|

시장보고서

상품코드

1773414

흉요추 고정 임플란트 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Thoracolumbar Spinal Fusion Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

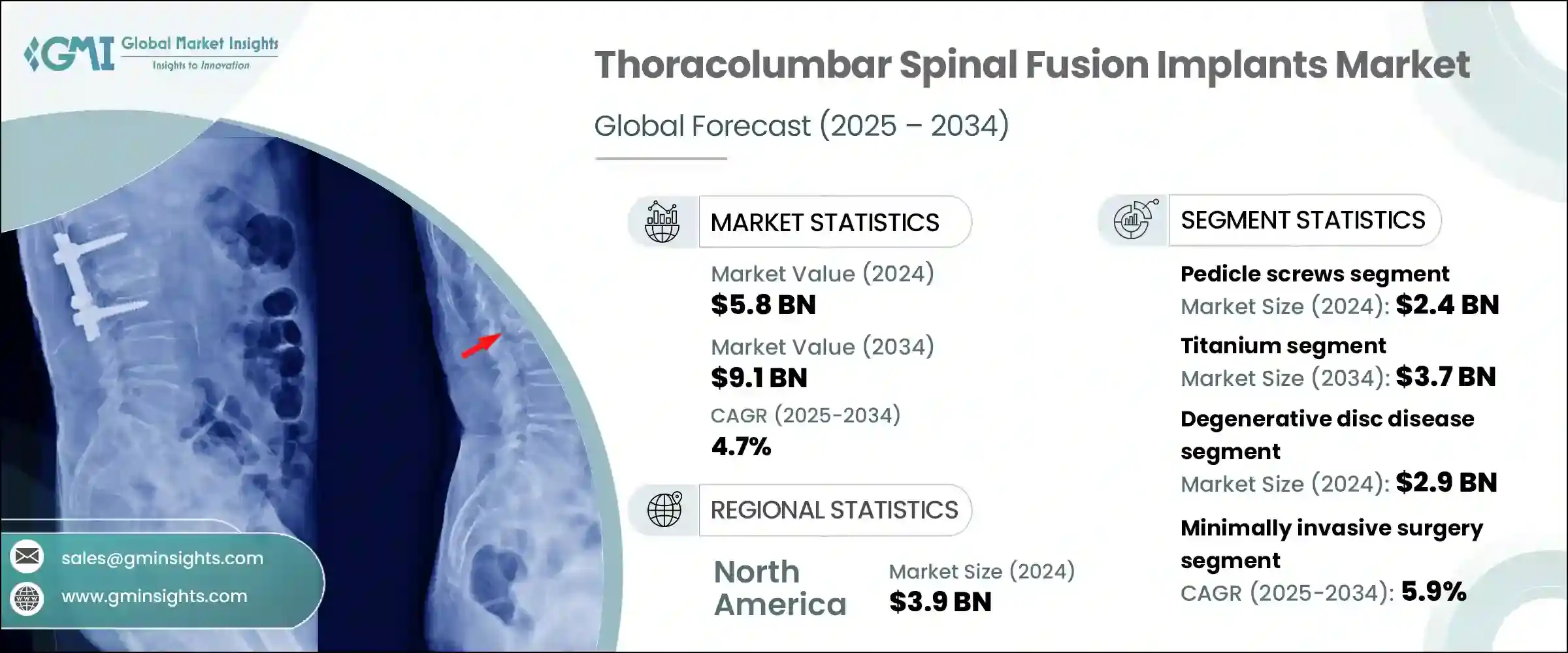

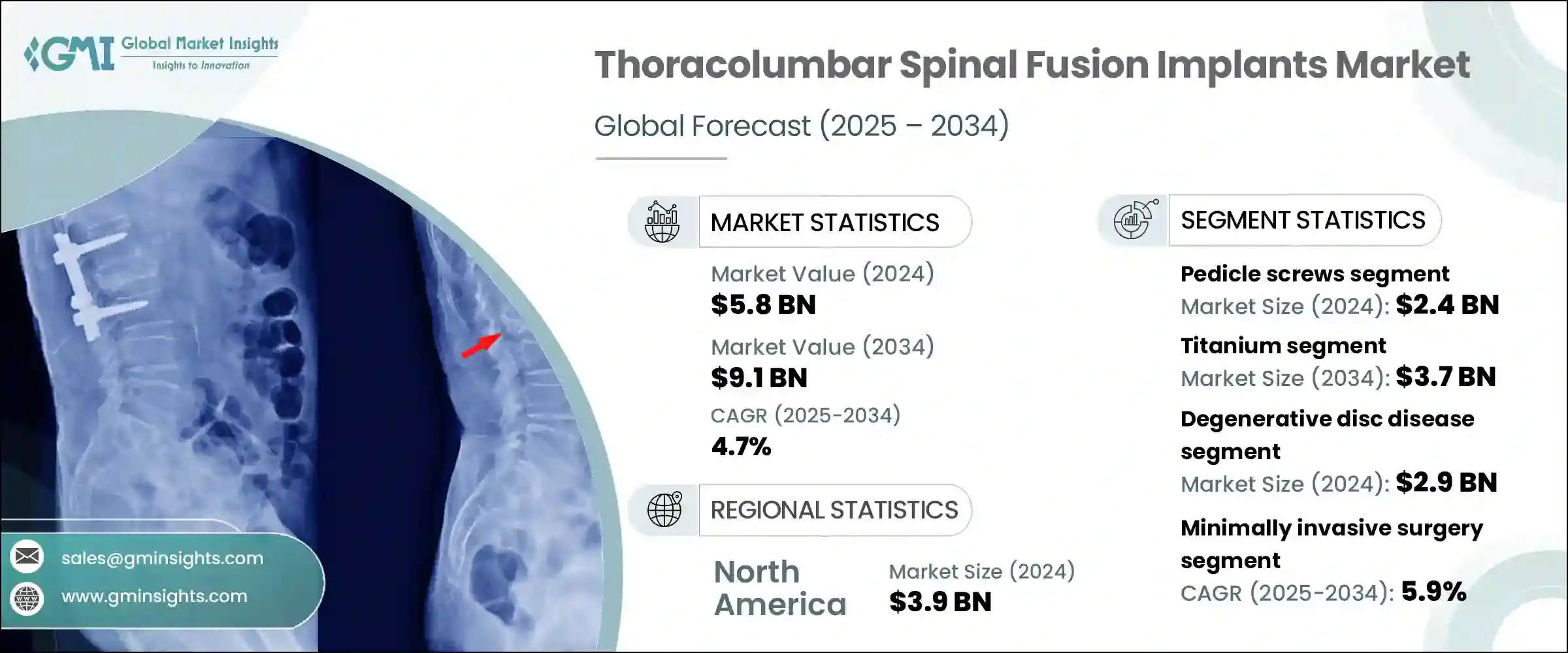

세계의 흉요추 고정 임플란트 시장은 2024년에 58억 달러로 평가되었고 CAGR 4.7%로 성장하여 2034년에는 91억 달러에 이를 것으로 추정되고 있습니다.

시장 확대의 원동력이 되고 있는 것은 척추 질환의 유병률 증가, 교통 사고에 의한 상해의 급증, 저침습 수술 솔루션에 대한 관심의 고조입니다. 척추 안정화에 대한 수요가 증가하면서 병원과 수술센터 전반적으로 척추 고정술의 도입이 확대되고 있습니다. 세계의 노인 인구 증가에 따라 노화에 수반하는 척추 합병증 가운데 특히 흉요추 영역의 합병증의 빈도는 증가세를 보이고 있어 고정 임플란트의 채용이 확대되고 있습니다.

또한 수술 방법을 개선하고 침습성이 낮은 접근법을 선호하는 환자의 선호도가 특히 신흥 건강 관리 시스템에서 이러한 동향을 뒷받침하고 있습니다. 한편 기업들은 조직 손상을 최소화하는 수술용 임플란트의 기술 혁신에도 주목하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 58억 달러 |

| 예측금액 | 91억 달러 |

| CAGR | 4.7% |

2024년 흉요추 고정 임플란트 시장은 척추경 나사가 24억 달러의 평가액으로 압도적인 점유율을 차지하였습니다. 척추경 나사는 척추 골절의 안정화, 교정, 추간판 압력의 완화를 위한 유력한 선택이 되고 있습니다.

외과의사는 특히 외상이나 변형 교정 사례 등 높은 정밀도와 장시간의 지지를 필요로 하는 수술에 이러한 시스템을 선호하여 사용하고 있습니다. 차세대 척추경 나사에는 다축성 나사 머리, 유관나사, 연장 가능 형태 등의 고급 구성이 포함되어 있습니다. 이러한 기능적 향상은 수술 중 효율성, 외과의사의 제어 능력, 다양한 척추 해부에 대한 적응성을 향상시킵니다.

티타늄 부문은 2034년까지 37억 달러에 이를 것으로 예측됩니다. 티타늄 소재는 인체 조직과의 높은 호환성으로 골통합을 신속하게 실시할 수 있습니다. 티타늄의 탄성률은 사람 뼈의 탄성률과 닮아 있기 때문에 응력의 차폐가 적고 임플란트의 탈락이나 인접 부문 질환 등의 합병증을 최소한으로 억제할 수 있습니다. 또한, MRI나 CT 스캔 등의 영상 진단 기술과의 적합성에 의해 임상적 효과를 인정받았습니다.

미국의 흉요추 고정 임플란트 시장은 2024년에 36억 달러로 평가되었습니다. 로봇공학과 네비게이션 시스템이 척추 수술의 워크플로우에 통합되어 고정 수술의 정확성이 향상되고 임플란트 수요가 증가하고 있습니다. Globus Medical과 Medtronic 같은 주요 기업은 지속적인 제품 혁신, 외과의사 교육 프로그램 및 광범위한 판매 제휴를 통해 미국 시장에서 강한 존재감을 유지하고 있습니다.

세계의 흉요추 고정 임플란트 시장을 형성하고 있는 유력 기업에는 Highridge Medical(ZimVie), B. Braun, Spineart, Orthofix Medical, DePuy Synthes(JnJ), Ulrich, JAYON, Alphatec Spine, Medtronic, Stryker(VB Spine), RTI Surgical, Globus Medical, WASTON MEDICAL, GS Medical 등이 있습니다. 이러한 기업은 수술 포트폴리오를 확대하고 임플란트 기술을 발전시켜 다양한 환자 요구에 대응하고 있습니다.

흉요추 고정 임플란트 시장의 각사는 시장에서의 포지셔닝을 강화하기 위해 적극적인 기술 혁신, 제품 개발, 세계 시장 전개를 진행하고 있습니다. 각사는 또한 시스템 설계에 투자하고 있으며 맞춤화, 모듈성 및 적응성은 시장에서 선호되는 제품의 핵심 기능입니다.

목차

제1장 조사방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 척추질환의 유병률 상승

- 저침습 수술 수요 증가

- 기술적 진보

- 유리한 보험 환급 정책

- 업계의 잠재적 위험 및 과제

- 척추 임플란트와 수술의 높은 비용

- 엄격한 규제 시나리오

- 기회

- 척추 수술에서 AI와 로봇의 통합

- 외래 진료와 통원 진료에 대한 주목 고조

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 제품별 가격 동향

- 장래 시장 동향

- 보험 환급 시나리오

- 보험 환급 정책이 시장 성장에 미치는 영향

- 소비자 행동 분석

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 기업 매트릭스 분석

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 척추경 나사

- 추간체 고정 장치(IBFD)

- 로드

- 플레이트

- 기타 제품 유형

제6장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 티타늄

- 폴리에테르에테르케톤(PEEK)

- 코발트 크롬

- 스테인레스 스틸

- 기타 재료

제7장 시장 추계 및 예측 : 수술 유형별(2021-2034년)

- 주요 동향

- 개복 수술

- 저침습 수술

제8장 시장 추계 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 변성 추간판 질환

- 척추 외상

- 척추 변형

- 척추 종양

- 기타 적응증

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 정형외과 클리닉

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Alphatec Spine

- B. Braun

- DePuy Synthes(JnJ)

- Globus Medical

- GS Medical

- Highridge Medical(ZimVie)

- JAYON

- Medtronic

- Orthofix Medical

- RTI Surgical

- Spineart

- Stryker(VB Spine)

- Ulrich

- WASTON MEDICAL

The Global Thoracolumbar Spinal Fusion Implants Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 9.1 billion by 2034. Market expansion is being driven by the increasing prevalence of spinal conditions, a surge in road-related injuries, and rising interest in minimally invasive surgical solutions. Growing demand for spinal stabilization in trauma cases, degenerative disorders, and congenital deformities has significantly boosted the uptake of spinal fusion procedures across hospitals and surgical centers. As the global elderly population rises, the frequency of age-associated spine complications-particularly in the thoracolumbar region-continues to grow, leading to greater adoption of fusion implants.

Furthermore, improvements in surgical methods and patient preference for less invasive approaches are supporting this trend, especially in emerging healthcare systems. As medical professionals seek faster recovery times and fewer complications, they're turning to innovations in surgical implants that minimize tissue damage while providing long-term spinal support. Overall, the combination of clinical necessity, aging demographics, technological advancement, and growing trauma incidence is pushing the market toward consistent growth globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 4.7% |

In 2024, pedicle screws dominated the thoracolumbar spinal fusion implants market with a total valuation of USD 2.4 billion. Their structural strength and ability to provide rigid three-dimensional spinal support make them the go-to option for stabilizing vertebral fractures, correcting alignment issues, or relieving disc pressure. Their utility is amplified in thoracolumbar surgeries, where secure fixation is critical.

Surgeons prefer these systems for procedures that demand high precision and long-lasting support, especially in trauma and deformity correction cases. With more minimally invasive techniques being adopted, newer generations of pedicle screws now include advanced configurations such as polyaxial heads, cannulated shafts, and expandable versions. These enhancements are improving intraoperative efficiency, surgeon control, and adaptability to varying spinal anatomies-all of which are enhancing clinical outcomes and boosting procedural success.

The titanium segment will reach USD 3.7 billion by 2034. Titanium and its alloys, especially Ti-6Al-4V, have become the preferred material choice for spinal fusion implants due to their ideal combination of high strength, biocompatibility, and corrosion resistance. Titanium's compatibility with human tissue enables quicker bone integration, which is vital for achieving long-term fusion. Its elastic modulus closely resembles that of human bone, reducing stress shielding and minimizing complications like implant loosening or adjacent segment disease. Moreover, its compatibility with diagnostic imaging technologies, including MRI and CT scans, further enhances its clinical desirability.

United States Thoracolumbar Spinal Fusion Implants Market was valued at USD 3.6 billion in 2024. This growth can be attributed to high surgical volumes, cutting-edge surgical technology availability, and favorable insurance reimbursement policies. A growing elderly population experiencing spinal stenosis, spondylolisthesis, and degenerative disc issues continues to fuel procedural demand. In addition, the integration of robotics and navigation systems into spinal surgery workflows has improved the precision of fusion procedures, thereby increasing the demand for implants. The broader use of expandable cages and percutaneous screw systems in minimally invasive techniques further boost market volume. Leading companies like Globus Medical and Medtronic maintain a strong market presence in the U.S. through continued product innovation, surgeon education programs, and wide-reaching distribution partnerships.

Prominent players shaping the Global Thoracolumbar Spinal Fusion Implants Market include Highridge Medical (ZimVie), B. Braun, Spineart, Orthofix Medical, DePuy Synthes (JnJ), Ulrich, JAYON, Alphatec Spine, Medtronic, Stryker (VB Spine), RTI Surgical, Globus Medical, WASTON MEDICAL, and GS Medical. These companies play pivotal roles in expanding surgical portfolios, improving implant technologies, and addressing diverse patient needs.

Companies in the thoracolumbar spinal fusion implants market are pursuing aggressive innovation, product development, and global expansion to strengthen their market positioning. Major players are investing in the design of advanced implant systems that support minimally invasive procedures and accommodate varying patient anatomies. Customization, modularity, and adaptability are core product features being prioritized. Firms are also collaborating with surgeons for clinical trials and real-world evidence generation to refine products and ensure clinical efficacy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates & calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Surgery type

- 2.2.5 Indication

- 2.2.6 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of spinal diseases

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Favorable reimbursement policies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of spinal implants and surgeries

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Opportunities

- 3.2.3.1 Integration of AI and robotics in spine surgery

- 3.2.3.2 Growing focus on outpatient and ambulatory settings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pedicle screws

- 5.3 Intervertebral body fusion device (IBFD)

- 5.4 Rods

- 5.5 Plates

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Polyether ether ketone (PEEK)

- 6.4 Cobalt chrome

- 6.5 Stainless steel

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Surgery Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open surgery

- 7.3 Minimally invasive surgery

Chapter 8 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Degenerative disc disease

- 8.3 Spinal trauma

- 8.4 Spinal deformities

- 8.5 Spinal tumors

- 8.6 Other indications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Orthopedic clinics

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alphatec Spine

- 11.2 B. Braun

- 11.3 DePuy Synthes (JnJ)

- 11.4 Globus Medical

- 11.5 GS Medical

- 11.6 Highridge Medical (ZimVie)

- 11.7 JAYON

- 11.8 Medtronic

- 11.9 Orthofix Medical

- 11.10 RTI Surgical

- 11.11 Spineart

- 11.12 Stryker (VB Spine)

- 11.13 Ulrich

- 11.14 WASTON MEDICAL