 규제 요구사항과 소비자의 기대를 모두 충족하기 위해 전체 라인업에 벨트 구동 ISG 기술을 적극적으로 도입했습니다. 세계적인 제조업체를 보유한 독일의 견고한 공급망은 현지 생산과 기술 혁신을 더욱 지원하고 세계의 ISG 시장에서 경쟁력을 유지하는 데 도움이 됩니다.

세계의 자동차용 ISG(Integrated Starter Generator) 시장에서 활약하는 주요 기업으로는 Bosch, Mitsubishi Electric, Denso, BorgWarner, Magna International, ZF Friedrichshafen, SEG Automotive, Continental, Hitachi Astemo, Valeo 등이 있습니다. 각사는 성능 향상, 경량화, 에너지 효율 개선을 위해 연구개발에 투자하고 있습니다. 또한 OEM과의 협력을 통해 특정 드라이브 트레인을 위한 솔루션을 맞춤화하고 있으며 리드 타임을 단축하고 지역 조달 정책을 준수하기 위해 현지 생산을 통해 생산 능력을 강화하고 있습니다.

목차

제1장 조사방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 연비 효율에 대한 수요의 급증

- 세계적으로 엄격한 배출 규제

- 비용 효율적인 전기 솔루션

- 고급품 및 중고품 부문에 대한 수요 증가

- 업계의 잠재적 위험 및 과제

- 엔트리레벨 차량의 초기 통합 비용이 높음

- 소비자의 인지도와 가치의 인식이 한정되어 있음

- 시장 기회

- 신흥시장에서의 48V 마일드 하이브리드의 확대

- 상용차의 전동화

- 프리미엄/고급차용 고성능 ISG

- 구형 차량의 애프터마켓과 개조

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산통계

- 생산거점

- 소비거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속 가능성과 환경 측면

- 지속 가능한 관행

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경친화적인 노력

- 탄소발자국의 고려

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 벨트 구동 ISG(B-ISG)

- 크랭크축 마운트 ISG

- 듀얼 클러치 변속기 ISG

제6장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- LCV(소형상용차)

- MCV(중형상용차)

- HCV(대형상용차)

제7장 시장 추계 및 예측 : 출력별(2021-2034년)

- 주요 동향

- 5kW 미만

- 5-10kW

- 10kW 이상

제8장 시장 추계 및 예측 : 추진 유형별(2021-2034년)

- 주요 동향

- 마일드 하이브리드 전기자동차(MHEV)

- 내연기관(ICE) 자동차

제9장 시장 추계 및 예측 : 판매채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 말레이시아

- 싱가포르

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제11장 기업 프로파일

- Aisin Corporation

- BorgWarner

- Bosch

- Continental

- Denso Corporation

- Hitachi Astemo

- Hyundai Mobis Co

- Johnson Electric Holdings

- Magna International

- MAHLE Group

- Mando Corporation

- Mitsubishi Electric Corporation

- Nidec Corporation

- Prestolite Electric Incorporated

- Schaeffler AG

- SEG Automotive

- Toyota Industries

- Woory Industrial Co

- Valeo

- ZF Friedrichshafen

The Global Automotive Integrated Starter-Generator Units Market was valued at USD 5.2 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 11.9 billion by 2034. This growth is largely fueled by rising demand for vehicles that offer both improved efficiency and reduced environmental impact. As global regulations surrounding emissions become stricter, automakers are ramping up the rollout of mild hybrid models that incorporate ISG technology. These systems are attractive to consumers seeking better fuel economy without the steep price tag associated with full or plug-in hybrids. ISG-equipped powertrains provide a middle ground-delivering noticeable fuel savings with minimal disruption to conventional vehicle designs.

The growing appetite for premium and performance vehicles is also accelerating the adoption of ISG units, as they contribute to smoother engine start-stop operations and deliver low-end torque improvements that enhance driving feel. This aligns perfectly with what high-end buyers want-efficiency without sacrificing power or luxury. As congestion increases in urban areas, demand for systems that reduce fuel use during idling and frequent stops has surged. ISG units help manage these challenges while also reducing emissions, making them a favored option in the push for smarter, greener urban transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $11.9 Billion |

| CAGR | 8.9% |

In 2024, the belt-driven ISG systems segment generated USD 3 billion, dominating the market by offering automakers a practical and cost-effective route to electrification. These units are mounted on the engine's front and connected via a belt to the crankshaft, allowing manufacturers to integrate them without redesigning major components. This streamlined integration is a major advantage for brands looking to electrify existing vehicle platforms quickly, saving both time and capital.

Mild hybrid-electric vehicles represented the largest market share in 2024 and are projected to remain a key growth area. These vehicles incorporate a compact battery and deliver performance benefits that drivers can immediately notice-from quiet operation during coasting to seamless engine restarts. The low-end torque boost improves drivability, particularly in stop-and-go traffic. Additionally, mild hybrids do not rely on external charging, making them ideal for consumers who want eco-friendly options without changing their driving habits. As a result, these systems are becoming more common across both commercial fleets and personal vehicles.

Germany Automotive Integrated Starter-Generator Units Market generated USD 496.7 million in 2024. The country's dominant position is supported by a mature automotive manufacturing base and early adoption of 48-volt systems across various vehicle classes. Leading manufacturers have aggressively implemented belt-driven ISG technology across their lineups to meet both regulatory demands and consumer expectations. Germany's robust supply chain, with major contributors such as Bosch, Continental, and ZF Friedrichshafen, further supports local production and innovation, helping the country maintain a competitive edge in the global ISG market.

Key players active in the Global Automotive Integrated Starter-Generator Units Market include Bosch, Mitsubishi Electric, Denso, BorgWarner, Magna International, ZF Friedrichshafen, SEG Automotive, Continental, Hitachi Astemo, and Valeo. To secure a leading position in the automotive ISG market, companies are focusing on several strategic areas. One core strategy involves investment in R&D to enhance performance, reduce weight, and improve the energy efficiency of ISG systems. Manufacturers are also targeting platform scalability to allow ISG integration across various vehicle categories. Collaborations with OEMs play a key role in customizing solutions for specific drivetrains. In addition, firms are strengthening their production capabilities through localized manufacturing to reduce lead times and comply with regional sourcing policies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Power rating

- 2.2.5 Propulsion type

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in demand for fuel efficiency

- 3.2.1.2 Stricter emission regulations worldwide

- 3.2.1.3 Cost-effective electrification solution

- 3.2.1.4 Growing demand in the luxury and mid-premium segment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial integration cost for entry-level vehicles

- 3.2.2.2 Limited consumer awareness and perceived value

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of 48V mild hybrids in emerging markets

- 3.2.3.2 Commercial vehicle electrification

- 3.2.3.3 High-performance ISGs for premium/luxury vehicles

- 3.2.3.4 Aftermarket & retrofits for legacy fleets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Belt-driven ISG (B-ISG)

- 5.3 Crankshaft-mounted ISG

- 5.4 Dual-clutch transmission ISG

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedan

- 6.2.2 SUV

- 6.2.3 Hatchback

- 6.3 Commercial vehicles

- 6.3.1 LCVs (light commercial vehicles)

- 6.3.2 MCVs (medium commercial vehicles)

- 6.3.3 HCVs (heavy commercial vehicles)

Chapter 7 Market Estimates & Forecast, By Power rating, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Below 5 kW

- 7.3 5–10 kW

- 7.4 Above 10 kW

Chapter 8 Market Estimates & Forecast, By Propulsion type, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Mild hybrid electric vehicles (MHEVs)

- 8.3 Internal combustion engine (ICE) vehicles

Chapter 9 Market Estimates & Forecast, By Sales channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aisin Corporation

- 11.2 BorgWarner

- 11.3 Bosch

- 11.4 Continental

- 11.5 Denso Corporation

- 11.6 Hitachi Astemo

- 11.7 Hyundai Mobis Co

- 11.8 Johnson Electric Holdings

- 11.9 Magna International

- 11.10 MAHLE Group

- 11.11 Mando Corporation

- 11.12 Mitsubishi Electric Corporation

- 11.13 Nidec Corporation

- 11.14 Prestolite Electric Incorporated

- 11.15 Schaeffler AG

- 11.16 SEG Automotive

- 11.17 Toyota Industries

- 11.18 Woory Industrial Co

- 11.19 Valeo

- 11.20 ZF Friedrichshafen